Graduating from college is an exhilarating milestone, marking the beginning of a new chapter filled with opportunities and potential. However, alongside the excitement often comes the daunting reality of managing student loans and other financial obligations. Navigating the world of debt management can seem overwhelming, but with the right strategies, it is entirely manageable. This article aims to empower recent graduates with practical, effective tips for taking control of their financial future. By implementing these proven strategies, you can confidently tackle your debt, paving the way for a secure and prosperous post-graduation life. Let’s dive into the best practices for transforming your financial outlook and achieving lasting financial health.

Understanding Your Debt Landscape

Graduating is a significant milestone, but it often comes with the challenge of managing accumulated debt. To effectively navigate this financial landscape, start by taking a comprehensive inventory of your debt. Identify the types of debt you have, such as student loans, credit card balances, or personal loans. List each debt with details like interest rates, minimum payments, and due dates. This clarity is crucial in formulating a plan tailored to your financial situation.

Consider organizing your debts using a spreadsheet or a debt management app. This can help you visualize your obligations and prioritize them. Here are some strategies to get started:

- Snowball Method: Focus on paying off the smallest debts first to gain momentum and build confidence.

- Avalanche Method: Target the debt with the highest interest rate to minimize overall interest payments.

- Consolidation: Explore consolidating multiple debts into one to simplify payments and potentially lower interest rates.

- Automate Payments: Set up automatic payments to avoid late fees and maintain a consistent payment schedule.

By understanding and organizing your debt, you empower yourself to take control and work towards financial freedom.

