In today’s unpredictable economic landscape, families are increasingly seeking robust investment strategies that can withstand the turbulence of volatile markets. With global financial systems continually affected by geopolitical tensions, economic shifts, and unexpected global events, the importance of crafting a resilient investment portfolio has never been more critical. This article delves into the best investment strategies tailored specifically for families, offering a comprehensive analysis of approaches that balance risk and reward. By examining historical trends, expert insights, and innovative financial instruments, we aim to empower families with the knowledge and confidence to navigate uncertainty, ensuring their financial security and prosperity for generations to come.

Understanding Market Volatility and Its Impact on Family Investments

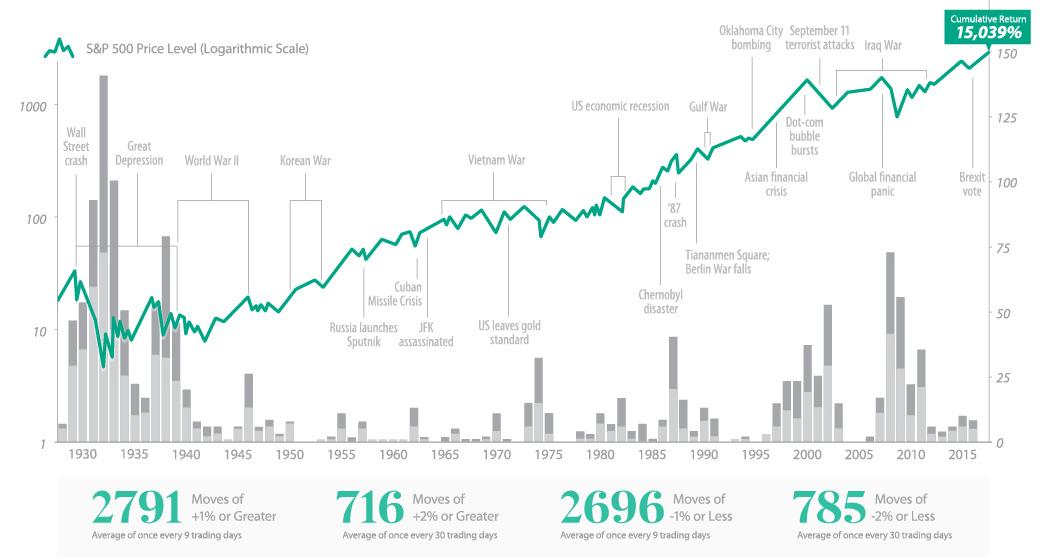

In times of market turbulence, understanding the intricate dynamics of volatility becomes crucial for families aiming to safeguard and grow their investments. Market volatility refers to the fluctuations in the market prices, which can be triggered by economic changes, political instability, or unexpected global events. For family investors, this often translates into unpredictable returns and increased anxiety. However, with the right strategies, volatility can be an ally rather than a foe.

To navigate these choppy waters, families should consider adopting a diversified portfolio that balances risk across various asset classes. Key strategies include:

- Asset Allocation: Distribute investments across stocks, bonds, and other securities to mitigate risks.

- Long-term Perspective: Focus on long-term goals and avoid knee-jerk reactions to short-term market fluctuations.

- Emergency Fund: Maintain a liquid emergency fund to avoid selling investments at a loss during downturns.

- Regular Reviews: Periodically review and adjust the portfolio to ensure alignment with changing market conditions and family goals.

By embracing these strategies, families can not only withstand market volatility but also leverage it to enhance their financial resilience and achieve their investment objectives.

Diversifying Family Portfolios for Stability and Growth

In the face of unpredictable market conditions, families seeking financial resilience should consider a diversified approach to their investment portfolios. This strategy not only cushions against market volatility but also positions the family for potential growth. A well-balanced portfolio might include a mix of stocks, bonds, and real estate, complemented by alternative investments such as commodities or hedge funds. By allocating assets across different sectors and geographies, families can mitigate risks associated with market fluctuations.

Another key element is the inclusion of income-generating assets. These can provide a steady stream of revenue even when markets are down. Consider incorporating:

- Dividend-paying stocks that offer regular payouts.

- Real estate investment trusts (REITs) for potential income and capital appreciation.

- Municipal bonds for tax-advantaged income.

Balancing growth-oriented assets with income-producing ones ensures both stability and the potential for capital growth. Regularly reviewing and adjusting the portfolio based on market conditions and family goals can further enhance financial security.

Utilizing Dollar-Cost Averaging to Mitigate Risks

In times of market turbulence, a thoughtful strategy like dollar-cost averaging (DCA) can serve as a reliable shield against volatility. This method involves investing a fixed amount of money at regular intervals, regardless of market conditions. By doing so, families can take advantage of price fluctuations and potentially lower their average cost per share over time. This approach not only removes the emotional burden of trying to time the market but also instills a disciplined investment routine.

- Consistency: Regular investments help avoid the pitfalls of emotional decision-making.

- Risk Mitigation: Buying at different price points reduces the impact of market volatility.

- Long-term Growth: Over time, DCA can smooth out the ups and downs, leading to steady portfolio growth.

By adopting dollar-cost averaging, families can focus on their long-term financial goals while reducing exposure to market volatility. This strategy ensures that investments are made systematically, providing peace of mind in an unpredictable financial landscape.

Leveraging Tax-Advantaged Accounts for Long-Term Gains

In uncertain economic climates, it becomes crucial for families to strategically utilize tax-advantaged accounts to bolster their long-term financial resilience. These accounts, such as 401(k)s, IRAs, and 529 plans, offer unique benefits that can help cushion the impact of market volatility. By maximizing contributions to these accounts, families can take advantage of tax-deferred growth or even tax-free withdrawals, depending on the type of account. This not only enhances potential returns but also provides a financial safety net in turbulent times.

Consider the following strategies to optimize these accounts for long-term gains:

- Diversification: Allocate assets across a variety of investment vehicles within your tax-advantaged accounts to reduce risk.

- Regular Contributions: Set up automatic contributions to ensure consistent growth and capitalize on dollar-cost averaging.

- Rebalancing: Periodically adjust your portfolio to maintain your desired asset allocation, especially after significant market shifts.

- Utilize Employer Matching: Take full advantage of any employer matching programs available in retirement accounts to maximize your contributions.

By thoughtfully managing these accounts, families can navigate economic uncertainties with confidence, leveraging the dual benefits of tax advantages and strategic investment practices.

{kind=link}