Planning for retirement can be a daunting task, especially when you’re navigating the unique challenges and opportunities that come with being self-employed. Unlike traditional employees who may have access to employer-sponsored retirement plans, self-employed individuals must take a proactive approach to ensure their financial security in the golden years. This article will guide you through the best strategies to effectively plan for retirement, tailored specifically for those who run their own businesses or work as freelancers. By leveraging the right tools and making informed decisions, you can build a robust retirement plan that aligns with your personal and professional goals. Whether you’re just starting your self-employment journey or are a seasoned entrepreneur, this comprehensive guide will equip you with the knowledge and confidence to secure a prosperous future.

Understanding Your Unique Retirement Needs as a Self-Employed Professional

As a self-employed professional, your retirement planning is as unique as your career path. Unlike traditional employees, you don’t have the luxury of employer-sponsored retirement plans or matching contributions. However, this doesn’t mean you are at a disadvantage. In fact, the flexibility you have allows you to tailor your retirement strategy to suit your specific needs and goals. To start, consider the following steps:

- Assess Your Current Financial Situation: Begin by understanding your cash flow, savings, and debts. This will help you determine how much you can realistically contribute towards retirement each month.

- Set Clear Retirement Goals: Visualize your retirement lifestyle and estimate the funds required to support it. This could include travel, hobbies, or even starting a new business venture.

- Choose the Right Retirement Accounts: Options like SEP IRAs, Solo 401(k)s, and SIMPLE IRAs offer tax advantages and are tailored for self-employed individuals.

- Diversify Your Investments: Don’t rely solely on one type of investment. Consider a mix of stocks, bonds, and real estate to balance risk and potential returns.

By understanding and addressing your unique retirement needs, you can create a robust plan that not only secures your future but also aligns with your personal and professional aspirations.

Maximizing Tax-Advantaged Retirement Accounts for Self-Employed Individuals

Navigating retirement planning as a self-employed individual can be daunting, but leveraging tax-advantaged accounts can offer significant benefits. Solo 401(k) plans are a powerful option, allowing contributions as both an employer and an employee, which means you can maximize your retirement savings while also reducing your taxable income. The SEP IRA is another excellent choice, providing flexibility in contributions based on your annual income, making it ideal for those with fluctuating earnings. Both options offer tax-deferred growth, ensuring that your investments compound without immediate tax implications.

To further optimize your retirement strategy, consider a Roth IRA for after-tax contributions, especially if you anticipate being in a higher tax bracket during retirement. This way, your withdrawals will be tax-free. Health Savings Accounts (HSAs) can also play a strategic role; not only do they offer tax deductions, but they also grow tax-free and can be used for medical expenses in retirement. By strategically utilizing these accounts, self-employed individuals can create a robust, tax-efficient retirement plan tailored to their unique financial circumstances.

Building a Diversified Investment Portfolio to Secure Your Future

Creating a diverse investment portfolio is crucial for self-employed individuals looking to secure their financial future. As an entrepreneur, you’re not just building a business; you’re also responsible for creating a personal safety net. Diversification is your ally in mitigating risks and maximizing potential returns. Start by exploring a range of investment vehicles that align with your financial goals and risk tolerance. Consider options such as:

- Stocks and Bonds: These are traditional investment choices that offer a balance between risk and reward. Stocks provide growth potential, while bonds offer stability.

- Real Estate: Investing in property can provide steady rental income and potential appreciation. Real estate also acts as a hedge against inflation.

- Mutual Funds and ETFs: These funds allow you to invest in a diversified portfolio managed by professionals, spreading your risk across various sectors and asset classes.

- Retirement Accounts: Utilize tax-advantaged accounts like a SEP IRA or a Solo 401(k) to save for retirement while enjoying tax benefits.

- Alternative Investments: Consider diversifying with options like peer-to-peer lending, REITs, or even cryptocurrency for those willing to take on higher risk.

By thoughtfully allocating your resources across different asset types, you can build a robust investment portfolio that not only secures your retirement but also supports your financial goals throughout your entrepreneurial journey.

Creating a Sustainable Withdrawal Strategy for a Comfortable Retirement

Developing a sustainable withdrawal strategy is essential for self-employed individuals aiming for a secure and enjoyable retirement. Since self-employment often means the absence of a traditional pension plan, it’s crucial to create a personalized strategy that balances both income needs and longevity. Here are some key elements to consider:

- Diversify Your Investment Portfolio: Spread your investments across various asset classes to mitigate risks and enhance growth potential. This includes a mix of stocks, bonds, and perhaps real estate or other alternative investments.

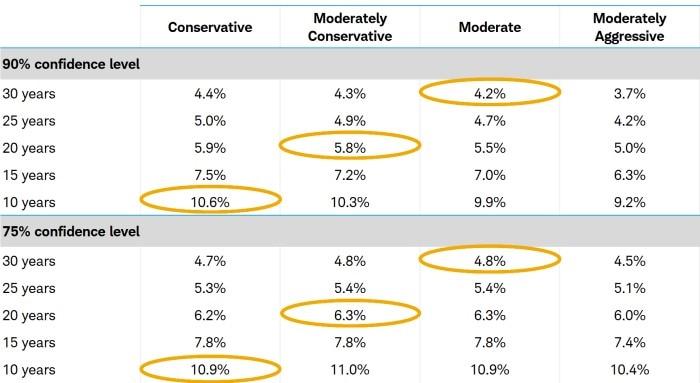

- Calculate Your Safe Withdrawal Rate: Determine a withdrawal rate that supports your lifestyle without depleting your savings too quickly. The commonly suggested rate is around 4%, but it may need adjustment based on your unique circumstances.

- Factor in Inflation: As costs of living rise, ensure your strategy accounts for inflation. This may involve regularly adjusting your withdrawal amounts or investing in assets that historically outpace inflation.

- Plan for Healthcare Costs: Consider setting aside funds specifically for healthcare expenses, which often increase with age. This can help prevent unexpected costs from derailing your retirement plans.

By focusing on these elements, you can craft a withdrawal strategy that provides stability and flexibility, ensuring your retirement years are both financially secure and fulfilling.

{kind=link}