Planning for a secure retirement is a critical endeavor, especially for those who are self-employed and accustomed to steering their own financial ship. Unlike traditional employees who may rely on employer-sponsored retirement plans, self-employed individuals bear the full responsibility of designing their own financial futures. This can seem daunting, but with the right strategies and a proactive mindset, securing a comfortable retirement is entirely achievable. In this article, we will guide you through the essential steps and considerations necessary for crafting a robust retirement plan tailored to the unique challenges and opportunities faced by self-employed professionals. Whether you’re just starting your entrepreneurial journey or are a seasoned veteran, these insights will empower you to take control of your financial destiny with confidence and clarity.

Understanding Retirement Needs and Setting Clear Goals

For self-employed individuals, retirement planning requires a proactive approach and a keen understanding of your future financial needs. Identifying your retirement goals is crucial in crafting a robust plan that ensures a comfortable lifestyle after you’ve hung up your work boots. Begin by asking yourself the right questions: What age do you wish to retire? What kind of lifestyle do you envision? How much will healthcare and other living expenses cost? Your answers will serve as a foundation for calculating how much you need to save.

Once you have a clear picture of your needs, it’s time to set specific, measurable goals. Here are some steps to guide you:

- Calculate your retirement income: Consider all potential sources such as savings, investments, and social security benefits.

- Estimate your expenses: Account for basic living costs, leisure activities, and unexpected healthcare expenses.

- Set a savings target: Determine how much you need to save monthly or annually to reach your retirement goal.

- Review and adjust: Regularly assess your progress and make necessary adjustments to stay on track.

By setting clear and actionable goals, you’ll have a structured roadmap that leads to a secure and fulfilling retirement.

Choosing the Right Retirement Accounts for Self-Employed Individuals

For self-employed individuals, selecting the right retirement accounts can significantly impact your financial future. It’s essential to understand the unique options available to you and how they align with your retirement goals. Here are some of the most effective retirement savings vehicles tailored for the self-employed:

