In today’s complex financial landscape, building wealth for your family requires more than just a steady income; it demands strategic foresight and informed decision-making. The journey towards financial prosperity is not merely about accumulating assets but involves a comprehensive approach that integrates saving, investing, and risk management. As families navigate economic uncertainties and evolving market dynamics, making smart financial decisions becomes crucial in securing a stable and prosperous future. This article delves into the essential strategies and principles that can guide families in crafting a robust financial plan, ensuring that wealth is not only built but sustained across generations. By analyzing key financial instruments, tax implications, and investment opportunities, we aim to empower families to make confident choices that align with their long-term goals and values.

Understanding the Foundations of Family Wealth

Creating a robust financial foundation for your family begins with understanding the core principles that govern wealth accumulation and preservation. At the heart of this endeavor lies the strategic allocation of resources, emphasizing not just earning but also saving and investing wisely. Developing a budget that aligns with your family’s goals and values is the first step. This involves a meticulous assessment of income streams and expenditure patterns, ensuring that every dollar is purposefully directed towards both immediate needs and future aspirations. Embrace the power of compound interest by investing early in diverse assets, balancing risk and return to suit your family’s risk tolerance.

- Asset Diversification: Spread investments across different asset classes to mitigate risks.

- Financial Education: Continuously educate yourself and your family on financial literacy to make informed decisions.

- Estate Planning: Implement wills, trusts, and other instruments to secure wealth transfer across generations.

- Insurance: Protect your family’s financial future with adequate insurance coverage against unforeseen events.

These foundational steps not only safeguard against financial instability but also empower future generations with the knowledge and resources needed to sustain and grow family wealth. By instilling these practices, you lay the groundwork for a legacy that transcends monetary value, fostering a culture of financial acumen and security.

Strategic Investment Choices for Long-term Growth

When it comes to ensuring long-term growth, making informed investment decisions is paramount. To cultivate a robust financial portfolio, consider diversifying across various asset classes. This could include a balanced mix of stocks, bonds, real estate, and even alternative investments like commodities or cryptocurrencies. Each of these assets has unique risk and return characteristics, and by diversifying, you can mitigate the impact of volatility on your portfolio.

- Equities: Historically, stocks have provided the highest returns over the long term, making them a cornerstone for growth-focused portfolios.

- Bonds: Offer stability and income, balancing the more volatile nature of stocks.

- Real Estate: Provides tangible asset value and can offer both income through rent and potential appreciation.

- Alternative Investments: Hedge against market downturns and offer exposure to different growth opportunities.

Additionally, regularly reviewing and rebalancing your portfolio is essential. This ensures your investments remain aligned with your financial goals and risk tolerance. Utilize the power of compounding by starting early and consistently investing, allowing your wealth to grow exponentially over time. Strategic investment choices are not just about where to invest but also about maintaining discipline and staying informed about market trends.

