In the ever-evolving landscape of personal finance, ensuring a secure and prosperous retirement is a goal shared by many. One of the most effective tools at your disposal is the Individual Retirement Account (IRA), a powerful vehicle designed to help you save for the future. However, simply contributing to an IRA is not enough; maximizing these contributions is crucial for long-term growth and financial stability. In this guide, we will walk you through strategic approaches to optimize your IRA contributions, empowering you to make informed decisions that will enhance your retirement savings. With confidence and clarity, we’ll explore key strategies, from understanding contribution limits and tax advantages to selecting the right investment mix, all tailored to help you harness the full potential of your IRA for a secure and flourishing retirement.

Understanding Contribution Limits and Catch-Up Opportunities

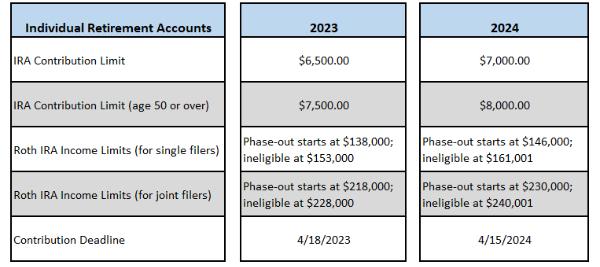

One of the most effective strategies to boost your retirement savings is to fully understand and utilize the contribution limits set by the IRS. For 2023, the standard contribution limit for an IRA is $6,500. However, if you are aged 50 or older, you are eligible for catch-up contributions, allowing you to contribute an additional $1,000, bringing your total possible contribution to $7,500. This additional space is designed to help those nearing retirement to accelerate their savings and take advantage of tax-deferred growth.

To make the most of these opportunities, consider these strategies:

- Automate Your Contributions: Set up automatic transfers from your bank account to your IRA to ensure you are consistently maximizing your contributions throughout the year.

- Review Your Budget: Regularly assess your financial situation to identify areas where you can cut back and reallocate funds to your IRA.

- Maximize Early: Try to reach your contribution limit as early in the year as possible to benefit from compound growth over a longer period.

- Stay Informed: Keep up with annual changes to contribution limits and catch-up provisions, as they can vary and impact your strategy.

Choosing the Right Investment Mix for Your IRA

Creating a well-balanced investment portfolio for your IRA is crucial to achieving long-term growth and stability. The ideal mix often depends on your age, risk tolerance, and retirement goals. Here are some key considerations to help you tailor your investment strategy:

- Diversification: Spread your investments across various asset classes, such as stocks, bonds, and real estate. Diversifying reduces risk and can enhance returns over time.

- Risk Assessment: Evaluate your comfort with risk. Younger investors may opt for more aggressive growth stocks, while those closer to retirement might prefer conservative options like bonds.

- Rebalancing: Regularly review and adjust your portfolio to maintain your desired asset allocation. This practice ensures you capitalize on growth opportunities and mitigate losses.

- Tax Efficiency: Consider the tax implications of your investment choices. Opt for tax-efficient funds and strategies to maximize your after-tax returns.

By focusing on these elements, you can craft a resilient IRA investment strategy that supports your financial aspirations and adapts to market changes.

Leveraging Tax Advantages for Maximum Growth

Taking full advantage of the tax benefits offered by IRAs can significantly boost your retirement savings. By understanding and utilizing these advantages, you can enhance your portfolio’s growth potential. Here’s how:

- Traditional IRA Tax Deductibility: Contributions to a Traditional IRA may be tax-deductible, lowering your taxable income for the year. This can provide you with more capital to invest, accelerating your growth potential.

- Roth IRA Tax-Free Withdrawals: Although contributions are made with after-tax dollars, withdrawals from a Roth IRA in retirement are tax-free. This allows your investments to grow without the burden of taxes, maximizing your net returns.

- Tax-Deferred Growth: Both Traditional and Roth IRAs offer the benefit of tax-deferred growth. This means you won’t pay taxes on any investment gains, dividends, or interest as long as the funds remain in the account, allowing your investments to compound more effectively.

By strategically choosing between a Traditional or Roth IRA, or even utilizing both, you can align your investment strategy with your tax situation, ensuring that you are positioned for maximum growth over the long term.

Strategies for Consistent and Increased Contributions

To ensure you’re maximizing your IRA contributions consistently, consider implementing some key strategies that can simplify the process and potentially enhance your financial growth over time. Start by automating your contributions; setting up automatic transfers from your bank account to your IRA can help ensure that you never miss a contribution deadline. This method also allows you to benefit from dollar-cost averaging, where regular investments help mitigate market volatility by buying more shares when prices are low and fewer when prices are high.

Another effective strategy is to review and adjust your budget regularly. This involves examining your current expenses and identifying areas where you can cut back, thereby freeing up additional funds for your IRA. Additionally, consider the following approaches to bolster your contributions:

- Take advantage of windfalls: Allocate a portion of any unexpected bonuses, tax refunds, or inheritances directly to your IRA.

- Increase contributions gradually: Each year, aim to increase your contributions by a small percentage. This gradual increase can have a significant impact over the long term without drastically affecting your monthly budget.

- Utilize catch-up contributions: If you’re over 50, make sure to take advantage of catch-up contributions to boost your retirement savings.

By adopting these strategies, you’ll be better positioned to make the most of your IRA and set yourself up for a more secure financial future.

{kind=link}