Retirement marks the beginning of a new chapter in life, offering the freedom to pursue passions, travel, and enjoy well-earned leisure time. However, ensuring that your retirement savings last throughout this chapter requires strategic planning and informed decision-making. In this guide, we will explore proven strategies and practical tips to help you manage your nest egg effectively, ensuring financial security and peace of mind for the rest of your life. With a confident approach and the right tools, you can navigate the complexities of retirement finance and make the most of your golden years. Whether you’re on the cusp of retirement or already enjoying it, this article will equip you with the knowledge to safeguard your financial future.

Understanding Your Retirement Needs

Planning for retirement involves more than just saving money; it’s about comprehensively understanding your future needs to ensure a financially secure and fulfilling retirement. Consider these key areas to assess your retirement requirements:

- Healthcare Costs: As you age, healthcare expenses can increase significantly. Factor in costs for insurance premiums, medications, and potential long-term care.

- Living Expenses: Evaluate your current lifestyle and consider how it might change. Think about housing, utilities, and daily living costs.

- Leisure and Travel: Retirement is a time to enjoy life. Budget for hobbies, travel plans, and any other leisure activities you plan to pursue.

- Inflation: Over time, the cost of living will rise. Ensure your savings account for inflation to maintain purchasing power.

- Emergency Fund: Life is unpredictable. Set aside funds for unexpected expenses to avoid dipping into your retirement savings.

By thoroughly evaluating these aspects, you can create a tailored retirement plan that aligns with your personal goals and lifestyle, ensuring your savings are well-prepared to support you throughout your retirement years.

Crafting a Sustainable Withdrawal Strategy

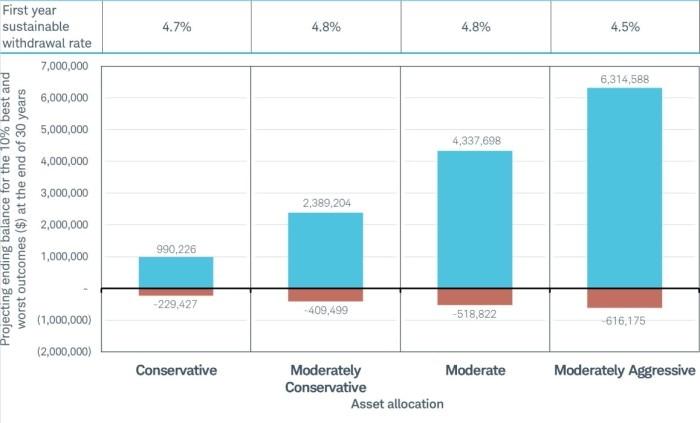

Developing a withdrawal plan that aligns with your retirement goals while ensuring the longevity of your savings requires strategic foresight and adaptability. Begin by understanding your expected expenses, including essentials like housing and healthcare, as well as discretionary spending on hobbies and travel. It’s crucial to distinguish between these to prioritize effectively. Many retirees adopt the 4% rule as a guideline, withdrawing 4% of their portfolio annually, but this might not suit everyone. Consider customizing this approach based on market conditions and personal circumstances.

- Diversify your investment portfolio to balance growth and stability.

- Adjust withdrawals based on market performance to preserve capital during downturns.

- Reassess your plan annually to accommodate changes in lifestyle and financial markets.

Incorporating a mix of guaranteed income sources, such as annuities or Social Security, with your investments can provide a safety net against market volatility. Always be prepared to adapt your strategy as life expectancy, inflation rates, and healthcare needs evolve. This dynamic approach not only safeguards your savings but also empowers you to enjoy a fulfilling retirement.

Investing Wisely for Long-Term Growth

When planning for the future, it’s crucial to focus on strategies that ensure your retirement savings grow steadily over time. To achieve this, consider diversifying your investment portfolio. A well-rounded mix of asset classes can help mitigate risks and maximize returns. Include a blend of:

- Stocks: While they can be volatile, stocks historically offer higher returns compared to other asset types.

- Bonds: These provide stability and regular income, balancing the riskier elements of your portfolio.

- Real Estate: Investing in property can offer both rental income and potential appreciation in value.

- Mutual Funds or ETFs: These provide instant diversification and professional management.

Regularly reviewing and rebalancing your portfolio is equally important. As market conditions change, the asset allocation that once suited your goals might need adjustments. Rebalancing helps maintain your desired risk level and keeps your investments aligned with your long-term objectives. Remember, the key is consistency and staying informed, ensuring that your retirement nest egg remains robust and resilient throughout your golden years.

Adapting to Economic Changes and Life Events

In today’s ever-shifting financial landscape, it’s crucial to be proactive and flexible with your retirement savings strategy. Economic fluctuations and unexpected life events can significantly impact your financial security, but with the right approach, you can navigate these changes smoothly. Consider diversifying your investments to mitigate risk and explore various income streams. Regularly reviewing your portfolio and adjusting your asset allocation can help you stay aligned with your long-term goals.

Moreover, adapting to life events such as health changes, family responsibilities, or even relocation requires careful planning. Here are some strategies to ensure your retirement savings remain robust:

- Emergency Fund: Maintain a dedicated fund to cover unexpected expenses, reducing the need to dip into retirement savings.

- Healthcare Planning: Account for potential healthcare costs by investing in long-term care insurance or health savings accounts.

- Downsizing: Consider reducing living expenses by downsizing your home or relocating to a more cost-effective area.

By being adaptable and informed, you can safeguard your retirement savings against economic and personal shifts, ensuring a financially secure future.

{kind=link}