In the ever-evolving landscape of personal finance, establishing and maintaining robust family financial goals is a cornerstone for long-term success. As families navigate through the complexities of everyday expenses, education costs, retirement planning, and unforeseen emergencies, a strategic approach to financial management becomes imperative. This article delves into the essential steps and considerations that families must undertake to secure their financial future. With a focus on building a solid financial foundation, setting realistic and achievable goals, and implementing disciplined saving and investment strategies, we aim to equip you with the knowledge and tools necessary to foster financial stability and prosperity for generations to come. Whether you are just starting your family journey or looking to refine your financial strategy, understanding and prioritizing long-term financial goals is key to ensuring a secure and thriving future.

Establishing a Robust Family Budget for Future Security

Crafting a strong financial framework for your family requires a meticulous approach to budgeting, ensuring both current stability and future security. Begin by evaluating all income sources and categorizing your expenses into essential and non-essential. Prioritize essential expenses such as housing, food, and healthcare. Once these are accounted for, allocate funds towards non-essential categories, but always leave room for savings.

- Emergency Fund: Aim to save at least three to six months’ worth of living expenses to safeguard against unforeseen circumstances.

- Debt Reduction: Focus on paying off high-interest debts first, using strategies like the avalanche or snowball method.

- Retirement Savings: Contribute consistently to retirement accounts, taking advantage of any employer matching programs.

- Education Fund: Consider setting up a college savings plan if you have children, to alleviate future educational costs.

Adopting a flexible yet disciplined approach to budgeting not only helps in meeting immediate financial needs but also in achieving long-term objectives. Regularly review and adjust your budget to accommodate changes in income or expenses, ensuring your family’s financial goals remain on track.

Strategic Investment Planning for Multi-Generational Wealth

Crafting a strategy for multi-generational wealth involves understanding the unique financial needs and aspirations of each family member, while also establishing a robust framework for future generations. It requires a comprehensive approach that includes diverse asset allocation, tax-efficient strategies, and long-term growth plans. Families should focus on creating a balance between risk and reward, ensuring that investments are not only aligned with current financial goals but also resilient to economic shifts over time.

- Diversify Investments: Spread investments across various asset classes such as equities, real estate, and fixed income to mitigate risks.

- Incorporate Estate Planning: Develop a solid estate plan that includes wills, trusts, and succession planning to ensure smooth transitions.

- Educate Younger Generations: Provide financial literacy education to younger family members to empower them with the knowledge to manage wealth responsibly.

- Leverage Tax Advantages: Utilize tax-advantaged accounts and strategies to maximize wealth preservation across generations.

By establishing clear financial objectives and employing strategic investment techniques, families can safeguard their wealth and ensure prosperity for generations to come. This proactive approach not only protects assets but also aligns with the evolving needs and values of the family. Engaging with financial advisors to tailor strategies to specific family circumstances can further enhance the effectiveness of these plans.

Safeguarding Assets with Comprehensive Insurance Solutions

In the pursuit of achieving family financial goals, ensuring the protection of your assets with a well-rounded insurance strategy is crucial. By prioritizing comprehensive insurance solutions, families can safeguard their financial future against unforeseen events. This involves evaluating various insurance options, from health and life insurance to home and auto coverage, each tailored to your family’s unique needs and long-term objectives.

- Life Insurance: Secure your family’s financial stability by choosing policies that provide adequate coverage for your dependents in case of unexpected loss.

- Health Insurance: Opt for plans that cover routine check-ups and emergencies, minimizing out-of-pocket expenses and ensuring access to quality healthcare.

- Property Insurance: Protect your home and valuable assets from natural disasters and theft with comprehensive home insurance policies.

- Auto Insurance: Choose coverage that not only meets legal requirements but also provides additional protection against accidents and liabilities.

By incorporating these strategies into your financial planning, you create a robust safety net that helps your family navigate life’s uncertainties while keeping your long-term financial goals intact. Remember, the key to success lies in regularly reviewing and updating your insurance policies to adapt to changing circumstances and needs.

