Raising a family while saving for a home might seem like juggling two full-time jobs, each with its own set of challenges and rewards. Yet, with the right strategies and a clear plan, you can achieve both without sacrificing one for the other. In this guide, we will explore practical, actionable steps to help you navigate the financial complexities of family life and homeownership goals. From budgeting tips to creative saving techniques, this article is designed to equip you with the tools and confidence needed to make your dream home a reality, all while ensuring your family thrives. Get ready to take charge of your financial future and create a stable, nurturing environment for your children.

Creating a Family Budget that Prioritizes Home Savings

When planning a budget that focuses on saving for a home while raising children, it’s crucial to strike a balance between current needs and future goals. Start by analyzing your family’s monthly expenses to identify areas where you can cut back. Track your spending meticulously for a month to gain insights into unnecessary expenditures. Once you have a clear picture, create a realistic budget that includes a specific savings goal for your home. Use tools like spreadsheets or budgeting apps to keep everything organized and transparent.

Implementing a few strategic changes can make a significant difference in your savings journey. Consider these options:

- Automate savings: Set up automatic transfers to a dedicated home savings account each month.

- Cut discretionary spending: Reduce dining out, subscription services, and impulse buys.

- Involve the family: Encourage kids to participate in cost-saving activities like energy conservation or home-cooked meals.

- Review and adjust: Regularly review your budget to ensure it aligns with your goals and make adjustments as needed.

By focusing on these strategies, you’ll be well on your way to achieving your dream of homeownership while still meeting the needs of your growing family.

Smart Strategies for Reducing Household Expenses

Finding ways to trim down household expenses is crucial when trying to save for a home, especially with the additional costs of raising kids. Start by reviewing your monthly bills and subscriptions. Cancel or downgrade any services you rarely use, and consider switching to more affordable alternatives. For instance, opt for a family mobile plan or explore community activities that offer free or low-cost entertainment for the whole family. Every little saving adds up, creating a more significant pool for your down payment fund.

Another effective method is to embrace energy-efficient practices. Simple changes like using LED bulbs, unplugging devices when not in use, and setting a programmable thermostat can significantly cut down utility bills. Consider implementing a meal plan to reduce grocery expenses, focusing on nutritious yet cost-effective meals. Engage your children in the process by involving them in meal prep or shopping for groceries, teaching them valuable lessons about budgeting and smart spending. Implementing these strategies will not only help you save money but also instill financial responsibility in your kids.

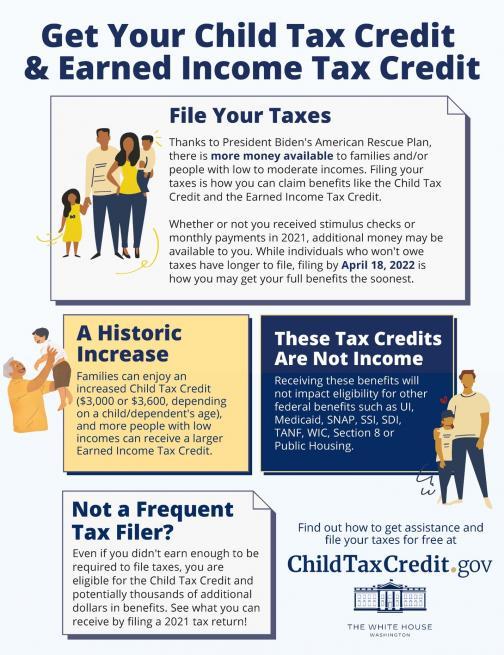

Leveraging Tax Benefits and Government Programs for Families

When managing the dual challenge of saving for a home and raising children, understanding available tax benefits and government programs can significantly lighten the load. Families can take advantage of various tax credits and deductions designed to ease financial burdens. For instance, the Child Tax Credit can reduce your tax bill, offering more room in your budget to allocate towards a down payment. Additionally, the Earned Income Tax Credit (EITC) is another valuable benefit for qualifying families, which can result in a substantial refund, further boosting your savings.

Beyond tax incentives, there are government-backed savings programs tailored to help families achieve homeownership. Programs like the First-Time Homebuyer Credit can provide significant financial support, while Individual Development Accounts (IDAs) offer matched savings plans that multiply your contributions. Consider these opportunities to maximize your savings efforts:

- Explore state-specific homebuyer assistance programs that offer grants or low-interest loans.

- Utilize 529 College Savings Plans not just for education, but to potentially reallocate funds for housing needs.

- Investigate local housing authority initiatives for additional resources and support.

By strategically leveraging these tax benefits and government programs, families can more effectively navigate the financial complexities of saving for a home while raising kids.

Building a Resilient Emergency Fund While Saving for a Home

When juggling the dual goals of purchasing a home and raising children, establishing a resilient emergency fund is crucial. This financial safety net provides peace of mind, ensuring that unexpected expenses don’t derail your larger savings objectives. Start by assessing your monthly expenses, including childcare, groceries, and utilities. Aim to set aside at least three to six months’ worth of living costs. Consider the following strategies to fortify your fund while still making progress toward your dream home:

- Automate Savings: Set up automatic transfers from your checking account to a dedicated emergency fund account. Consistency is key to building a robust safety net.

- Trim Non-Essential Expenses: Review your monthly budget for discretionary spending. Cutting back on dining out or subscription services can free up funds for both your emergency fund and home savings.

- Prioritize High-Interest Debts: Paying down high-interest debts can reduce financial stress and increase the funds available for savings.

- Utilize Windfalls Wisely: Allocate bonuses, tax refunds, or monetary gifts toward your emergency fund and home savings goals.

By taking these deliberate steps, you can build a sturdy financial foundation that supports both your family’s current needs and your future aspirations of homeownership.

{kind=link}