In an era marked by economic volatility and rapid financial changes, creating a robust investment plan tailored to your family’s unique needs has never been more crucial. Navigating the complex world of investments can be daunting, but with a strategic approach grounded in sound financial principles, you can secure a prosperous future for your loved ones. This article delves into the analytical framework necessary for crafting an investment plan that aligns with your family’s goals, risk tolerance, and financial circumstances. By examining key components such as asset allocation, risk management, and long-term planning, we aim to empower you with the confidence to make informed decisions. Join us as we explore actionable strategies and insights that will help you build a resilient financial foundation, ensuring your family’s security and peace of mind in an unpredictable world.

Understanding Your Familys Financial Goals and Priorities

To tailor an investment plan that aligns with your family’s unique financial landscape, it’s essential to delve deep into understanding what truly matters to each family member. Begin by identifying core financial goals—these could range from saving for your children’s education to planning for a comfortable retirement. Equally important is recognizing the short-term priorities that might include saving for a vacation or purchasing a new home. Engage in open conversations to uncover each family member’s aspirations and fears about money. This collaborative approach ensures that the investment strategy reflects a shared vision, fostering commitment and unity in financial decision-making.

- Identify Core Goals: Understand long-term and short-term objectives.

- Evaluate Risk Tolerance: Different family members might have varying levels of comfort with risk.

- Set Realistic Milestones: Establish achievable steps to monitor progress.

- Regular Reviews: Conduct periodic check-ins to reassess priorities and make necessary adjustments.

By clearly outlining these priorities and understanding the risk tolerance of each family member, you lay the groundwork for an investment plan that not only meets financial goals but also strengthens family bonds. This analytical process transforms abstract desires into actionable steps, ensuring a future where your family’s financial aspirations are not just dreams, but realities.

