As you approach retirement, understanding how to maximize your Social Security benefits becomes a crucial component of securing your financial future. Social Security is not just a government program; it is a lifeline that can significantly enhance your retirement lifestyle when leveraged effectively. In this guide, we will demystify the complexities of Social Security, offering you practical strategies to optimize your benefits. From understanding the impact of your earnings history to strategically timing your claims, we will equip you with the knowledge and tools necessary to make informed decisions. Prepare to take charge of your retirement planning with confidence, ensuring that you receive the maximum benefits you have rightfully earned.

Understanding Social Security Eligibility and Timing

Strategic Claiming: When and How to File for Maximum Benefits

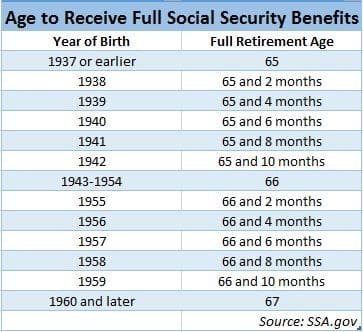

Timing is everything when it comes to unlocking the full potential of your Social Security benefits. Deciding when to file can significantly impact the amount you receive monthly. While you are eligible to start claiming benefits at age 62, waiting until your full retirement age—between 66 and 67, depending on your birth year—can increase your benefits by a substantial margin. For those who are willing to delay even further, up to age 70, the payoff is even greater, thanks to delayed retirement credits. This can boost your monthly benefit by 8% each year you delay past your full retirement age.

- Early Filing: Provides access to funds sooner but results in reduced monthly benefits.

- Full Retirement Age Filing: Offers a balanced approach, ensuring you receive the full benefits you’re entitled to.

- Delayed Filing: Maximizes your benefits, offering a higher monthly payout for the rest of your life.

Consider your financial situation carefully. If you have other income sources or are in good health, delaying your claim can be a smart move. Conversely, if you need the funds immediately or have health concerns, filing earlier might be the better choice. Remember, strategic claiming is not just about timing; it’s about understanding your personal circumstances and making informed decisions to secure a financially stable retirement.

Leveraging Spousal and Survivor Benefits for Financial Advantage

Understanding the intricacies of Social Security benefits can offer significant financial leverage, particularly through spousal and survivor benefits. These options allow you to maximize the benefits you or your spouse are entitled to, creating a more robust retirement plan. Spousal benefits enable you to claim up to 50% of your spouse’s full retirement age benefit, even if you have never worked or have a lower earnings record. This can be especially advantageous if your spouse’s earnings significantly surpass your own. To make the most of this, consider delaying your own benefits to increase your personal payout while utilizing the spousal benefits as a financial bridge.

Survivor benefits provide another layer of security, offering up to 100% of your deceased spouse’s benefits if they were higher than your own. This option is vital for widows and widowers, helping to cushion the financial impact of losing a partner. Key strategies to consider include:

- Delaying your benefits past full retirement age to maximize your monthly payments.

- Coordinating the timing of benefit claims between spouses to optimize total family income.

- Reviewing your family’s earnings records periodically to ensure accuracy and optimal benefit calculations.

By strategically navigating these benefits, you can significantly enhance your financial stability in retirement, ensuring a more secure and comfortable future.

Tax Strategies to Optimize Your Social Security Income

To make the most of your Social Security income, strategic tax planning is crucial. Consider delaying your benefits; by postponing your claim until after your full retirement age, you could increase your monthly benefit by up to 8% annually until age 70. This delay not only boosts your monthly check but can also lead to lower taxes on your benefits in the early years of retirement.

- Manage Your Other Income Sources: Be mindful of how other retirement income, such as pensions or withdrawals from retirement accounts, might push you into a higher tax bracket. Adjusting your income mix can help you stay below the thresholds where Social Security benefits become taxable.

- Leverage Roth Accounts: Withdrawals from Roth IRAs are tax-free and do not count as income for Social Security taxation purposes. This strategy can help you manage your taxable income and reduce the tax impact on your Social Security benefits.

By understanding these tax strategies, you can effectively enhance the longevity and efficiency of your Social Security income, ensuring a more financially secure retirement.

{kind=link}