Achieving financial independence is a transformative goal for families seeking to secure a stable and prosperous future. In an era where financial pressures are ever-present, understanding how to effectively set and attain financial independence is more crucial than ever. This guide is designed to provide families with the practical strategies and insights needed to navigate the complexities of financial planning. With a confident approach, we will explore actionable steps to define financial goals, manage expenses, and build sustainable wealth. Whether you’re just starting your journey or looking to refine your existing strategies, this article will empower you to take control of your financial destiny and create a legacy of security and freedom for your loved ones.

Establishing a Clear Financial Vision for Your Family

Setting a financial vision for your family begins with understanding your collective goals and aspirations. Start by holding a family meeting to discuss what financial independence means to each member. Encourage open dialogue to ensure everyone feels heard and valued. Once you have a comprehensive understanding, translate these goals into a clear vision statement. This will serve as your family’s guiding star, aligning every financial decision you make with your long-term objectives.

Next, break down this vision into actionable steps. Consider creating a family financial plan that includes:

- A monthly budget to track income and expenses.

- Emergency savings goals to provide a safety net for unforeseen circumstances.

- Investment strategies to grow your wealth over time.

- Debt reduction plans to alleviate financial burdens.

By establishing a clear path and regularly reviewing your progress, your family can steadily move towards financial independence with confidence and unity.

Crafting a Practical Budget and Savings Plan

To embark on the journey toward financial independence, families must create a budget and savings plan that is both realistic and adaptable. Start by analyzing your current financial situation: list all sources of income and track every expense. This transparency will reveal spending habits and highlight areas for improvement. Once you have a clear picture, categorize your expenses into necessities, savings, and discretionary spending. Allocating funds wisely is key; aim to prioritize essential expenses while setting aside a fixed percentage for savings.

- Necessities: Ensure that your basic needs such as housing, utilities, groceries, and healthcare are covered first.

