Facing the challenge of mounting debt can feel like navigating a financial labyrinth, where every turn seems to lead to further stress and uncertainty. However, the journey to financial freedom does not have to deplete your hard-earned savings or compromise your future security. In this article, we will guide you through effective strategies to eliminate debt while preserving your savings, empowering you to regain control over your finances with confidence. With practical advice and proven methods, you’ll learn how to balance debt repayment with maintaining a healthy financial cushion, ensuring a stable and secure path forward. Let’s embark on this journey together, transforming debt from a daunting burden into a manageable hurdle.

Understanding Your Debt Landscape and Setting Realistic Goals

Embarking on the journey to financial freedom requires a clear understanding of your current financial obligations. Begin by assessing your debt landscape. Identify all outstanding debts, including credit cards, student loans, and personal loans. Create a comprehensive list detailing the creditor, outstanding balance, interest rate, and minimum monthly payment for each debt. This will provide a clear picture of where you stand and allow you to prioritize debts based on interest rates and balances.

Once you have a clear understanding, it’s time to set realistic and achievable goals. Consider the following steps to establish a strategic plan:

- Prioritize High-Interest Debts: Focus on paying off debts with the highest interest rates first to minimize the total interest paid over time.

- Create a Budget: Allocate a specific portion of your monthly income towards debt repayment while ensuring that your essential needs and a modest savings plan are met.

- Set Milestones: Break down your overall debt into smaller, manageable goals. Celebrate small victories as you achieve each milestone to stay motivated.

- Consider Professional Advice: If needed, consult a financial advisor to tailor a debt repayment plan that aligns with your financial situation and goals.

By methodically navigating your debt landscape and setting practical goals, you can take charge of your financial future without sacrificing your savings.

Crafting a Strategic Budget to Optimize Cash Flow

When aiming to eliminate debt without compromising your savings, crafting a well-thought-out budget is essential. Start by analyzing your current financial situation to identify income sources and categorize expenses. Distinguish between needs and wants to determine where cuts can be made without affecting your quality of life. A strategic budget should include:

- Fixed Expenses: Rent, mortgage, utilities, and other non-negotiable payments.

- Variable Expenses: Groceries, transportation, and entertainment—areas where spending can be adjusted.

- Debt Repayment: Prioritize high-interest debts while maintaining minimum payments on others.

- Savings Contribution: Allocate a small percentage to savings to avoid feeling deprived.

Integrate tools like budgeting apps or spreadsheets to track your spending and adjust your plan as needed. Regularly review and refine your budget to ensure it aligns with your financial goals, allowing you to pay down debt while preserving your savings.

Leveraging Negotiation Tactics with Creditors

Mastering negotiation tactics with creditors can be a game-changer in your journey to becoming debt-free. The key is to approach each conversation with confidence and a well-thought-out strategy. Start by understanding your financial situation in detail, which will enable you to communicate clearly and assertively. Remember, creditors are often open to negotiation because they prefer receiving partial payment over none at all. Here are some tactics to consider:

- Know Your Numbers: Be ready with a detailed breakdown of your income, expenses, and debts. This transparency can help build trust and facilitate a more productive discussion.

- Offer a Lump Sum Payment: If possible, propose a one-time payment that is lower than the total owed. Creditors might accept this as a compromise, especially if it’s immediate.

- Request a Lower Interest Rate: By reducing the interest rate, you can significantly decrease your monthly payments and the total amount paid over time.

- Propose a Payment Plan: Suggest a realistic installment plan that fits your budget. Creditors are more likely to agree if they see you’re committed to repaying the debt.

- Highlight Your History: If you have a good payment history, use it to your advantage to negotiate better terms.

These tactics, when applied correctly, can help you navigate the complex world of debt repayment without depleting your savings, allowing you to regain financial stability.

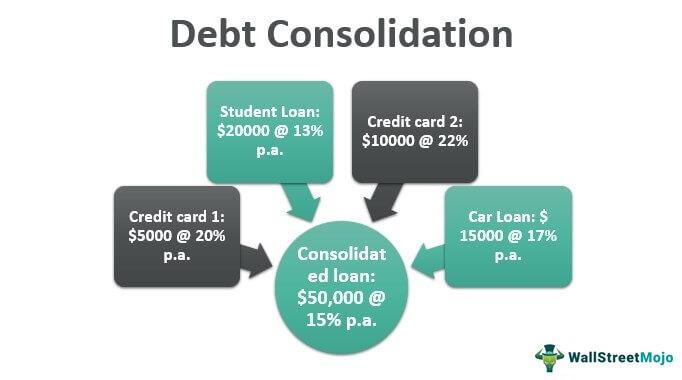

Exploring Debt Consolidation and Refinancing Options

When managing multiple debts, it can feel like you’re juggling flaming torches while balancing on a tightrope. Fortunately, debt consolidation and refinancing can offer a more stable footing. Debt consolidation involves combining all your outstanding debts into a single loan with a lower interest rate, simplifying your monthly payments and potentially reducing the total interest paid over time. On the other hand, refinancing is the process of replacing an existing loan with a new one, often with better terms and lower interest rates. Both options can streamline your financial obligations, allowing you to focus on paying off your debt more efficiently.

- Lower Interest Rates: Both consolidation and refinancing aim to reduce the interest rates on your debts, which can save you money in the long run.

- Single Monthly Payment: By consolidating debts, you combine them into one loan, making it easier to manage with just one payment each month.

- Improved Credit Score: Successfully managing a consolidated loan can positively impact your credit score over time.

It’s important to assess your financial situation carefully before deciding on either option. Compare interest rates, fees, and terms from different lenders to find the best solution tailored to your needs. Remember, the ultimate goal is to regain control over your finances without depleting your savings, so choose the path that aligns with your financial objectives.

{kind=link}