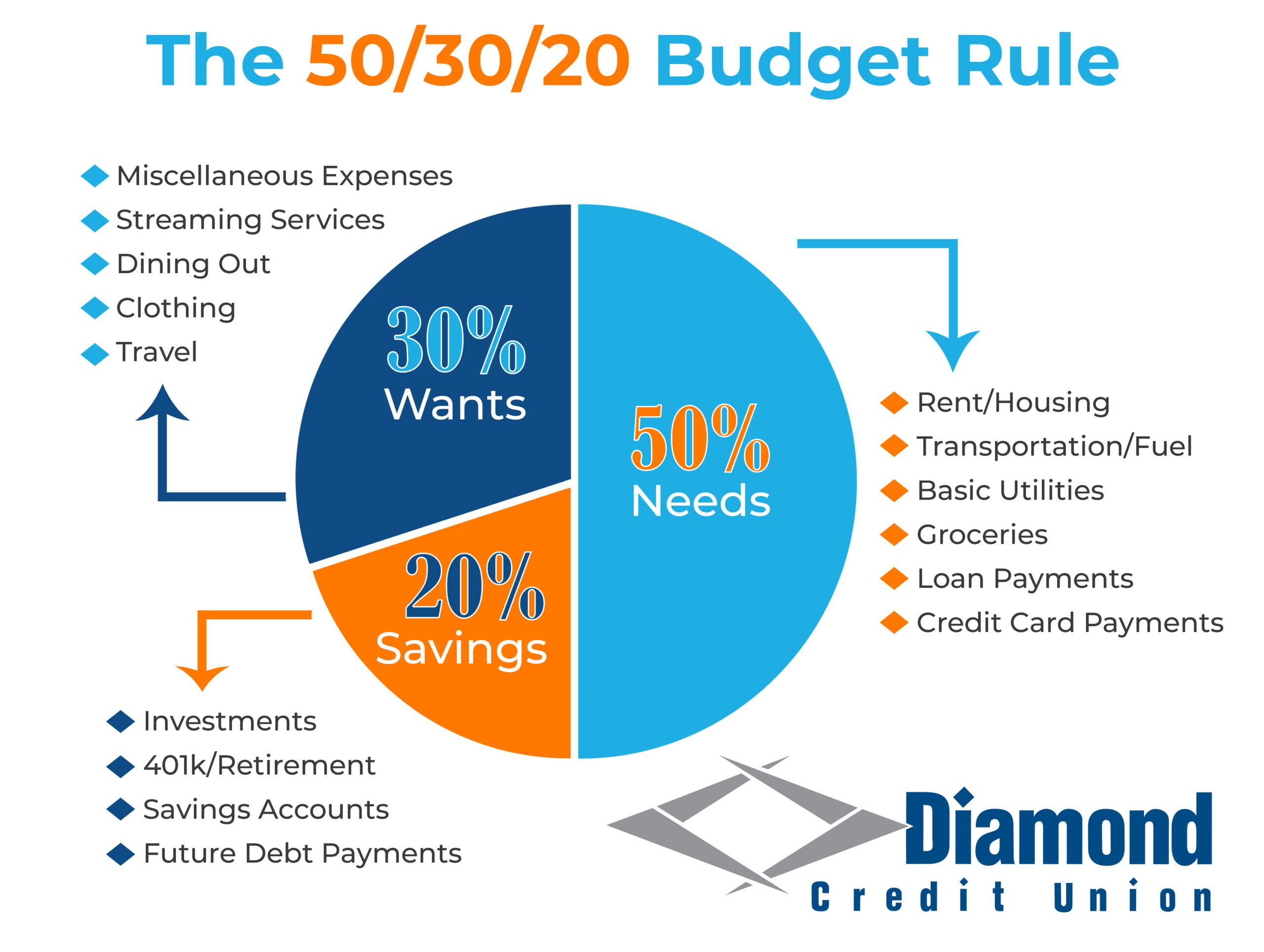

Crafting a Realistic Budget

Creating a budget that mirrors your financial reality is a vital step in managing debt effectively after graduation. Begin by listing all your sources of income, such as your salary, any side gigs, or passive income streams. Then, itemize your expenses to see where your money is going. This includes fixed costs like rent, utilities, and loan payments, as well as variable expenses such as groceries, entertainment, and dining out. The key is to be honest with yourself about your spending habits.

- Track every dollar: Use budgeting apps or spreadsheets to keep a detailed account of your expenses.

- Identify non-essential spending: Look for areas where you can cut back without sacrificing your quality of life.

- Allocate funds for debt repayment: Prioritize paying off high-interest debts to save money in the long run.

Remember, a realistic budget is not about restricting your lifestyle but about making informed decisions that align with your financial goals. With discipline and consistency, you’ll find yourself gaining control over your finances and reducing debt stress.

