In an increasingly complex financial landscape, the pursuit of family wealth growth requires a strategic balance between risk and reward. A balanced investment approach, integrating both traditional and modern financial instruments, offers a robust pathway to achieving long-term financial goals. This article delves into the best methodologies for cultivating family wealth, emphasizing the importance of diversification, risk management, and informed decision-making. By analyzing current market trends and historical data, we will explore how families can effectively allocate resources across various asset classes, from equities and bonds to real estate and emerging investment opportunities. Armed with a confident understanding of these principles, families can navigate the financial markets with greater assurance, securing their financial future while laying a solid foundation for generations to come.

Understanding Risk and Reward in Diverse Investment Portfolios

In the intricate world of investments, the balance between risk and reward is crucial for growing family wealth effectively. A well-diversified portfolio can serve as a robust strategy, minimizing potential losses while maximizing returns. This approach involves allocating assets across various categories such as stocks, bonds, real estate, and even alternative investments like commodities or cryptocurrencies. Diversification reduces exposure to any single asset class, thereby cushioning the portfolio against market volatility.

- Stocks: Offer high growth potential but come with higher risk.

- Bonds: Generally more stable, providing a steady income stream.

- Real Estate: Tangible assets that can appreciate over time and generate rental income.

- Alternative Investments: Hedge against inflation and market downturns.

By understanding the risk profile of each asset type, families can tailor their investment strategies to align with their financial goals and risk tolerance. It’s not just about spreading investments across different sectors; it’s about strategically choosing assets that complement each other. This balanced approach ensures that the portfolio is resilient and capable of achieving long-term financial objectives.

Strategic Asset Allocation for Long-term Family Wealth

In the pursuit of long-term family wealth, a disciplined approach to strategic asset allocation can serve as a cornerstone for financial growth. By diversifying investments across a variety of asset classes, families can effectively manage risk while optimizing potential returns. Key considerations include:

- Equity Investments: Allocating a portion of the portfolio to stocks offers the potential for high returns over time, benefiting from market growth and dividends.

- Fixed Income: Bonds and other fixed-income securities provide stability and regular income, acting as a buffer against market volatility.

- Real Estate: Including real estate can hedge against inflation and provide both rental income and capital appreciation.

- Alternative Investments: Exposure to commodities, private equity, or hedge funds can enhance diversification and yield uncorrelated returns.

Adopting a balanced approach not only aligns with varying risk appetites within the family but also ensures that the portfolio remains resilient through economic cycles. Regular reviews and adjustments, aligned with changing financial goals and market conditions, are essential to sustaining growth and safeguarding wealth for future generations.

Leveraging Tax-efficient Investment Strategies

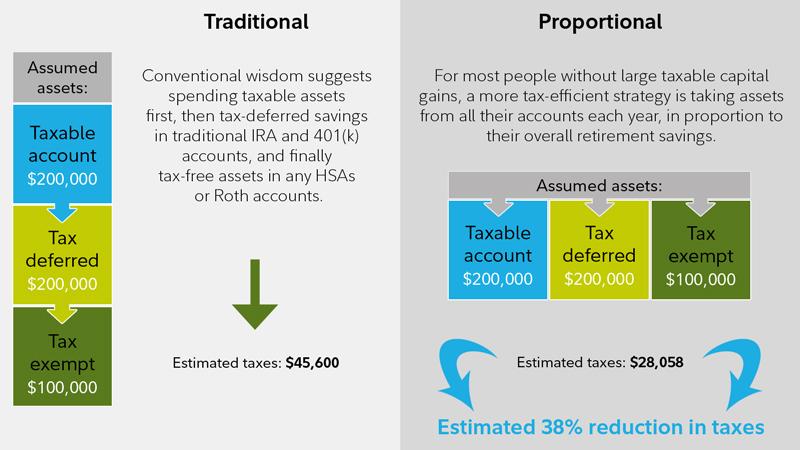

Understanding how to minimize tax liabilities is crucial for maximizing the growth of family wealth. Tax-efficient investment strategies allow investors to keep more of their returns by reducing the tax impact on their portfolios. One effective approach is to utilize tax-advantaged accounts, such as IRAs and 401(k)s, which offer tax deferral or tax-free growth. These accounts can significantly enhance the compounding effect over time, providing a substantial boost to long-term wealth accumulation.

Investors should also consider the strategic placement of assets within different account types. For example, placing high-growth assets in tax-advantaged accounts can shield them from immediate taxation, while allocating income-generating investments to taxable accounts might allow for the utilization of lower tax rates on dividends and long-term capital gains. Additionally, employing tax-loss harvesting can be an effective way to offset gains with losses, thereby reducing taxable income. Key strategies include:

- Maximizing contributions to tax-advantaged retirement accounts.

- Strategically placing high-yield investments in tax-advantaged accounts.

- Utilizing tax-loss harvesting to offset capital gains.

- Investing in tax-efficient mutual funds and ETFs.

By integrating these strategies into a balanced investment approach, families can efficiently grow their wealth while keeping tax implications in check, ultimately achieving a more robust financial future.

Building a Resilient Financial Future through Smart Diversification

In today’s dynamic economic landscape, achieving financial resilience for your family requires a strategic and diversified approach. By allocating assets across various investment vehicles, families can mitigate risks and seize growth opportunities. Consider a mix of the following:

- Stocks and Bonds: Equities offer growth potential, while bonds provide stability. A balanced portfolio can harness the benefits of both, adjusting the ratio based on your risk tolerance.

- Real Estate: Investing in property not only provides potential rental income but also serves as a hedge against inflation, diversifying your portfolio beyond traditional securities.

- Mutual Funds and ETFs: These pooled investment vehicles offer diversified exposure to various asset classes, making them ideal for investors seeking professional management without the complexities of individual stock selection.

- Alternative Investments: Consider adding assets like commodities, hedge funds, or private equity to your portfolio. These can offer unique growth opportunities and further diversification.

By thoughtfully integrating these elements, families can craft a robust investment strategy that adapts to market fluctuations and aligns with long-term financial goals. A well-diversified portfolio not only protects against volatility but also positions your family for sustained wealth accumulation.

{kind=link}