In the ever-evolving landscape of personal finance, building a robust retirement fund is a cornerstone of long-term financial security. As individuals navigate through their careers, the importance of strategic planning for retirement cannot be overstated. With an array of investment options and strategies available, understanding how to effectively grow and safeguard your nest egg is crucial. This article delves into proven long-term investment strategies that can help you construct a resilient retirement fund, ensuring financial independence and peace of mind in your golden years. Whether you’re just starting your career or are a seasoned professional, these insights will empower you to make informed decisions, aligning your investments with your retirement goals and risk tolerance.

Understanding the Importance of Diversification in Your Retirement Portfolio

When planning for a robust retirement fund, one of the most critical strategies to consider is diversification. By spreading your investments across various asset classes, you can effectively manage risk and improve the potential for long-term returns. Diversification acts as a financial safety net, helping to cushion your portfolio against market volatility. A well-diversified retirement portfolio might include:

- Stocks: Equities offer the potential for high returns, but they also come with higher risk. Balancing your stock investments across different sectors and geographies can mitigate some of this risk.

- Bonds: Known for being more stable than stocks, bonds provide a reliable income stream and can help balance out the volatility of equities.

- Real Estate: Investing in property or real estate funds can provide steady income and capital appreciation, acting as a hedge against inflation.

- Commodities: Assets like gold or oil can diversify your portfolio further, offering protection against inflation and economic downturns.

- Mutual Funds/ETFs: These investment vehicles allow you to pool your resources with others to invest in a diversified portfolio, managed by professionals.

By including a mix of these assets, you ensure that your retirement portfolio is not overly reliant on any single investment, reducing the risk of significant losses. Remember, the goal is to balance risk and reward, securing a stable financial future that withstands the test of time.

Crafting a Balanced Asset Allocation to Minimize Risks

When it comes to establishing a solid foundation for your retirement fund, understanding the nuances of asset allocation is paramount. A well-crafted allocation strategy is not just about spreading your investments across different asset classes; it’s about achieving a harmonious balance that aligns with your risk tolerance and financial goals. Diversification is the cornerstone of minimizing risks, as it ensures that the performance of one asset doesn’t overly influence your entire portfolio. Consider the following principles to guide your allocation strategy:

- Equities for Growth: Allocate a portion to stocks, which typically offer higher returns over the long term, though they come with increased volatility. Adjust your exposure based on your risk appetite and investment horizon.

- Bonds for Stability: Bonds can provide a steady income stream and act as a buffer against the volatility of equities. Incorporate a mix of government and corporate bonds to balance risk and return.

- Real Assets for Inflation Hedge: Real estate and commodities can protect against inflation and add another layer of diversification. Evaluate their inclusion based on market conditions and personal investment strategy.

- Cash for Liquidity: Maintaining a cash reserve can help manage short-term needs and mitigate the impact of market downturns, ensuring you don’t have to liquidate assets at an inopportune time.

By thoughtfully considering each component and regularly reviewing your portfolio, you can craft an asset allocation that not only seeks growth but also safeguards against potential market downturns, ultimately paving the way for a robust retirement fund.

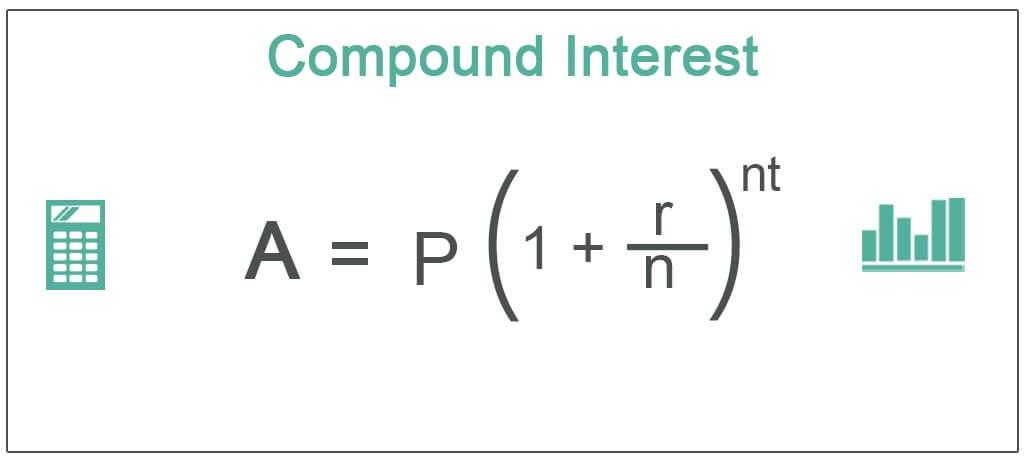

Harnessing the Power of Compound Interest for Long-term Growth

One of the most powerful tools in building a substantial retirement fund is compound interest. This financial phenomenon works by earning interest on both the initial principal and the accumulated interest from previous periods, effectively making your money work for you over time. The longer you allow your investments to compound, the more exponential your growth can become, thanks to the “snowball effect” of reinvested earnings.

- Start Early: The earlier you begin investing, the more time your money has to grow. Even small, regular contributions can lead to significant growth over decades.

- Reinvest Dividends: Opt to reinvest dividends rather than taking them as cash. This increases the amount of money that is compounding over time.

- Choose High-Quality Investments: Look for investments with a strong track record of growth and stability. High-quality stocks, bonds, and mutual funds can offer reliable returns.

- Stay Consistent: Regularly contribute to your investment portfolio, regardless of market conditions. This discipline helps to harness the full potential of compounding.

By strategically leveraging compound interest, you can build a robust retirement fund that grows more powerful with each passing year, securing your financial future with confidence.

Identifying and Avoiding Common Pitfalls in Retirement Investing

When planning for retirement, it’s crucial to be aware of the common mistakes that can derail your investment journey. Avoiding high fees is a critical step. Investment products often come with hidden costs that can eat into your returns over time. Always read the fine print and compare expense ratios to ensure you’re not paying more than necessary. Over-concentration in one asset class is another pitfall. Diversifying your portfolio helps mitigate risk and ensures you’re not overly reliant on the performance of a single market sector.

- Emotional decision-making: Market volatility can tempt investors to make impulsive decisions. Stick to your strategy and avoid knee-jerk reactions.

- Ignoring inflation: Failing to account for inflation can erode your purchasing power. Consider inflation-protected securities or assets that traditionally outpace inflation.

- Underestimating longevity: People are living longer, and your savings need to last. Plan for a longer retirement to avoid running out of funds.

By staying vigilant and avoiding these common errors, you can enhance the likelihood of building a robust retirement fund.

{kind=link}