In today’s fast-paced world, managing finances can often feel like an overwhelming task, especially when debt begins to overshadow your family’s financial well-being. However, taking control of your debt doesn’t have to be a daunting endeavor. By making debt repayment a priority, you can pave the way to a more secure and prosperous future for your family. This article will guide you through practical steps and strategies to effectively tackle debt, empowering you to create a financial plan that aligns with your family’s goals and values. With confidence and determination, you can transform debt repayment from a burden into an achievable and rewarding milestone on your family’s journey to reduce expenses in retirement to extend your savings”>financial freedom.

Assess Your Familys Financial Situation and Set Clear Goals

To make debt repayment a priority, it’s essential to begin by evaluating your family’s current financial landscape. Gather all necessary documents, such as bank statements, credit card bills, and loan agreements, to gain a comprehensive understanding of your financial standing. Analyze your income and expenses to identify any potential areas for improvement. Consider creating a detailed budget that reflects your family’s needs and goals, ensuring that debt repayment is highlighted as a significant component.

Once you have a clear picture of your financial situation, work together to set achievable and specific financial goals. These goals might include:

- Reducing unnecessary expenses to free up more money for debt payments.

- Establishing a debt repayment timeline, with clear milestones to celebrate progress.

- Creating an emergency fund to prevent future debt accumulation.

By setting these goals, you ensure that every family member understands the importance of debt repayment and is committed to achieving financial freedom.

