In today’s fast-paced financial landscape, managing multiple debts can be a daunting task. As interest rates climb and monthly payments pile up, many individuals find themselves seeking effective strategies to regain control of their financial health. One popular option that often emerges is the use of personal loans for debt consolidation. This method promises to simplify repayment processes and potentially lower interest rates, offering a streamlined path to financial freedom. However, like any financial decision, it comes with its own set of advantages and drawbacks. In this article, we will delve into the pros and cons of using personal loans for debt consolidation, equipping you with the knowledge needed to make an informed decision that aligns with your financial goals. Whether you’re struggling to keep track of multiple credit card payments or looking for a way to reduce your financial burden, understanding the intricacies of debt consolidation through personal loans is crucial in navigating your path to financial stability.

Understanding the Basics of Debt Consolidation with Personal Loans

When considering debt consolidation, personal loans can be an effective tool, offering the potential for lower interest rates and simplified payments. Key advantages of using personal loans include:

- Fixed Interest Rates: Unlike credit cards with variable rates, personal loans often come with fixed rates, providing predictability in monthly payments.

- Streamlined Payments: Consolidating multiple debts into a single loan can reduce the hassle of managing various due dates and amounts.

- Potential for Lower Costs: If you qualify for a lower interest rate, you might save money over the life of the loan compared to maintaining high-interest credit card balances.

However, it’s essential to weigh these benefits against potential drawbacks:

- Origination Fees: Some personal loans may include fees that increase the overall cost of the loan.

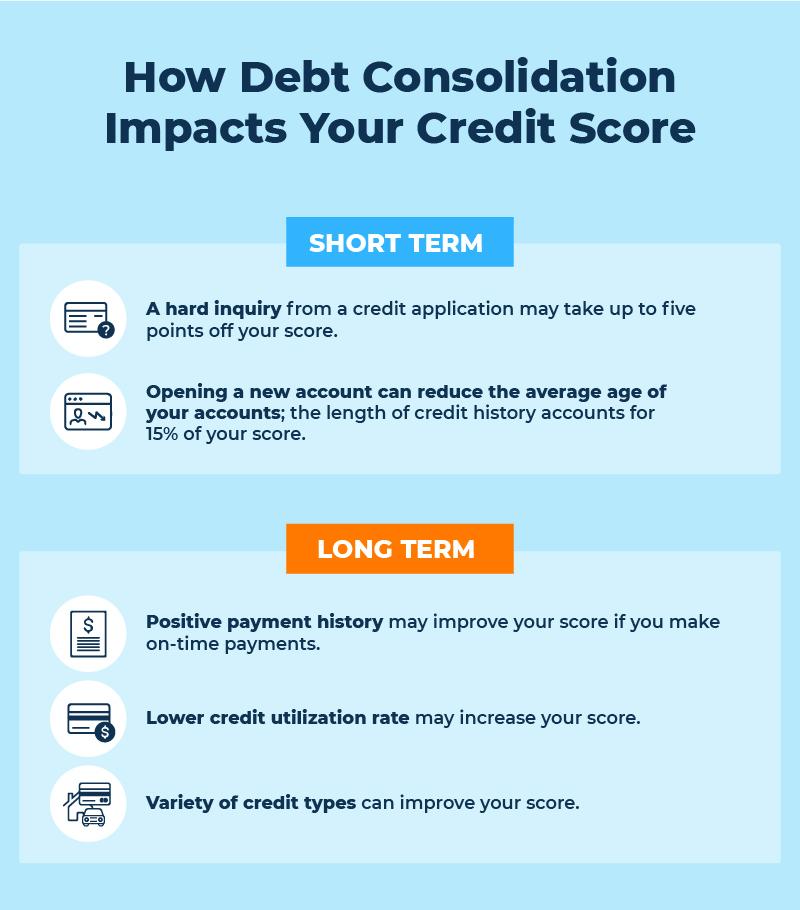

- Credit Score Impact: Applying for a new loan can result in a hard inquiry on your credit report, which might temporarily lower your credit score.

- Extended Repayment Terms: While lower monthly payments might be appealing, they could result in paying more interest over time if the loan term is significantly longer.

Analyzing the Benefits of Personal Loans for Debt Management

When it comes to managing multiple debts, personal loans can be a strategic tool to streamline finances and potentially reduce interest payments. By consolidating various high-interest debts into a single loan, individuals can benefit from a simplified repayment process and potentially lower monthly payments. This approach often comes with a fixed interest rate, which can provide a sense of stability and predictability in financial planning.

- Single monthly payment: Instead of juggling multiple due dates, you can focus on one.

- Lower interest rates: Personal loans often offer better rates compared to credit cards.

- Improved credit score: Consistent payments on a personal loan can enhance your credit history.

However, it’s crucial to weigh these benefits against potential downsides. While personal loans can reduce interest costs, they might also extend the repayment period, which could mean paying more interest over time. Moreover, if the loan is not managed wisely, there’s a risk of accumulating more debt. It’s essential to evaluate the terms carefully and ensure that the consolidation aligns with your financial goals and capabilities.

Identifying Potential Drawbacks of Personal Loans in Debt Consolidation

While personal loans can offer a streamlined path to managing multiple debts, there are several drawbacks that potential borrowers should consider. One significant issue is the possibility of higher interest rates. Personal loans often come with interest rates that may be higher than those of existing debts, particularly if your credit score isn’t stellar. This can result in paying more over the life of the loan, negating the benefits of consolidation.

Another concern is the origination fees that can accompany personal loans. These fees, typically a percentage of the loan amount, can add an unexpected cost to your consolidation plan. Additionally, if you’re not careful, consolidating debts into one loan might lead to a longer repayment period, which could mean you’re in debt for a longer time, even if the monthly payments are reduced. It’s crucial to read the fine print and ensure that the terms of the loan truly align with your financial goals.

Expert Recommendations for Effectively Using Personal Loans to Consolidate Debt

Leveraging personal loans for debt consolidation can be a savvy financial strategy when done correctly. Experts suggest that before committing to a personal loan, you should thoroughly evaluate your current debt situation. This includes understanding the total amount you owe, the interest rates of your existing debts, and your repayment capacity. Here are some key recommendations to consider:

- Calculate Total Costs: Make sure to account for any origination fees or prepayment penalties that could offset the savings from a lower interest rate.

- Review Loan Terms: Carefully read through the terms and conditions of the loan. Look for flexible repayment options and ensure there are no hidden fees.

- Compare Interest Rates: Seek out loans with the lowest possible interest rate. This will reduce the overall cost of the debt over time.

- Consider Credit Impact: While personal loans can initially cause a slight dip in your credit score, timely repayments can ultimately boost your credit rating.

- Stick to a Budget: Use this opportunity to create a realistic budget to avoid accumulating new debt.

Consulting with a financial advisor can also provide personalized insights and help ensure that consolidating your debt with a personal loan aligns with your long-term financial goals.

{kind=link}