In an ever-evolving financial landscape, building and sustaining wealth for your family is both a strategic challenge and a rewarding opportunity. Among the myriad of investment avenues available, real estate and stocks stand out as two of the most robust vehicles for wealth creation. This article delves into the analytical intricacies of leveraging these powerful tools to secure your family’s financial future. By examining historical trends, current market dynamics, and expert insights, we will uncover actionable strategies to maximize returns and minimize risks. Whether you’re a seasoned investor or just starting your wealth-building journey, this guide aims to equip you with the knowledge and confidence to make informed decisions that align with your family’s long-term financial goals. Through a balanced approach that considers both asset classes, we will explore how to construct a diversified portfolio that not only withstands economic fluctuations but also thrives in an unpredictable world.

Maximizing Family Wealth Through Strategic Real Estate Investments

In the dynamic world of wealth-building, strategic real estate investments stand out as a robust pillar for securing and enhancing family wealth. To make the most of this opportunity, it’s crucial to focus on several key strategies. First, diversification is paramount; don’t put all your eggs in one basket. By investing in various types of properties, such as residential, commercial, and vacation rentals, you can mitigate risks and capitalize on different market trends.

Another vital approach is leveraging the power of location. Investing in properties in emerging neighborhoods or cities with growth potential can yield substantial returns. Keep an eye on factors like local employment rates, infrastructure developments, and population growth. Furthermore, consider the tax advantages associated with real estate investments. Many regions offer incentives such as tax deductions on mortgage interest, property taxes, and depreciation, which can significantly enhance your net returns.

- Prioritize properties with potential for appreciation.

- Utilize rental income to cover expenses and generate cash flow.

- Regularly review and adjust your investment portfolio to align with market changes.

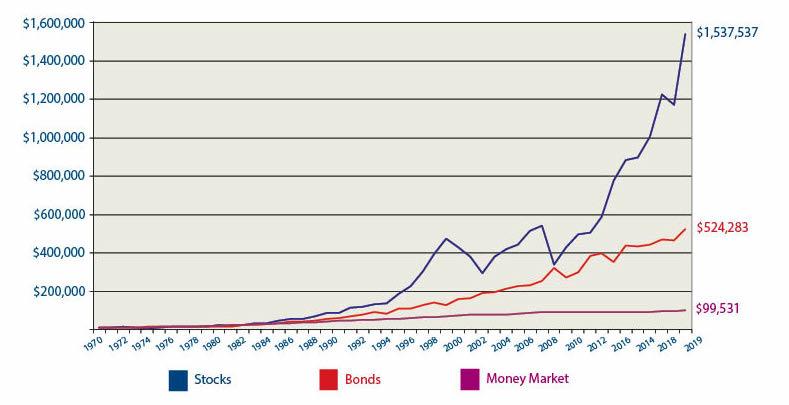

Harnessing the Power of Stock Market Growth for Long-Term Financial Security

Understanding the dynamics of stock market growth is crucial for securing a robust financial future. With strategic investments, you can harness the compounding power of the market to build wealth over time. Here are some key strategies to consider:

- Diversification: Spreading investments across different sectors and asset classes can reduce risk and enhance returns.

- Long-Term Focus: Embrace a buy-and-hold strategy to benefit from the market’s long-term upward trend.

- Regular Contributions: Consistently invest a portion of your income to take advantage of dollar-cost averaging.

- Reinvestment: Reinvest dividends and capital gains to accelerate growth and compound interest.

By implementing these strategies, you can create a resilient portfolio that not only grows with the market but also provides a safety net for your family’s future. This disciplined approach to investing not only helps mitigate short-term volatility but also positions you to capitalize on the market’s long-term potential.

Balancing Risk and Reward: Diversifying Your Familys Investment Portfolio

When it comes to building a robust investment portfolio for your family, striking the right balance between risk and reward is crucial. Diversification is the key strategy here, allowing you to mitigate risks while maximizing potential returns. By investing in both real estate and stocks, you can create a portfolio that benefits from the unique advantages each asset class offers. Real estate provides tangible assets and potential rental income, offering a degree of stability and long-term appreciation. Stocks, on the other hand, offer liquidity and the potential for high growth, especially when investing in a mix of sectors and market caps.

- Real Estate: Consider a mix of residential and commercial properties. Rental properties can generate steady cash flow, while REITs (Real Estate Investment Trusts) offer a way to invest in real estate without direct property management.

- Stocks: Diversify across industries and geographies. Include blue-chip stocks for stability and growth stocks for higher potential returns. Don’t overlook emerging markets and sectors like technology and healthcare for added growth opportunities.

By thoughtfully diversifying across these asset classes, you ensure that your family’s financial future is secured, with a balanced approach that accommodates both steady income and capital appreciation. This strategy not only helps in weathering market volatility but also in seizing opportunities for wealth accumulation over time.

Implementing Tax-Efficient Strategies to Preserve and Grow Family Assets

Preserving and growing family assets requires strategic planning, especially in the realm of taxes. By adopting tax-efficient strategies, families can maximize their wealth potential while minimizing liabilities. Diversification plays a crucial role in this process. Balancing investments between real estate and stocks can provide substantial tax benefits and create a robust financial portfolio. For instance, real estate investments offer depreciation benefits, which can significantly reduce taxable income. Meanwhile, holding stocks for the long term can take advantage of capital gains tax rates, which are typically lower than ordinary income tax rates.

To further enhance tax efficiency, consider the following strategies:

- Utilize Tax-Deferred Accounts: Leverage retirement accounts such as IRAs and 401(k)s to defer taxes on stock investments.

- Engage in 1031 Exchanges: For real estate, use 1031 exchanges to defer capital gains taxes by reinvesting proceeds from a property sale into a similar investment.

- Harvest Tax Losses: Offset capital gains with losses from other investments, effectively reducing taxable income.

These strategies, when implemented effectively, not only safeguard family wealth from excessive tax burdens but also position the family to capitalize on growth opportunities in both the real estate and stock markets.

{kind=link}