As you approach retirement, the prospect of enjoying your golden years is often accompanied by the reality of rising healthcare costs. With longer life expectancies and the increasing complexity of medical needs, planning for healthcare expenses has never been more critical. However, by taking proactive steps and implementing strategic financial measures, you can effectively manage these costs and secure your peace of mind. In this guide, we will explore the best ways to prepare for healthcare expenses during retirement, empowering you with the knowledge and tools necessary to safeguard your financial future. From understanding insurance options to optimizing savings strategies, this article will equip you with the confidence to navigate the financial challenges of healthcare in retirement with ease and assurance.

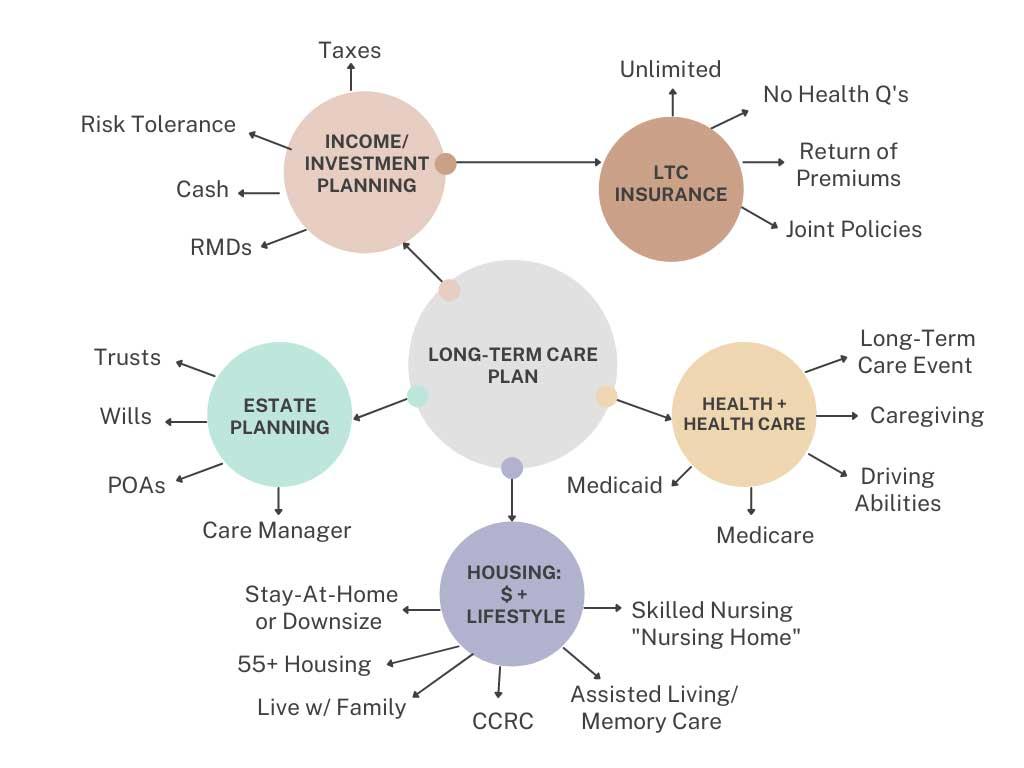

Understanding Future Healthcare Needs and Costs

As we age, healthcare needs evolve, often becoming more complex and costly. Understanding these future requirements is crucial for effective financial planning. Begin by evaluating your current health status and family medical history to anticipate potential health issues. Consider the increasing prevalence of chronic conditions and the likelihood of requiring long-term care services. These factors can significantly impact your healthcare expenses in retirement.

- Research Medicare and Supplemental Insurance: Explore different plans and what they cover to avoid unexpected out-of-pocket costs.

- Consider Health Savings Accounts (HSAs): Maximize contributions to these tax-advantaged accounts if eligible, as they can be used for a wide range of medical expenses.

