Planning for retirement while saving for a home can feel like juggling two significant financial goals at once, each with its own set of challenges and rewards. However, with the right strategies, it’s entirely possible to balance both pursuits effectively, ensuring a secure financial future and a comfortable place to call home. This guide will walk you through the best ways to approach these dual objectives, offering practical advice and actionable steps to help you build a solid financial foundation. Whether you’re just starting out or looking to optimize your current plan, these insights will empower you to make informed decisions with confidence, turning what might seem like a daunting task into a manageable and rewarding journey.

Understanding Your Financial Priorities for Dual Goals

Balancing the desire to save for both a comfortable retirement and a dream home can feel like walking a financial tightrope. To effectively manage these dual goals, it’s crucial to understand and prioritize your financial objectives. Begin by clearly defining what each goal means to you and establishing a realistic timeline for achieving them. Consider the following steps to gain clarity:

- Evaluate Your Current Financial Situation: Assess your income, expenses, and existing savings. Knowing where you stand financially will help you allocate resources more effectively.

- Set Specific Goals: Determine the amount you need for a down payment on your home and how much you want to have saved for retirement. Make sure these goals are specific, measurable, and time-bound.

- Prioritize Based on Urgency and Importance: If you’re nearing retirement age, you might prioritize retirement savings. Conversely, if you’re younger and eager to own a home, focus on building your home fund.

- Explore Flexible Saving Strategies: Look into retirement accounts like a 401(k) or IRA that offer tax advantages, and consider saving for a home in a high-yield savings account.

By clearly identifying your priorities and aligning your savings strategies accordingly, you can make informed decisions that support both your short-term and long-term financial aspirations.

Creating a Balanced Budget to Accommodate Both Retirement and Home Savings

Crafting a budget that effectively addresses both retirement and home savings requires strategic planning and disciplined execution. Begin by assessing your current financial situation, including income, expenses, and existing savings. Identify non-essential expenditures that can be trimmed to boost savings. It’s crucial to establish clear savings goals for both retirement and a home, taking into account factors such as desired retirement age, lifestyle, and housing market conditions.

Next, allocate funds wisely by implementing a 50/30/20 budgeting rule. Allocate 50% of your income towards necessities like housing, utilities, and groceries. Dedicate 30% to discretionary spending, ensuring you enjoy life while maintaining financial discipline. Lastly, reserve 20% for savings and debt repayment, with a balanced split between retirement accounts and a dedicated home savings fund. Consider the following tips to optimize your savings strategy:

- Maximize employer-sponsored retirement contributions to benefit from potential matching funds.

- Set up automatic transfers to your savings accounts to enforce consistent saving habits.

- Regularly review and adjust your budget to accommodate changes in income or financial priorities.

- Explore investment opportunities that align with your risk tolerance to grow your savings more effectively.

By adhering to these strategies, you can confidently progress towards achieving both retirement security and homeownership dreams.

Leveraging Investment Options to Maximize Long-term Growth

When it comes to balancing the dual goals of preparing for retirement and saving for a home, it’s essential to explore a variety of investment options that can drive long-term growth. Diversification is key. Consider allocating your assets across a mix of traditional and alternative investments. Stocks and mutual funds are classic choices that offer the potential for substantial growth, though they come with a higher level of risk. On the other hand, bonds provide more stability and can serve as a buffer against market volatility.

- Real Estate Investments: This option not only helps you save for your home but also provides a steady income stream through rental properties.

- Retirement Accounts: Maximize contributions to tax-advantaged accounts like 401(k)s or IRAs, ensuring you benefit from employer matches and tax breaks.

- Robo-Advisors: For those who prefer a hands-off approach, robo-advisors can automatically balance your portfolio in alignment with your risk tolerance and financial goals.

It’s crucial to regularly review your investment portfolio to ensure it aligns with your evolving goals and market conditions. Leveraging a combination of these investment strategies can pave the way for a financially secure retirement while simultaneously building the equity needed to purchase your dream home.

