As you chart the course toward a financially secure retirement, maximizing your Individual Retirement Account (IRA) contributions can serve as a powerful strategy to enhance your savings. With the right approach, you can take full advantage of the tax benefits and growth potential that IRAs offer, ensuring a more comfortable and rewarding retirement. In this guide, we’ll walk you through essential tips and strategies to maximize your IRA contributions effectively. From understanding annual limits and catch-up contributions to exploring different types of IRAs and optimizing your investment choices, you’ll gain the knowledge and confidence needed to supercharge your retirement savings. Whether you’re just starting out or nearing retirement, these insights will empower you to make informed decisions and secure a prosperous future.

Understanding IRA Contribution Limits and Opportunities

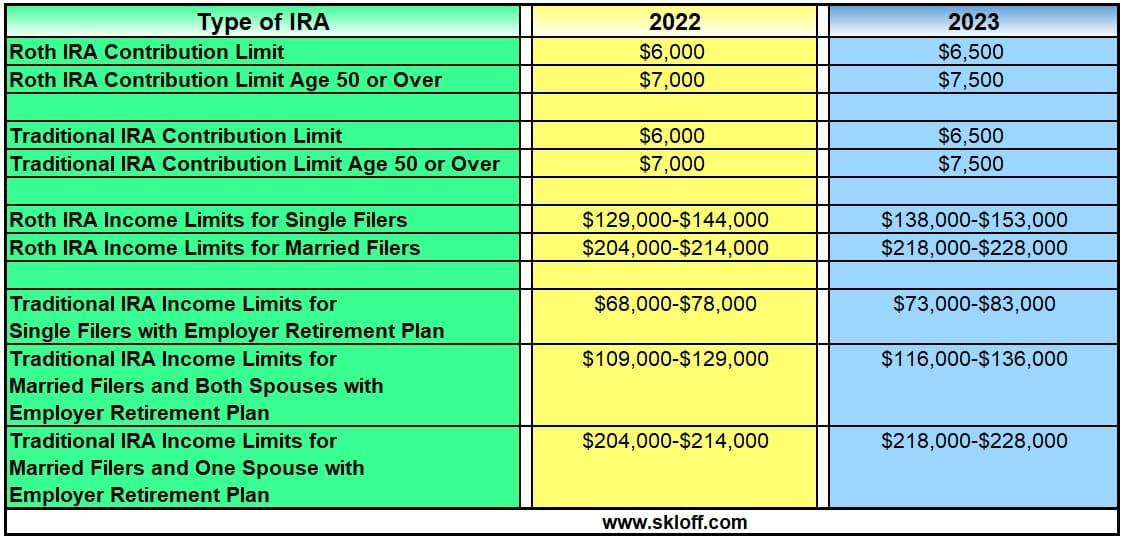

When it comes to maximizing your Individual Retirement Account (IRA) contributions, understanding the annual limits and leveraging available opportunities is crucial. Each year, the IRS sets contribution limits for IRAs, and staying informed about these caps can significantly impact your retirement savings strategy. For 2023, the maximum contribution limit for those under 50 is $6,500, while individuals aged 50 and over can contribute an additional $1,000 as a “catch-up” contribution. It’s essential to contribute the maximum amount allowed if your financial situation permits, as this can enhance the growth potential of your retirement fund through the power of compounding.

To make the most of your IRA contributions, consider the following strategies:

- Start Early: The earlier you start contributing, the more time your investments have to grow.

- Automate Contributions: Set up automatic transfers to your IRA to ensure consistent contributions.

- Re-evaluate Annually: Review your financial situation each year to adjust your contribution amount, taking advantage of any increases in limits.

- Utilize Catch-Up Contributions: If you are 50 or older, make use of the additional contribution room to boost your savings.

By strategically planning your contributions and staying informed about the limits, you can effectively maximize your IRA and set yourself up for a more secure retirement.

Strategic Timing for IRA Contributions to Maximize Growth

One of the most effective strategies for maximizing your IRA contributions is to time your deposits strategically throughout the year. Contributing early in the tax year can allow your investments more time to compound, potentially leading to greater growth by the time you retire. By front-loading your contributions, you give your investments the opportunity to take advantage of market gains throughout the year. This method is especially beneficial during bullish market periods, where earlier contributions can compound on top of initial market growth.

- Early Contributions: Make your full or partial contributions at the beginning of the year to benefit from compound growth.

- Dollar-Cost Averaging: If contributing a lump sum isn’t feasible, consider setting up automatic monthly contributions to spread your investment over time, reducing the impact of market volatility.

- Reevaluate Annually: Regularly review your financial situation to adjust your contribution strategy, ensuring you’re maximizing potential growth while staying within budget.

Choosing Between Traditional and Roth IRAs for Optimal Benefits

When deciding which type of IRA to contribute to, understanding the key differences between Traditional and Roth IRAs is crucial for maximizing your retirement savings. Both options offer unique benefits tailored to different financial situations and future plans.

Traditional IRA:

- Contributions may be tax-deductible, potentially lowering your taxable income for the year.

- Taxes are deferred until withdrawal, allowing investments to grow tax-free.

- Ideal if you expect to be in a lower tax bracket during retirement.

Roth IRA:

- Contributions are made with after-tax dollars, offering tax-free growth and withdrawals.

- No required minimum distributions (RMDs) during the account holder’s lifetime, providing more flexibility.

- Beneficial if you anticipate being in a higher tax bracket in the future or want tax-free income during retirement.

Strategic Considerations:

- Income Level: Consider your current and expected future tax brackets.

- Age and Retirement Plans: Younger individuals with lower income might benefit more from Roth IRAs, while those nearing retirement might prefer the immediate tax benefits of a Traditional IRA.

- Diversification: Some savers choose to contribute to both types of IRAs to balance tax benefits now and in retirement.

Leveraging Catch-Up Contributions for Enhanced Retirement Savings

As you approach the golden years, the opportunity to make catch-up contributions becomes a strategic advantage in your retirement planning arsenal. Once you hit the age of 50, the IRS permits you to contribute an additional amount to your IRA, over and above the standard contribution limits. This is designed to help you bolster your retirement savings if you started late or if your financial landscape allows for a more aggressive savings approach.

Key strategies to maximize your catch-up contributions include:

- Prioritize contributions: Make catch-up contributions a financial priority. Budget effectively to ensure you can fully utilize this opportunity every year.

- Reassess your asset allocation: With additional funds at your disposal, consider diversifying your investments to balance risk and return as you edge closer to retirement.

- Leverage tax advantages: The additional contributions may offer tax benefits, either through tax-deferred growth or immediate tax deductions, depending on your IRA type.

- Regularly review and adjust your retirement goals: Regularly update your financial plan to reflect these enhanced contributions, ensuring your retirement goals are aligned with your current and future needs.

By proactively leveraging these catch-up contributions, you can significantly enhance your financial security in retirement, setting the stage for a more comfortable and fulfilling post-career life.

{kind=link}