In today’s rapidly evolving financial landscape, crafting a robust family investment strategy has become more crucial than ever. As families navigate the complexities of economic uncertainties, inflationary pressures, and an array of investment opportunities, a well-structured approach can serve as a cornerstone for financial stability and growth. This article delves into the essential components of a successful family investment strategy, offering analytical insights to help families align their financial goals with practical investment choices. By examining risk tolerance, time horizons, and asset diversification, we aim to empower families with the confidence and knowledge needed to build a sustainable financial future. Join us as we explore the intricacies of creating a family investment strategy that not only withstands market fluctuations but also fosters long-term prosperity.

Identifying Your Familys Financial Goals and Priorities

Understanding what your family values financially is the cornerstone of a successful investment strategy. Start by gathering all family members for an open discussion about financial aspirations. These conversations can reveal a variety of goals, such as:

- Long-term security: Building a substantial retirement fund or saving for future generations.

- Education: Setting aside money for children’s college tuition or professional development.

- Homeownership: Purchasing a family home or investing in real estate properties.

- Travel and experiences: Allocating funds for family vacations or cultural experiences.

- Entrepreneurship: Starting a family business or supporting individual entrepreneurial pursuits.

Identifying these priorities will not only help you align your investment strategy with your family’s values but also foster a sense of shared commitment. Once these goals are clearly defined, you can categorize them into short-term, medium-term, and long-term objectives, allowing you to tailor your investment approach to meet these timelines effectively.