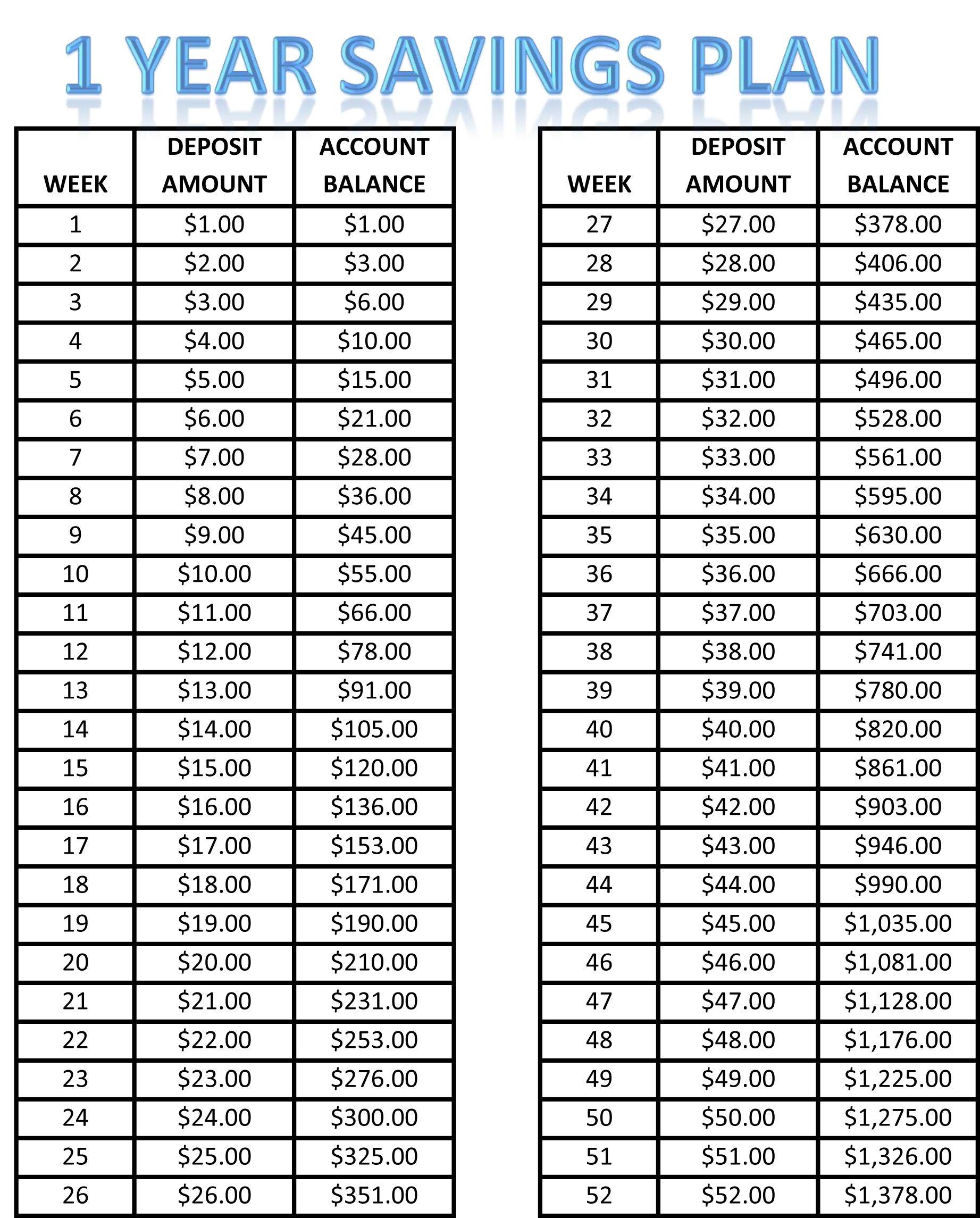

Creating an Effective Savings Plan for Educational and Retirement Needs

Establishing a savings plan that effectively caters to both educational and retirement needs requires a balanced approach. Start by assessing your current financial situation, including income, expenses, and any existing savings. Allocate funds specifically for education and retirement, ensuring that each category receives appropriate attention. Consider creating separate accounts to avoid mixing funds, and take advantage of any tax-advantaged accounts available, such as 529 plans for education and IRAs or 401(k)s for retirement.

- Prioritize your goals: Determine which goal is more urgent based on your family’s timeline. If college is on the horizon, you may need to focus on education savings initially.

- Automate your savings: Set up automatic transfers to your savings accounts to ensure consistency and discipline in your saving habits.

- Review and adjust regularly: Life changes and so should your financial plan. Schedule regular reviews to ensure your savings strategy remains aligned with your goals.

Engage with financial advisors to explore investment opportunities that could potentially grow your savings over time, balancing risk with the timeline for each goal. Remember, a well-structured savings plan not only secures future educational needs but also builds a comfortable retirement nest egg, paving the way for long-term financial success.

{kind=link}