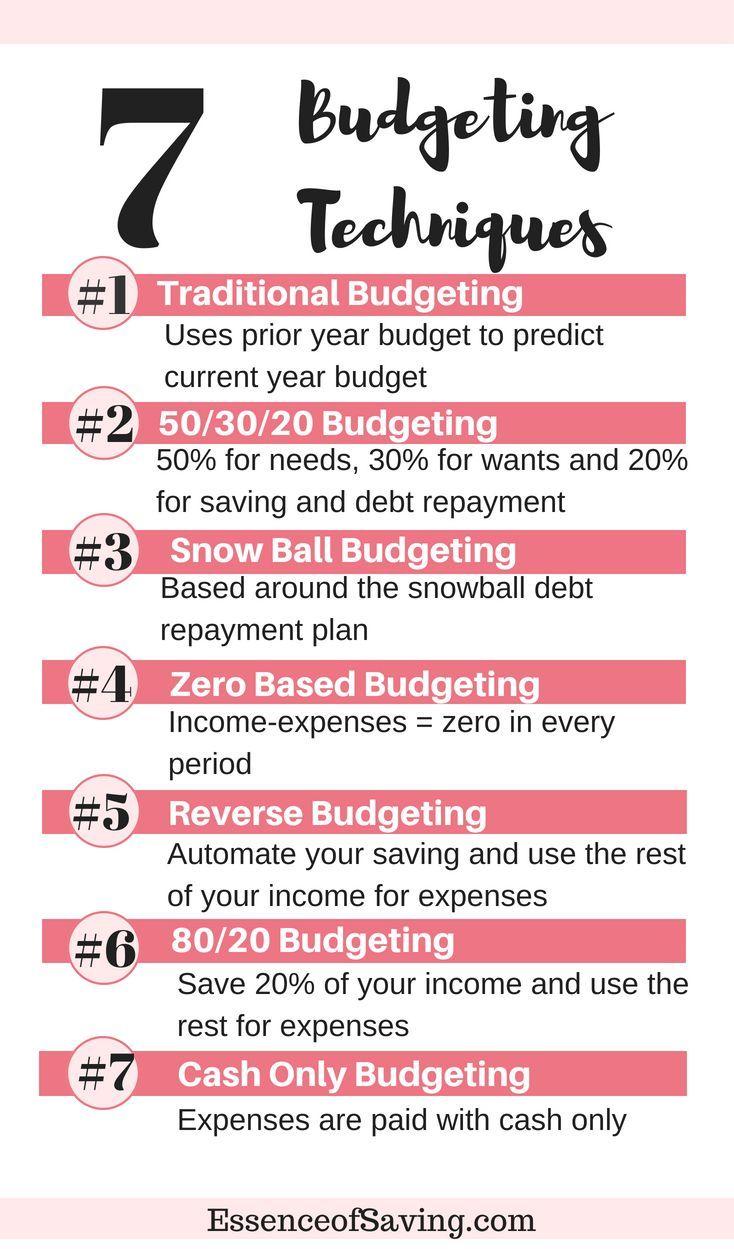

Effective Budgeting Techniques to Maximize Savings

Mastering the art of budgeting is crucial for building wealth and ensuring financial stability for your family. Start by creating a comprehensive plan that aligns with your financial goals. Identify essential expenses and distinguish them from non-essential ones. This will help you allocate your resources more effectively. Utilize budgeting tools and apps to track your spending habits, which can highlight areas where you can cut back.

- Set realistic goals: Define short-term and long-term financial objectives, such as saving for a house or your child’s education.

- Automate savings: Set up automatic transfers to your savings account to ensure consistent growth.

- Review and adjust: Regularly evaluate your budget and make necessary adjustments to accommodate changes in income or expenses.

- Embrace the 50/30/20 rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

By implementing these strategies, you can optimize your financial resources, reduce unnecessary expenditures, and significantly boost your savings. This disciplined approach to budgeting not only helps in accumulating wealth but also provides a safety net for your family’s future.

Leveraging Tax Advantages for Family Financial Health

When it comes to enhancing your family’s financial health, understanding and utilizing tax advantages can be a game-changer. By making informed decisions, you can not only reduce your tax liabilities but also enhance your long-term wealth. Here are some strategies to consider:

- Utilize Tax-Deferred Accounts: Accounts like 401(k)s and IRAs allow you to invest pre-tax income, deferring taxes until you withdraw the funds. This can significantly increase your savings over time due to the power of compound interest.

- Take Advantage of Tax Credits: Credits such as the Child Tax Credit or Earned Income Tax Credit can directly reduce the amount of tax you owe, providing more room in your budget for savings or investments.

- Invest in Education Savings Accounts: Plans like 529 savings accounts offer tax-free growth and withdrawals for educational expenses, easing the future financial burden of tuition fees.

By strategically leveraging these tax benefits, you can effectively build a robust financial foundation, ensuring your family’s prosperity for generations to come. Remember, each family’s situation is unique, so consulting with a tax advisor to tailor these strategies to your specific needs can further amplify their impact.

Contributions")

{kind=link}