Planning for a comfortable retirement is a journey that requires foresight, discipline, and strategic financial planning. In an era where financial security in retirement is becoming increasingly uncertain, understanding the best long-term saving strategies is crucial. This article aims to equip you with the knowledge and tools necessary to build a robust retirement savings plan. By exploring various saving strategies, investment options, and financial planning techniques, we will guide you through the essential steps to ensure that your golden years are not only secure but also enjoyable. Whether you’re just starting your career or nearing retirement, it’s never too late to take control of your financial future. Let’s delve into the most effective ways to save for a retirement that meets your aspirations and provides peace of mind.

Understanding Retirement Goals and Financial Needs

To ensure a comfortable retirement, it is crucial to have a clear understanding of your retirement goals and financial needs. These objectives will guide your saving strategies and help you maintain the lifestyle you envision. Begin by asking yourself what kind of lifestyle you desire in retirement. Do you plan to travel extensively, relocate to a different city, or perhaps start a small business? Each of these choices will have distinct financial implications. Consider the following key factors when setting your retirement goals:

- Estimated Retirement Age: Determine when you plan to retire to calculate how many years you need to save.

- Expected Lifespan: Consider how long you might live to ensure your savings last throughout your retirement.

- Current Savings: Evaluate your current assets and savings to understand your starting point.

- Income Sources: Identify potential income sources such as pensions, Social Security, and investments.

- Inflation and Healthcare Costs: Account for rising living costs and healthcare expenses, which can significantly impact your savings.

By clearly defining these elements, you will be better positioned to select the most effective saving strategies that align with your vision for retirement. With the right plan, you can achieve financial security and enjoy a fulfilling retirement.

Maximizing Growth with Diversified Investment Portfolios

To achieve a robust financial future, consider crafting a diversified investment portfolio that caters to both stability and growth. Diversification involves spreading your investments across various asset classes, sectors, and geographic regions, which can mitigate risk and enhance potential returns over the long term. Here are some strategies to consider:

- Equity Investments: Allocate a portion of your portfolio to stocks, focusing on a mix of blue-chip companies and emerging markets to capture growth opportunities.

- Bonds and Fixed Income: Incorporate government and corporate bonds to provide steady income and cushion against stock market volatility.

- Real Estate: Consider real estate investment trusts (REITs) or direct property investments to benefit from property value appreciation and rental income.

- Commodities: Add commodities like gold or agricultural products to hedge against inflation and diversify your portfolio further.

- Alternative Investments: Explore opportunities in private equity, hedge funds, or cryptocurrencies to enhance growth potential and diversify beyond traditional assets.

By integrating a balanced mix of these components, investors can position themselves to not only withstand market fluctuations but also capitalize on various economic cycles, ensuring a more secure and comfortable retirement.

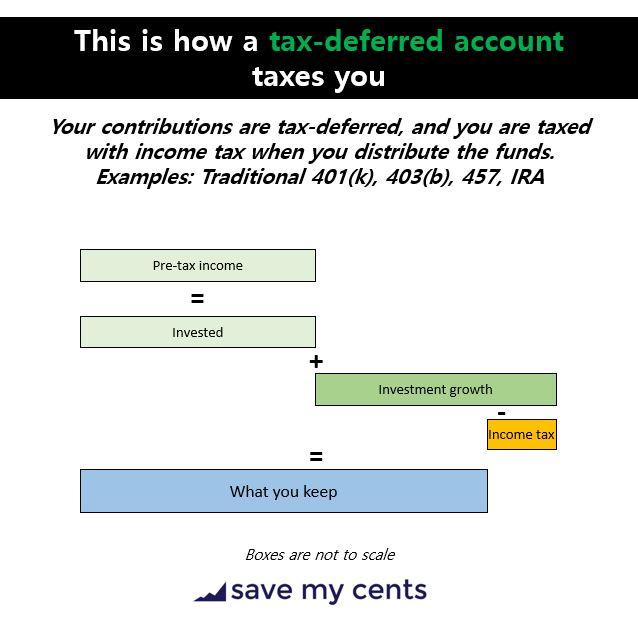

Harnessing Tax-Advantaged Accounts for Long-Term Benefits

When planning for a secure and enjoyable retirement, understanding and utilizing tax-advantaged accounts can be a game-changer. These accounts, designed to encourage saving by offering tax benefits, can significantly enhance your financial growth over the long term. Individual Retirement Accounts (IRAs) and 401(k) plans are among the most popular options, each offering distinct advantages. By contributing to a traditional IRA or 401(k), you can benefit from tax-deferred growth, meaning you won’t pay taxes on your contributions or earnings until you withdraw the funds in retirement. This allows your investments to compound more effectively, potentially leading to a more substantial retirement nest egg.

- Roth IRAs provide another excellent option, offering tax-free growth and tax-free withdrawals in retirement, assuming certain conditions are met.

- Health Savings Accounts (HSAs), although primarily for medical expenses, can also serve as a retirement savings vehicle with triple tax benefits: tax-deductible contributions, tax-free earnings, and tax-free withdrawals for qualified medical expenses.

Integrating these accounts into your long-term saving strategy not only maximizes your retirement funds but also offers flexibility and tax efficiency. The key is to assess your current financial situation, projected retirement needs, and tax implications to choose the right mix of accounts that align with your goals. Remember, starting early and consistently contributing to these accounts can amplify your financial security, ensuring a comfortable retirement.

Incorporating Real Estate for Steady Income and Appreciation

For those seeking a reliable path to a comfortable retirement, integrating real estate into your financial strategy can offer both consistent income and potential for appreciation. Real estate investments, such as rental properties or real estate investment trusts (REITs), provide a steady cash flow through rental income or dividends, which can be particularly appealing in times of market volatility. Moreover, real estate has a history of appreciating in value over time, thus enhancing your asset portfolio.

- Diversification: Real estate adds a layer of diversification to your retirement portfolio, reducing overall risk.

- Tax Benefits: Enjoy deductions on mortgage interest, property depreciation, and other expenses.

- Inflation Hedge: Real estate often outpaces inflation, preserving purchasing power.

Strategic Considerations: Ensure you research the local market trends and economic indicators before making a purchase. Opt for properties in growing areas with strong rental demand to maximize returns. Alternatively, investing in REITs can offer exposure to real estate markets without the need for direct property management, making it a hands-off option for retirees.

{kind=link}