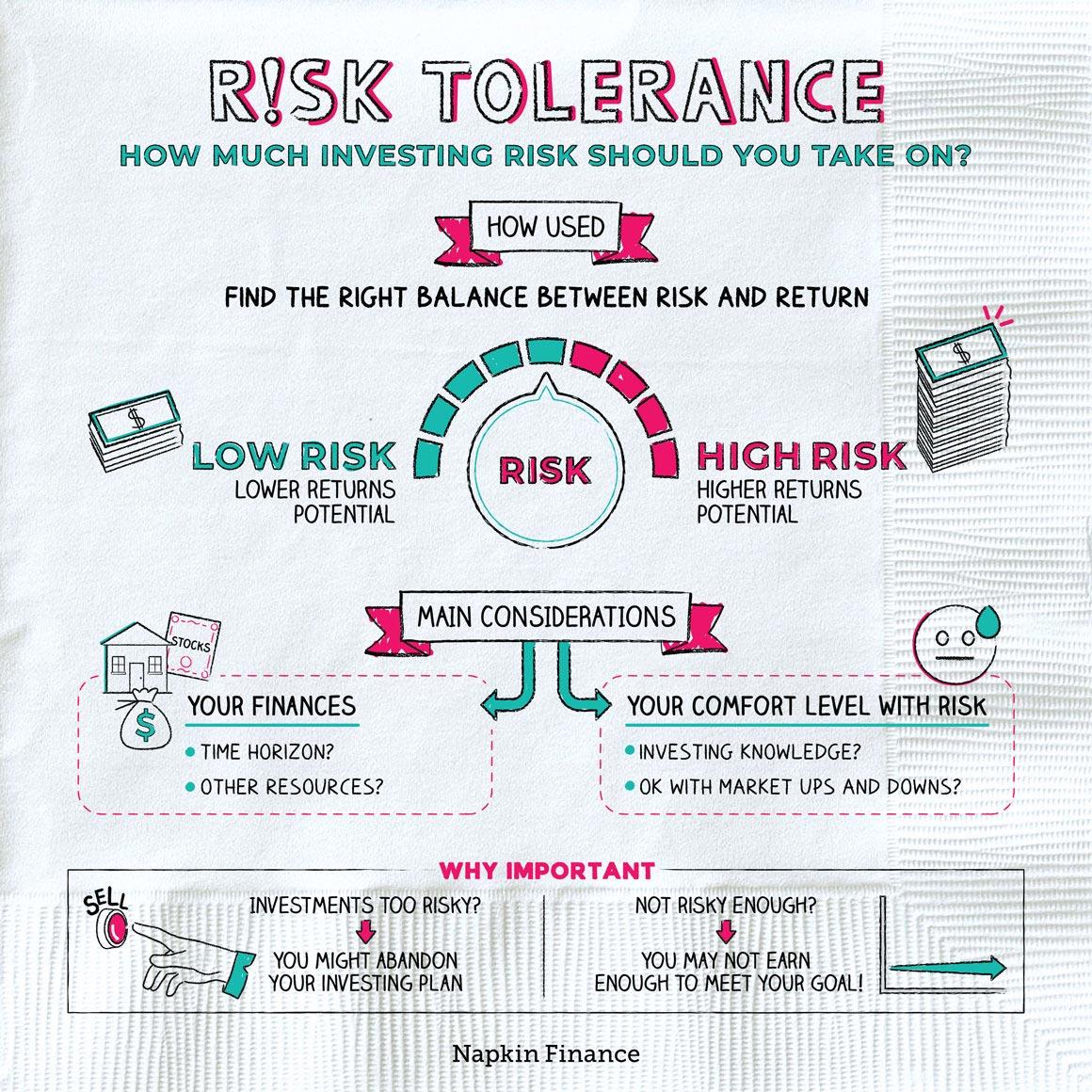

Evaluating Risk Tolerance and Time Horizon for Effective Planning

Understanding your family’s risk tolerance is a crucial step in crafting an investment plan that aligns with your financial goals. Risk tolerance refers to the level of variability in investment returns that you are willing to withstand. To evaluate this, consider factors such as:

- Your family’s current financial situation and future income prospects

- Previous investment experiences and reactions to market fluctuations

- Psychological comfort with potential losses

Equally important is determining your time horizon, which is the period you expect to hold an investment before taking the money out. A longer time horizon allows for a greater tolerance for risk, as there is more time to recover from potential losses. Consider these aspects:

- Short-term goals like buying a home or funding education, which may require more conservative investments

- Long-term objectives such as retirement, where higher-risk, higher-return investments could be suitable

- Life changes that might affect your timeline, such as career shifts or family expansions

Balancing risk tolerance with your time horizon is essential for effective financial planning, ensuring your family’s investment plan is both sustainable and aligned with your aspirations.

Diversifying Investments to Balance Growth and Security

Creating a robust investment plan involves striking a delicate balance between growth and security, ensuring that your family’s financial future is both prosperous and protected. A diversified investment portfolio is key to achieving this balance, as it mitigates risk while maximizing potential returns. Diversification involves spreading investments across various asset classes, sectors, and geographical regions. Consider including a mix of:

- Equities: Stocks offer potential for high returns but come with increased volatility. Allocate a portion to growth stocks for long-term appreciation and dividend-paying stocks for income.

- Bonds: These provide stability and regular income, acting as a counterbalance to more volatile assets. Choose a combination of government and corporate bonds to enhance security.

- Real Estate: Investing in property can offer both income and capital appreciation, adding a tangible asset to your portfolio.

- Alternative Investments: Consider options like commodities, hedge funds, or private equity to further diversify and hedge against market fluctuations.

Regularly reassess your family’s financial goals and risk tolerance, adjusting the asset allocation accordingly. Employ a disciplined approach by setting clear investment objectives, and use tools like dollar-cost averaging to mitigate timing risks. By doing so, you can create a well-rounded investment plan that aligns with your family’s unique needs and aspirations, paving the way for both immediate security and long-term growth.

Implementing and Monitoring Your Familys Investment Strategy

To ensure your family’s investment plan remains effective, consistent implementation and vigilant monitoring are crucial. Begin by establishing a clear schedule for reviewing your investment portfolio. Quarterly reviews are a common practice, allowing you to assess performance without overreacting to short-term market fluctuations. During these reviews, consider the following:

- Asset Allocation: Ensure your portfolio remains diversified and aligned with your family’s risk tolerance and long-term goals.

- Performance Evaluation: Compare the performance of your investments against relevant benchmarks to identify any underperforming assets.

- Market Trends: Stay informed about economic indicators and market trends that could impact your investment strategy.

Effective monitoring also involves setting predefined criteria for making adjustments. Establish clear guidelines on when to rebalance your portfolio or divest from certain assets. This proactive approach helps in maintaining discipline and prevents emotional decision-making. Utilize tools such as automated alerts or portfolio tracking apps to keep you informed and in control. By integrating these practices, your family’s investment strategy will be more resilient and adaptable to changing financial landscapes.

{kind=link}