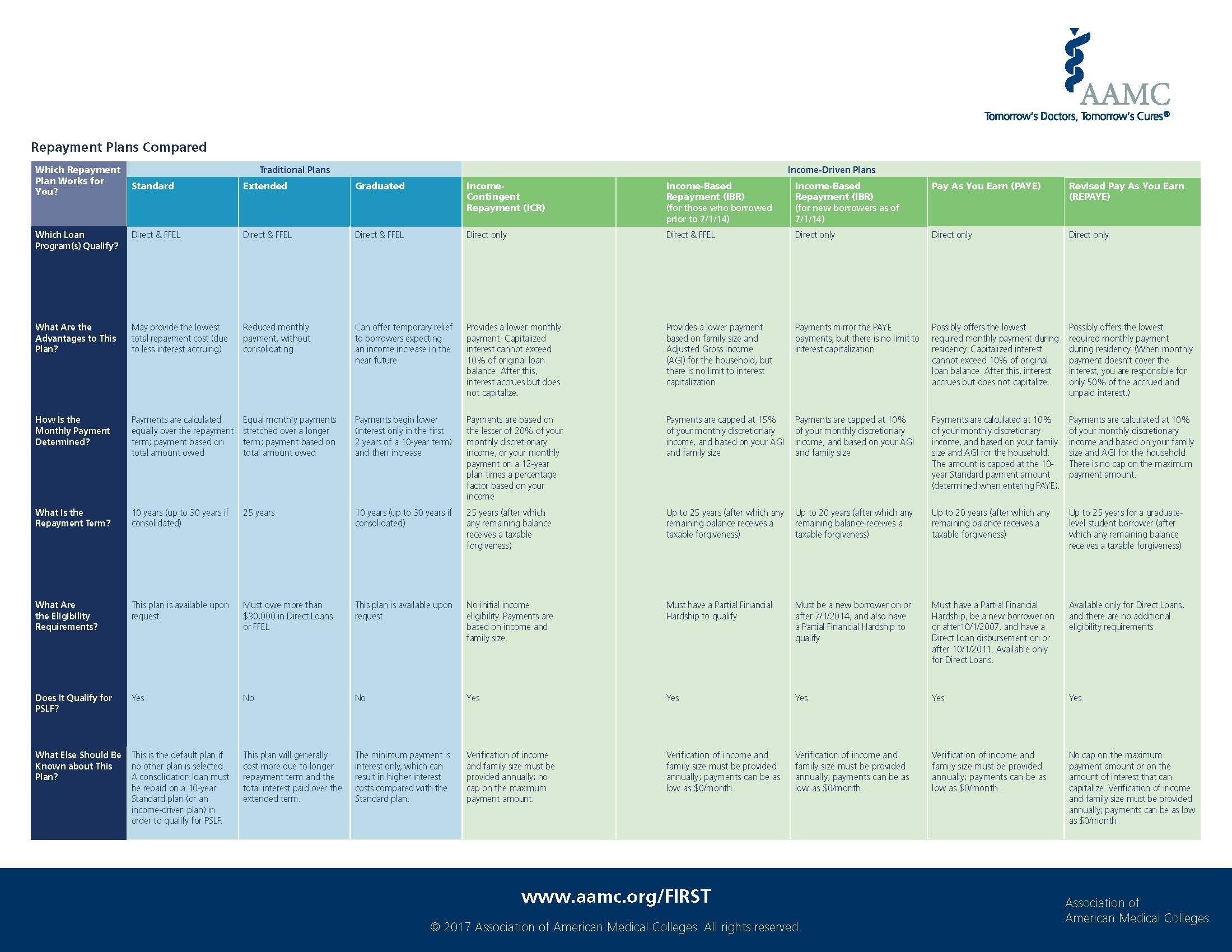

Exploring Repayment Options

After graduation, one of the key steps in managing your debt effectively is understanding and exploring various repayment options. This involves evaluating different plans to find the one that best aligns with your financial situation and goals. Here are some strategies to consider:

- Income-Driven Repayment Plans: These plans adjust your monthly payments based on your income and family size. They can significantly reduce your payments, especially in the early stages of your career when your income might be lower.

- Refinancing: By refinancing your student loans, you may secure a lower interest rate, which can save you money over the life of the loan. Be sure to compare offers from multiple lenders to find the best rate.

- Loan Forgiveness Programs: Investigate whether you qualify for any loan forgiveness programs. Certain careers, such as public service or teaching, may offer forgiveness after a set number of years of qualifying payments.

- Deferment or Forbearance: If you’re facing financial hardship, these options allow you to temporarily pause or reduce your payments. However, interest may continue to accrue, so use them cautiously.

By taking the time to explore these options, you can develop a repayment strategy that minimizes stress and maximizes your financial well-being. Remember, choosing the right plan is crucial to staying on top of your debt while paving the way for a secure financial future.

Building a Strong Financial Future

After graduation, managing debt can seem daunting, but with the right strategies, it’s entirely manageable. The key is to stay organized and proactive. Start by creating a detailed budget that includes all your income and expenses. This will help you track where your money is going and identify areas where you can cut back. Remember, it’s essential to prioritize your debts by focusing on those with the highest interest rates first, as this will save you money in the long run.

- Consolidate your loans if possible, as this can simplify payments and potentially lower your interest rate.

- Consider setting up automatic payments to avoid late fees and improve your credit score over time.

- Explore income-driven repayment plans if your federal student loan payments are too high relative to your income.

- Take advantage of any employer benefits that offer student loan repayment assistance.

Lastly, building an emergency fund should be a priority, even while paying off debt. This fund will serve as a financial cushion in case of unexpected expenses, preventing you from accumulating more debt. Stay disciplined, review your financial plan regularly, and adjust as necessary to ensure you’re on track to achieving a stable and prosperous financial future.

{kind=link}