In today’s fast-paced financial landscape, ensuring a robust educational fund for your children or future generations is more critical than ever. As tuition fees continue to climb and educational expenses rise, crafting a well-structured education investment account becomes an essential strategy for securing academic futures without financial strain. This article will guide you through the intricacies of maximizing growth in education investment accounts, empowering you with the knowledge to make informed decisions. From selecting the right account types to optimizing your investment choices, we’ll provide you with a step-by-step approach to building a resilient and prosperous education fund. Whether you’re a seasoned investor or new to the world of financial planning, this guide will equip you with the confidence and tools necessary to achieve maximum growth in your educational investments.

Understanding Different Types of Education Investment Accounts

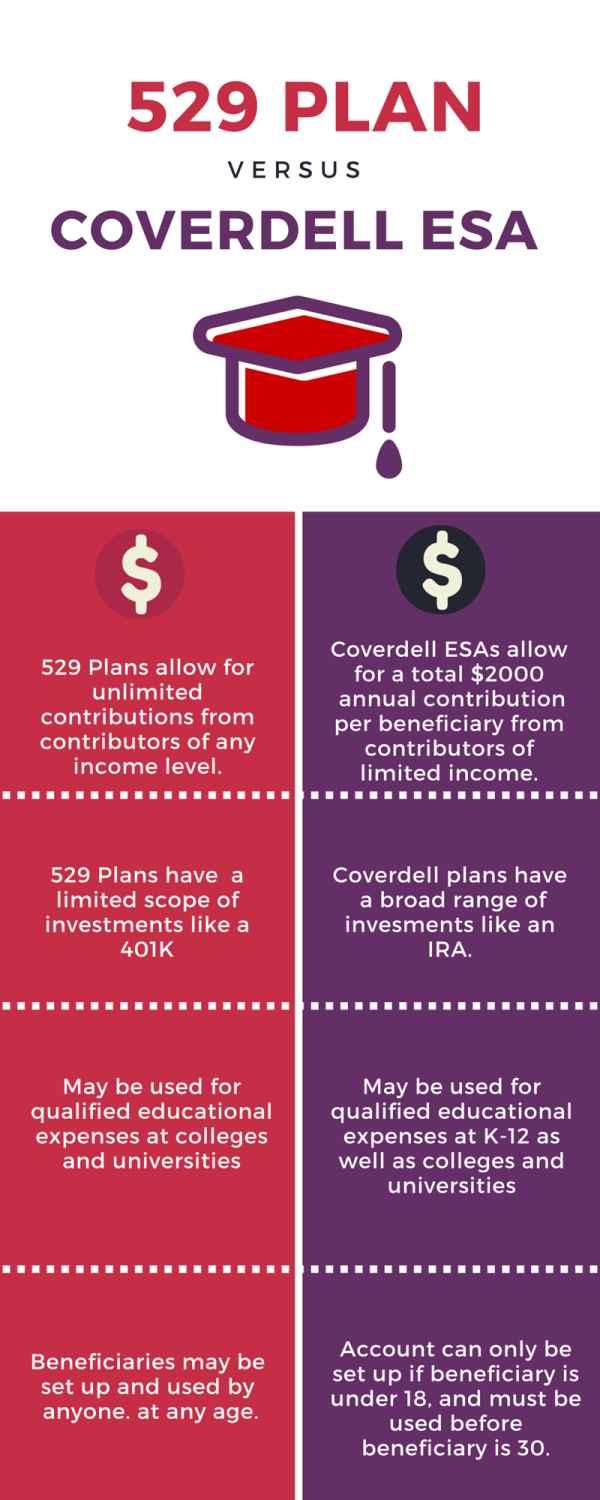

When it comes to maximizing growth in education investment accounts, understanding the distinct characteristics of each type is crucial. 529 Plans are perhaps the most popular, offering tax-free growth and withdrawals for qualified education expenses. They come in two flavors: prepaid tuition plans, which allow you to lock in current tuition rates, and education savings plans, which offer investment options similar to a 401(k). Coverdell Education Savings Accounts (ESAs) provide more flexibility in investment choices but come with contribution limits and income restrictions. These accounts also offer tax-free growth and withdrawals for education expenses, including K-12 costs.

Another option is the Custodial Accounts (UGMA/UTMA), which are not specifically designed for education but can be used for that purpose. They offer greater investment flexibility and no contribution limits, though they lack tax benefits specific to education expenses. For families who prioritize control and flexibility, these accounts might be appealing, but it’s essential to consider the potential tax implications. Understanding these options and aligning them with your financial goals can help you structure an education investment portfolio that maximizes growth while meeting future educational needs.

Choosing the Right Investment Strategy for Your Goals

Maximizing growth in education investment accounts requires aligning your strategy with specific goals. Here are some considerations to keep in mind:

- Diversification: Spread your investments across different asset classes such as stocks, bonds, and mutual funds to reduce risk and enhance potential returns.

- Time Horizon: Understand the timeline until the funds are needed. Longer horizons allow for more aggressive growth strategies, while shorter ones may necessitate a more conservative approach.

- Tax Efficiency: Take advantage of tax-advantaged accounts like 529 plans or Coverdell ESAs, which offer tax-free growth and withdrawals for qualified educational expenses.

By tailoring your investment strategy to these factors, you can effectively position your education investment accounts for optimal growth, ensuring that you meet your educational funding goals with confidence.

Optimizing Tax Benefits and Contributions

When planning for your child’s education, strategic use of investment accounts can significantly enhance both growth and tax benefits. 529 Plans are a popular choice, offering tax-free growth and withdrawals for qualified educational expenses. These plans also often allow for high contribution limits, which can be a boon for long-term growth. Consider the following strategies:

- Start Early: The earlier you begin contributing, the more time your investment has to compound.

- Maximize Contributions: Contribute the maximum allowable amount each year to take full advantage of tax benefits.

- Explore State Tax Deductions: Some states offer tax deductions for contributions to their 529 Plans, adding another layer of tax efficiency.

Coverdell Education Savings Accounts (ESAs) can also be part of your strategy. Although contributions are limited to $2,000 per year, ESAs offer flexibility in investment choices, potentially leading to higher returns. Additionally, Coverdell accounts can be used for K-12 expenses, offering a wider range of educational applications.

Monitoring and Adjusting Your Investment Portfolio for Long-Term Success

To ensure your education investment accounts are aligned for long-term success, regular monitoring and strategic adjustments are crucial. Begin by assessing your current asset allocation to ensure it matches your risk tolerance and time horizon. Diversification is key—consider spreading investments across various asset classes such as stocks, bonds, and mutual funds to mitigate risk. Utilize tools like rebalancing to maintain your desired asset mix, particularly after significant market fluctuations.

- Set Clear Goals: Define specific objectives for your investment accounts, such as target growth rates or specific educational milestones.

- Review Performance: Regularly evaluate the performance of each asset within your portfolio, focusing on both short-term gains and long-term growth.

- Stay Informed: Keep abreast of market trends and economic changes that could impact your investments, adjusting your strategy as needed.

- Leverage Tax-Advantaged Accounts: Maximize the benefits of accounts like 529 plans, which offer tax advantages for education savings.

By keeping a vigilant eye on your portfolio and making informed adjustments, you can optimize your education investment accounts for maximum growth, ensuring a stable financial foundation for future educational endeavors.

{kind=link}