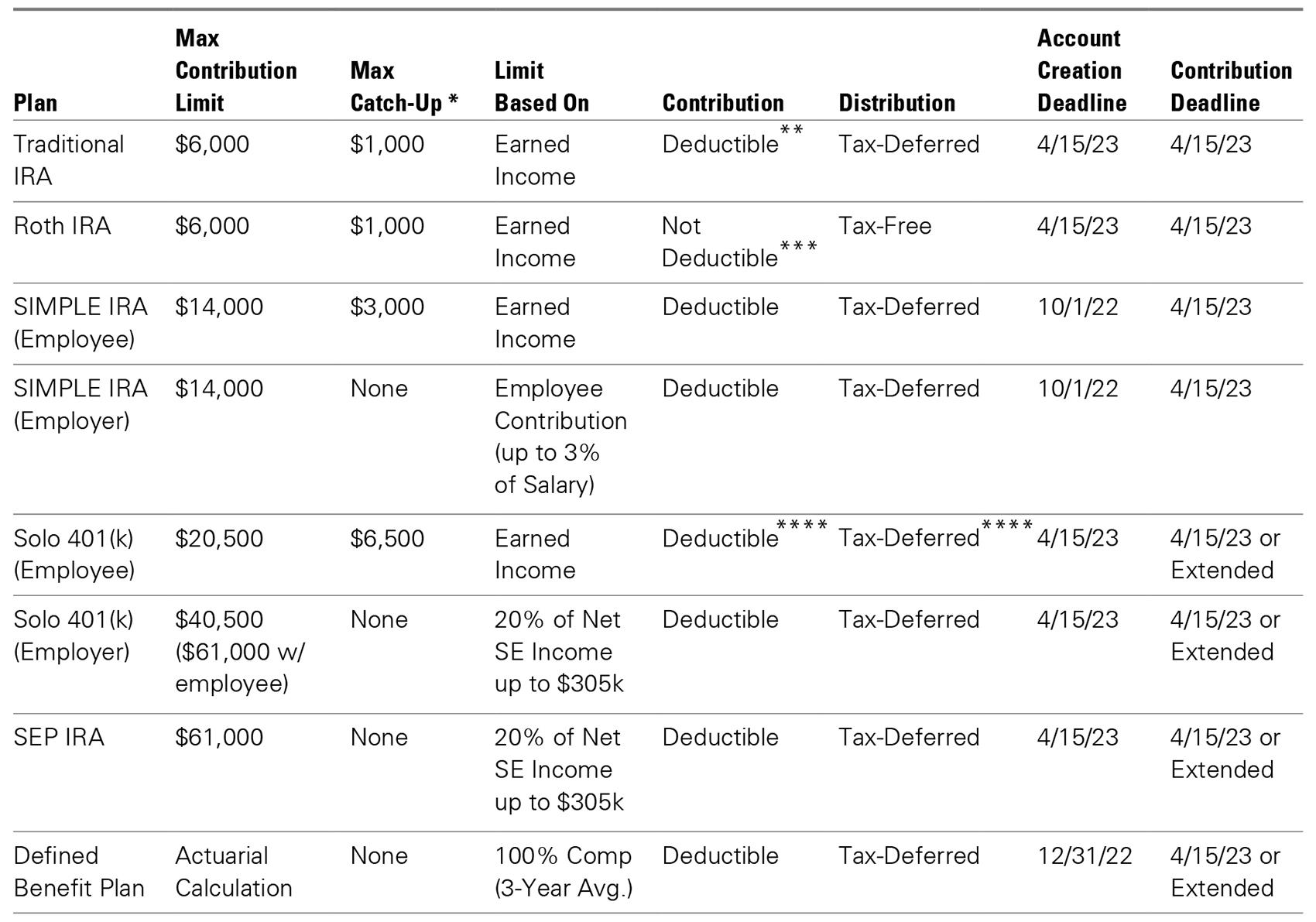

- SEP IRA: The Simplified Employee Pension (SEP) IRA allows you to contribute up to 25% of your net earnings, making it a powerful tool for maximizing your retirement savings. It’s simple to set up and has low administrative costs, offering flexibility for fluctuating income levels.

- Solo 401(k): Ideal for sole proprietors, this account provides the opportunity to make both employer and employee contributions, allowing for higher total contributions compared to other options. Additionally, the Roth Solo 401(k) variant offers tax-free withdrawals, which can be beneficial depending on your tax strategy.

- SIMPLE IRA: Although less flexible than a SEP IRA, the Savings Incentive Match Plan for Employees (SIMPLE) IRA is easier to maintain and still provides tax-deferred growth. It’s a suitable choice if you have a small team or plan to expand your business.

Each option comes with its own set of rules and benefits, so it’s crucial to evaluate them based on your business structure, income level, and long-term retirement objectives. Consulting with a financial advisor can also provide personalized insights to ensure you’re making the best choice for your situation.

Maximizing Contributions and Tax Benefits

As a self-employed individual, it’s crucial to be strategic about your retirement savings to both enhance your future security and enjoy immediate tax advantages. Consider these key actions to maximize your contributions and reap tax benefits:

- Open a SEP IRA or Solo 401(k): These accounts offer high contribution limits, allowing you to set aside a substantial portion of your income while reducing your taxable income.

- Take Advantage of Catch-Up Contributions: If you’re over 50, you can make additional contributions to your retirement accounts, providing an opportunity to bolster your savings as you near retirement.

- Leverage Tax Deductions: Contributions to traditional retirement accounts are often tax-deductible, lowering your taxable income and potentially placing you in a lower tax bracket.

- Consider a Roth IRA for Tax-Free Growth: While contributions aren’t tax-deductible, the tax-free withdrawals during retirement can be a significant benefit, especially if you anticipate being in a higher tax bracket later.

Implementing these strategies not only secures your financial future but also provides immediate tax relief, allowing you to invest more effectively in your retirement.

Diversifying Investments to Secure Your Financial Future

When you’re self-employed, taking charge of your financial future is essential, and diversifying your investments plays a crucial role in this process. A well-diversified portfolio helps mitigate risks and capitalizes on various growth opportunities. Consider incorporating a mix of stocks, bonds, and real estate into your investment strategy. Stocks offer the potential for high returns, while bonds provide stability and regular income. Real estate investments, whether through direct property ownership or Real Estate Investment Trusts (REITs), can offer both capital appreciation and rental income.

Additionally, explore alternative investments such as peer-to-peer lending, cryptocurrencies, and commodities. These options can provide a hedge against market volatility and inflation. Ensure you stay informed about market trends and adjust your portfolio as needed to maintain a balanced and diverse asset allocation. Diversification not only safeguards your financial future but also enhances your chances of achieving a secure retirement.

{kind=link}