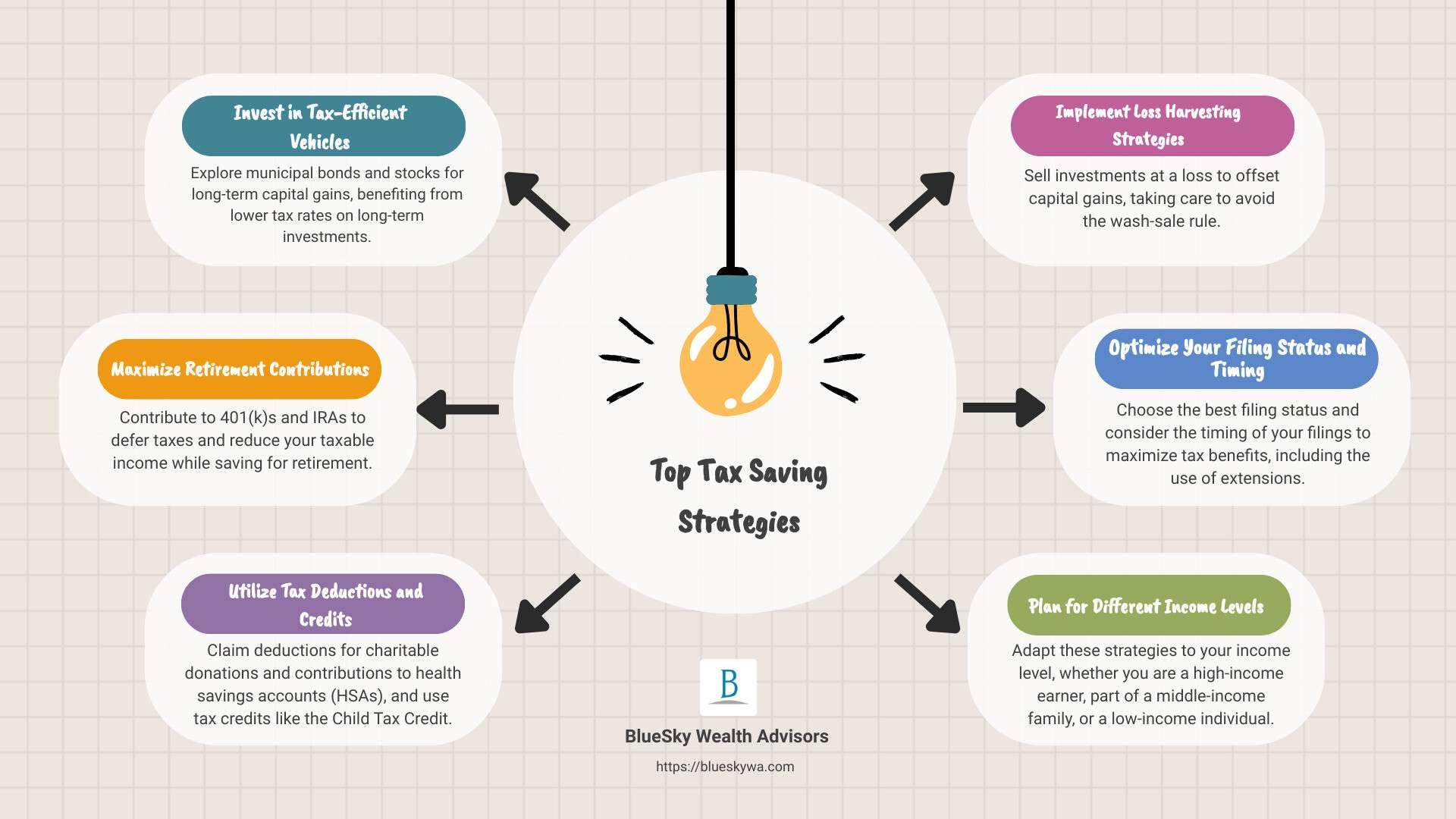

Utilizing Tax-efficient Strategies for Optimized Savings

Maximizing your savings while balancing the dual goals of retirement planning and home ownership requires smart, tax-efficient strategies. One key approach is to leverage tax-advantaged accounts. Consider contributing to a Roth IRA or a traditional IRA for retirement, both of which offer tax benefits that can help your savings grow more efficiently. A Roth IRA allows for tax-free withdrawals in retirement, while contributions to a traditional IRA may be tax-deductible, depending on your income.

- 401(k) Contributions: Maximize your employer-sponsored 401(k) contributions, especially if your employer offers a matching program. This not only reduces your taxable income but also boosts your retirement savings with “free money” from your employer.

- Health Savings Accounts (HSAs): If you’re eligible, an HSA can be a powerful tool for tax-free growth, providing funds for medical expenses now and in retirement.

- First-Time Homebuyer Programs: Look into tax incentives and savings programs designed for first-time homebuyers, such as tax credits or special savings accounts, which can ease the tax burden and accelerate your home savings.

By strategically utilizing these tax-efficient options, you can effectively grow your wealth while preparing for both retirement and homeownership, securing a financially stable future.

{kind=link}