- Invest in Preventive Care: Regular check-ups and a healthy lifestyle can help mitigate future health issues, potentially reducing costs.

- Plan for Inflation: Medical costs tend to rise faster than general inflation, so ensure your savings strategy accounts for this trend.

By taking these steps, you can create a robust plan that not only addresses your healthcare needs but also safeguards your financial well-being in retirement.

Creating a Comprehensive Healthcare Savings Strategy

In crafting a robust financial plan for your golden years, one crucial element to prioritize is addressing future medical expenses. With healthcare costs on a consistent upward trajectory, it’s essential to employ strategic measures to safeguard your retirement savings. Begin by diversifying your savings portfolio. This can involve a mix of Health Savings Accounts (HSAs), traditional savings, and investments in low-risk bonds or mutual funds, specifically tailored to cover medical needs. An HSA, for instance, not only offers tax advantages but also allows you to accumulate funds over time, growing into a substantial resource for future healthcare expenditures.

Consider implementing the following strategies to fortify your healthcare savings plan:

- Maximize your HSA contributions: Aim to contribute the maximum allowable amount each year to capitalize on tax-free growth and withdrawals for qualified medical expenses.

- Invest in long-term care insurance: This can help mitigate the high costs associated with prolonged medical care, providing peace of mind for both you and your family.

- Regularly review and adjust your plan: Healthcare needs can change over time; hence, it’s vital to periodically reassess your plan to ensure it aligns with your current and anticipated future needs.

- Explore Medicare and supplemental options: Understand the coverage and limitations of Medicare, and consider supplemental insurance to fill any gaps, ensuring comprehensive coverage.

By proactively addressing these areas, you can build a resilient strategy that protects your financial health as you navigate retirement.

Exploring Insurance Options for Enhanced Coverage

When preparing for retirement, it’s crucial to assess your insurance options to ensure you have comprehensive coverage that adapts to the ever-increasing healthcare costs. Start by evaluating your current health insurance policy and consider whether it will suffice in the long run. Medicare is a popular choice for retirees, but it may not cover all your needs. You might want to look into Medicare Advantage Plans or Medigap policies, which can offer additional benefits like dental, vision, or even wellness programs. These options can provide a financial cushion against unexpected medical expenses, ensuring your peace of mind.

Furthermore, think about the potential need for long-term care insurance. As longevity increases, so does the likelihood of requiring extended care, which traditional health insurance plans typically don’t cover. Investigate policies that offer flexible benefits and consider partnerships with health savings accounts (HSAs) or retirement health savings plans to set aside funds specifically for healthcare. Here are some steps to enhance your coverage:

- Review your current health insurance plan for any coverage gaps.

- Explore supplemental insurance options that align with your future needs.

- Consider the role of health savings accounts in funding medical expenses.

- Consult with a financial advisor to tailor a plan that suits your retirement goals.

Maximizing Benefits from Government and Employer Programs

Leveraging government and employer programs can significantly ease the burden of healthcare expenses during retirement. Start by exploring Medicare and its various plans. Medicare Part A covers hospital services, while Part B takes care of outpatient care and preventive services. To fill in any gaps, consider Medicare Supplement Insurance (Medigap) or Medicare Advantage Plans (Part C). These options can help cover costs not included in standard Medicare, such as copayments and deductibles.

Don’t overlook the potential benefits from employer-sponsored programs. Many employers offer Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). These accounts allow you to save pre-tax dollars specifically for healthcare expenses. Additionally, check if your employer provides any retiree health benefits or access to group health insurance plans post-retirement. By effectively utilizing these programs, you can strategically manage and reduce out-of-pocket expenses, ensuring a financially secure retirement.

- Medicare Part A and B – Basic hospital and outpatient coverage.

- Medicare Supplement Insurance – Fills coverage gaps in traditional Medicare.

- Employer-Sponsored HSAs and FSAs – Tax-advantaged savings for medical expenses.

- Retiree Health Benefits – Additional coverage options from past employers.

{kind=link}