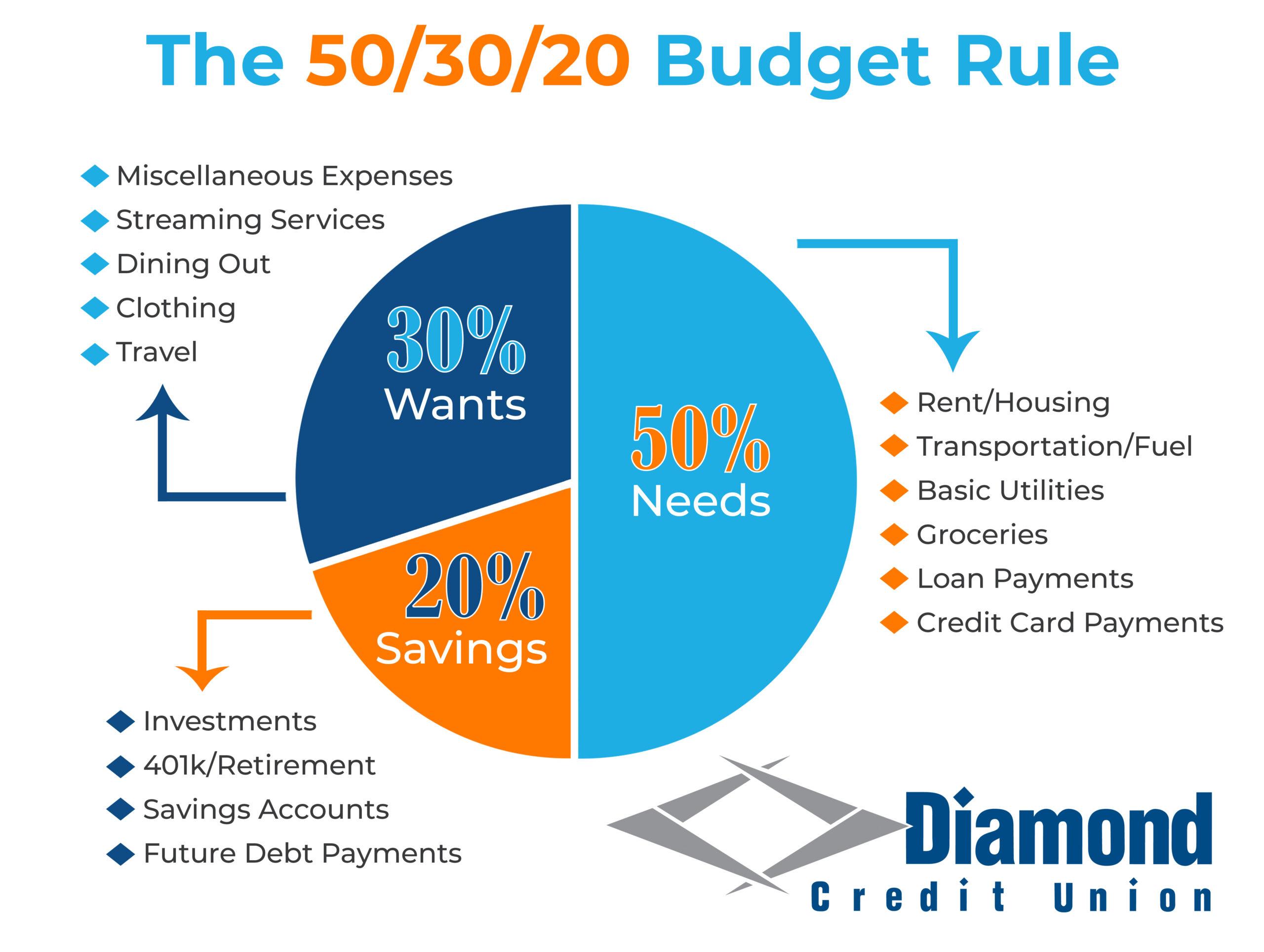

- Savings: Implement the 50/30/20 rule—where 20% of your income is dedicated to savings and debt repayment.

- Discretionary Spending: Limit these expenses and opt for cost-effective alternatives to maximize your savings.

To enhance your savings strategy, consider setting specific goals. Whether it’s an emergency fund, a family vacation, or retirement savings, having clear objectives will motivate you to stick to your plan. Use tools like budgeting apps or spreadsheets to track your progress and make adjustments as needed. By crafting a practical and tailored financial plan, families can steadily move towards achieving their long-term goals.

Investing Wisely to Build Long-Term Wealth

Embarking on the journey to financial independence requires a well-crafted strategy that considers both immediate needs and future goals. For families, this means creating a comprehensive plan that balances current expenses with long-term savings. Begin by setting clear financial goals, such as paying off debt, saving for a child’s education, or building a retirement fund. Prioritize these objectives and allocate resources accordingly, ensuring each goal is accompanied by a realistic timeline and actionable steps.

One effective approach is to diversify your investments, thus spreading risk and increasing potential returns. Consider a mix of asset classes such as stocks, bonds, and real estate. Explore options like index funds or exchange-traded funds (ETFs) for stock market exposure, which offer low fees and broad diversification. Additionally, investing in real estate can provide both rental income and long-term appreciation. Utilize tax-advantaged accounts like 401(k)s or IRAs to maximize your savings potential, and make sure to review and adjust your investment portfolio periodically to align with changing financial goals and market conditions.

Leveraging Tax Strategies to Maximize Family Income

One of the most effective ways to bolster family income is by implementing strategic tax planning. Understanding and utilizing available tax credits and deductions can significantly reduce the annual tax burden. Consider the following strategies to make the most of your tax situation:

- Take advantage of tax-advantaged accounts: Contribute to retirement accounts like IRAs or 401(k)s, which can offer immediate tax deductions and long-term tax benefits.

- Utilize family tax credits: Ensure you’re claiming all eligible credits such as the Child Tax Credit, Earned Income Tax Credit, and education credits, which can provide substantial savings.

- Leverage tax-loss harvesting: Offset capital gains by selling investments at a loss, effectively reducing taxable income.

- Optimize filing status: Choose the most beneficial filing status for your family situation, such as “Married Filing Jointly,” which often results in lower tax rates.

By incorporating these strategies into your financial plan, you can effectively increase your family’s disposable income, paving the way toward achieving financial independence.

{kind=link}