Create a Realistic Budget That Prioritizes Debt Repayment

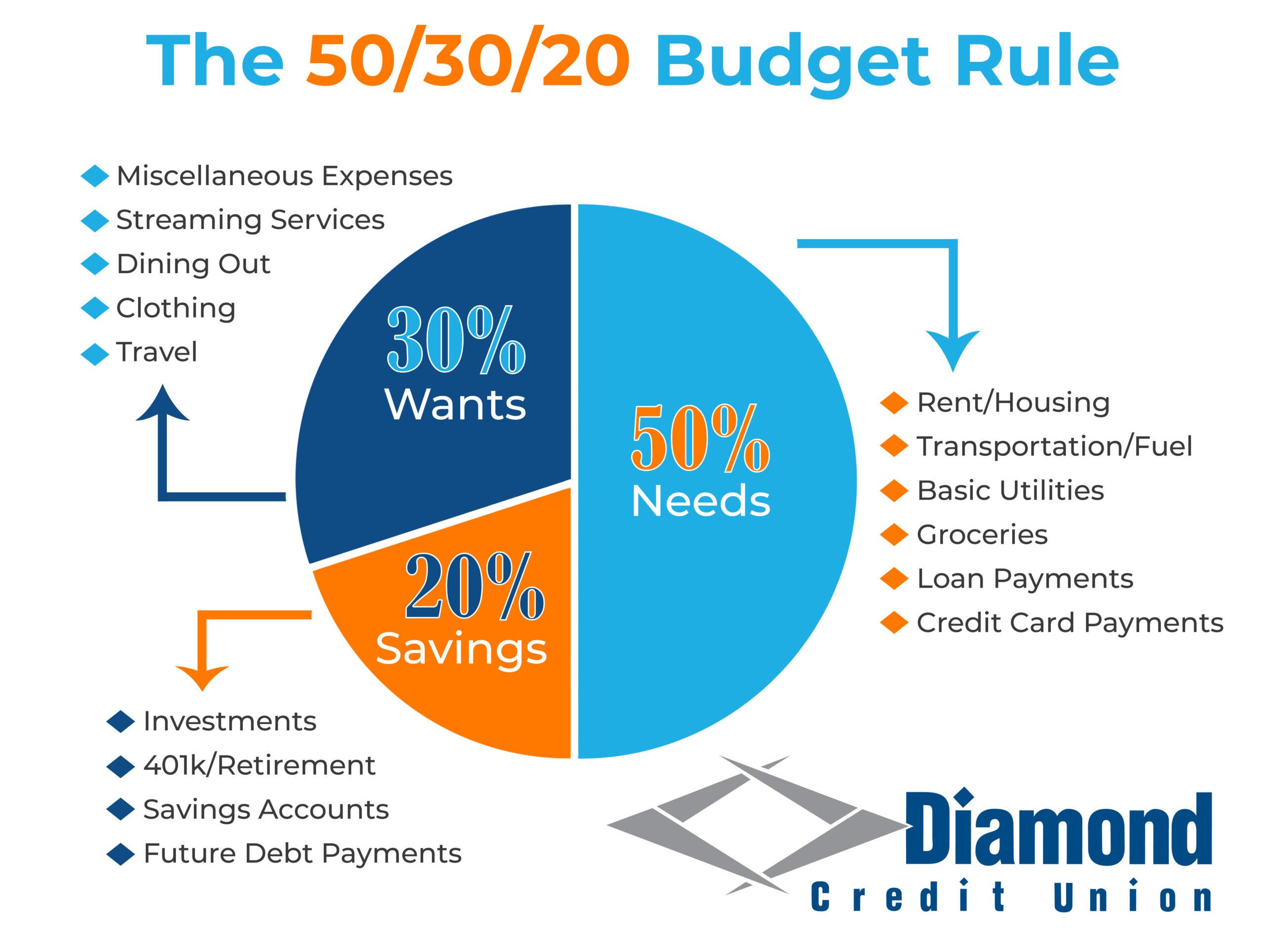

Creating a budget that effectively addresses your family’s debt can seem daunting, but with a strategic approach, it’s entirely achievable. Start by listing all your income sources and essential expenses. This includes rent or mortgage, utilities, groceries, and transportation. Once you’ve identified these, allocate a specific amount towards debt repayment each month. Treat this allocation as a non-negotiable expense, much like your rent or mortgage, to ensure it remains a priority.

To further refine your budget, consider the following strategies:

- Cut Unnecessary Costs: Review your monthly subscriptions and dining habits to find areas where you can reduce spending.

- Set Clear Financial Goals: Establish short-term and long-term objectives for debt repayment to keep you motivated and focused.

- Utilize the Snowball or Avalanche Method: Decide whether to pay off smaller debts first for quick wins (snowball) or target high-interest debts to save on interest (avalanche).

By consistently tracking your spending and adjusting your budget as necessary, you’ll be well on your way to achieving a debt-free future.

Implement Practical Strategies to Reduce Expenses and Increase Income

Reducing expenses and boosting income are key strategies in prioritizing debt repayment for your family. Start by scrutinizing your monthly expenditures to identify areas where you can cut back. Track every dollar and categorize your spending into essentials and non-essentials. You may be surprised to find hidden savings in areas such as dining out, subscription services, or utility bills. Consider implementing a few simple changes:

- Meal planning to reduce grocery costs and minimize food waste.

- Energy-saving habits, like unplugging devices and using energy-efficient bulbs, to lower utility bills.

- Reviewing subscriptions and cancelling those that aren’t used regularly.

To increase income, leverage your skills or hobbies to create additional revenue streams. Freelancing, tutoring, or selling handmade crafts can be lucrative side gigs. Also, consider renting out unused spaces in your home or selling items you no longer need. Each additional dollar earned can be directed towards your debt, accelerating your journey to financial freedom. By implementing these strategies, your family can maintain a balanced budget and make significant strides in debt repayment.

Monitor Progress and Adjust Your Plan to Stay on Track

Regularly evaluating your debt repayment journey is crucial to ensure you remain aligned with your financial goals. Set aside time each month to review your family’s financial statements and assess your progress. Consider the following steps to maintain a clear view of your journey:

- Review Monthly Statements: Examine your credit card and loan statements to track the decrease in your debt balances.

- Analyze Spending Habits: Compare your current spending to your initial budget plan to identify areas where adjustments are needed.

- Adjust Budget if Necessary: If unexpected expenses arise, revise your budget to accommodate these changes without derailing your debt repayment goals.

Don’t hesitate to make necessary adjustments to your strategy. Life circumstances change, and your plan should be flexible enough to adapt. Remember, the objective is to keep moving forward, even if it means making small, incremental changes. Keep your family engaged in the process by discussing progress and setbacks openly, ensuring everyone remains motivated and committed to the goal of becoming debt-free.

{kind=link}