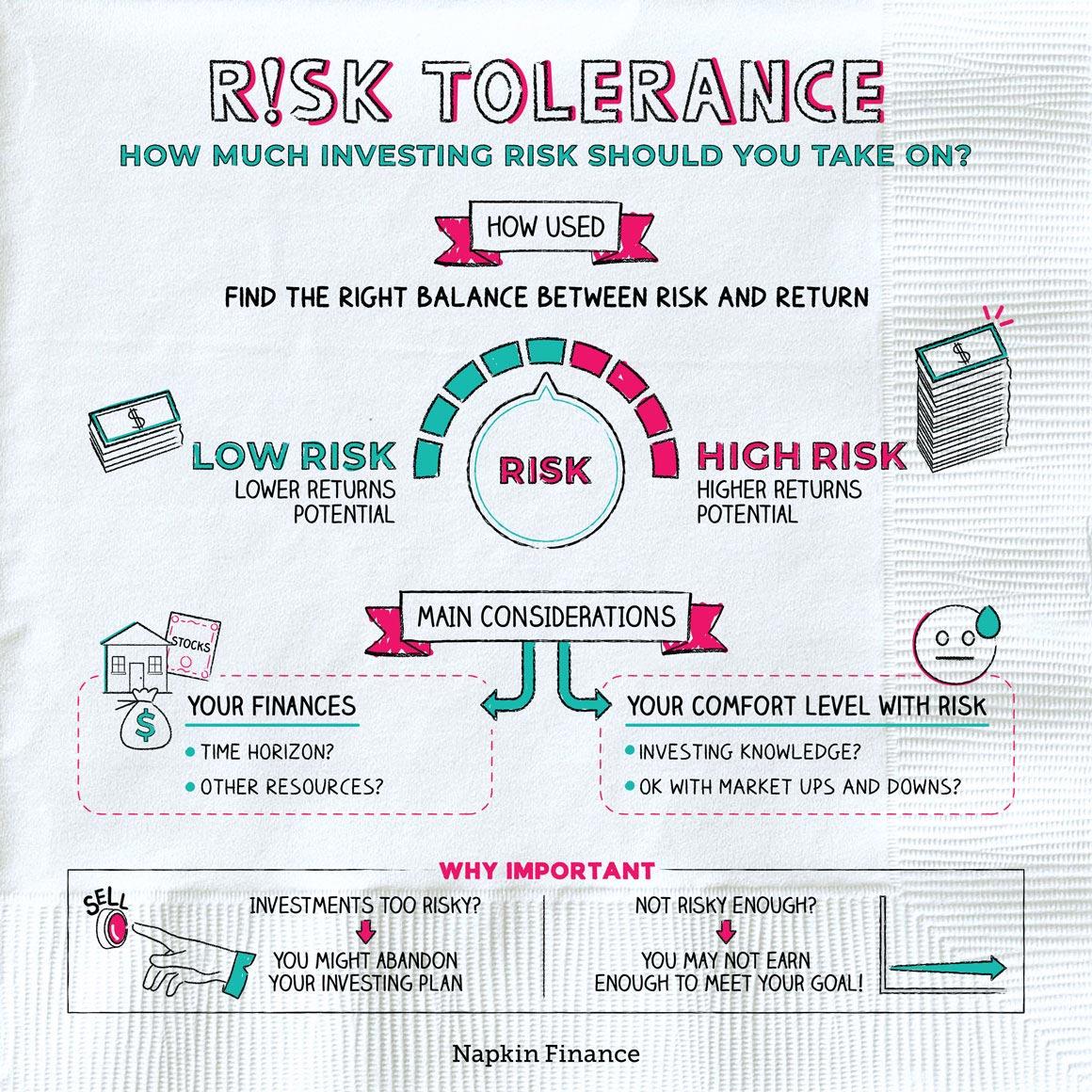

Assessing Risk Tolerance and Time Horizons for Optimal Investment Choices

When crafting a family investment strategy, understanding each family member’s risk tolerance and time horizon is essential for making informed decisions. Risk tolerance varies significantly among individuals; some may prefer the steady, predictable growth of bonds, while others are comfortable with the volatility of stocks. To gauge risk tolerance, consider factors such as financial stability, investment knowledge, and past experiences with financial markets. Engage in open discussions to ensure everyone’s comfort level is considered, thus fostering a cohesive investment approach.

Equally important is aligning investment choices with appropriate time horizons. Different goals—such as funding a child’s education or planning for retirement—require varying timelines and investment strategies. Consider the following:

- Short-term goals: Opt for low-risk investments like savings accounts or short-term bonds, ensuring liquidity and capital preservation.

- Medium-term goals: Diversify with a mix of bonds and equities to balance growth potential and risk.

- Long-term goals: Embrace higher-risk investments such as stocks or real estate, capitalizing on the potential for greater returns over time.

By carefully assessing these elements, families can create a robust investment strategy that aligns with their collective goals and individual preferences, setting the stage for financial success.

Diversifying Investments to Balance Growth and Security

In crafting a robust family investment strategy, it’s crucial to understand the importance of spreading investments across various asset classes to mitigate risks and enhance potential returns. Diversification acts as a shield, protecting the family’s financial future from the volatility of individual markets. By allocating resources to a mix of assets such as stocks, bonds, real estate, and commodities, families can achieve a harmonious balance between growth and security. This approach not only reduces the impact of any single asset’s poor performance but also provides opportunities for gains in different market conditions.

- Stocks: Offer potential for high returns but come with higher risk.

- Bonds: Provide steady income and are generally considered safer.

- Real Estate: Can offer both income and capital appreciation.

- Commodities: Act as a hedge against inflation and market volatility.

Furthermore, regularly reviewing and adjusting the investment portfolio is vital to ensure alignment with the family’s financial goals and risk tolerance. Leveraging tools like asset allocation calculators and financial advisory services can aid in making informed decisions, ensuring the strategy remains dynamic and responsive to both market changes and family needs.

Implementing and Monitoring the Strategy for Long-term Success

Crafting a robust family investment strategy is only the beginning; implementing and monitoring it is crucial for ensuring long-term success. Start by clearly defining roles and responsibilities within the family, ensuring that everyone is aligned with the strategic goals. Regular communication is key—schedule monthly or quarterly family meetings to discuss progress and adjust plans as necessary. Use these meetings to review performance metrics and ensure that the strategy remains aligned with both family values and financial goals.

To effectively monitor the strategy, employ a combination of digital tools and manual tracking. Consider using financial management software to provide real-time insights into your portfolio’s performance. Key actions include:

- Setting up automated alerts for market changes that could impact your investments.

- Establishing benchmarks for measuring performance against industry standards.

- Conducting annual reviews to reassess risk tolerance and investment goals.

This vigilant approach ensures that the family investment strategy remains dynamic, adapting to both external market conditions and internal family circumstances, ultimately driving sustainable financial growth.

{kind=link}