Navigating the financial landscape as newlyweds can be both exciting and daunting. As you embark on this new chapter together, establishing a strong financial foundation is crucial to ensuring a stable and prosperous future. Smart budgeting is not just about managing expenses; it’s about aligning your financial goals with your shared life ambitions. In this guide, we delve into authoritative and practical budgeting strategies tailored specifically for newlywed families. From setting clear financial goals to managing joint accounts and planning for long-term investments, these tips will equip you with the knowledge and tools to make informed financial decisions. Embrace the journey of smart budgeting and lay the groundwork for a lifetime of financial harmony and success.

Establishing a Joint Financial Vision for Your Future

Creating a shared financial path is crucial for newlywed families, ensuring both partners are aligned in their monetary goals and aspirations. Begin by holding an open discussion about individual financial habits and future objectives. This lays the groundwork for a robust, unified strategy. Consider these key elements to establish a harmonious financial future:

- Define Common Goals: Whether it’s buying a home, saving for travel, or planning for children, clearly outline what you both want to achieve. Use these goals to guide your budgeting decisions.

- Establish a Joint Budget: Develop a comprehensive budget that accommodates both shared and individual expenses. Ensure that both partners have input and agree on how money is allocated.

- Regular Financial Check-ins: Schedule monthly or quarterly meetings to review your budget, discuss progress toward goals, and make necessary adjustments. This keeps both parties accountable and informed.

- Emergency Fund Prioritization: Build a robust emergency fund to safeguard against unexpected expenses. This fund should be a top priority, offering peace of mind and financial security.

By fostering open communication and working collaboratively on your finances, you’ll lay the foundation for a prosperous and fulfilling future together.

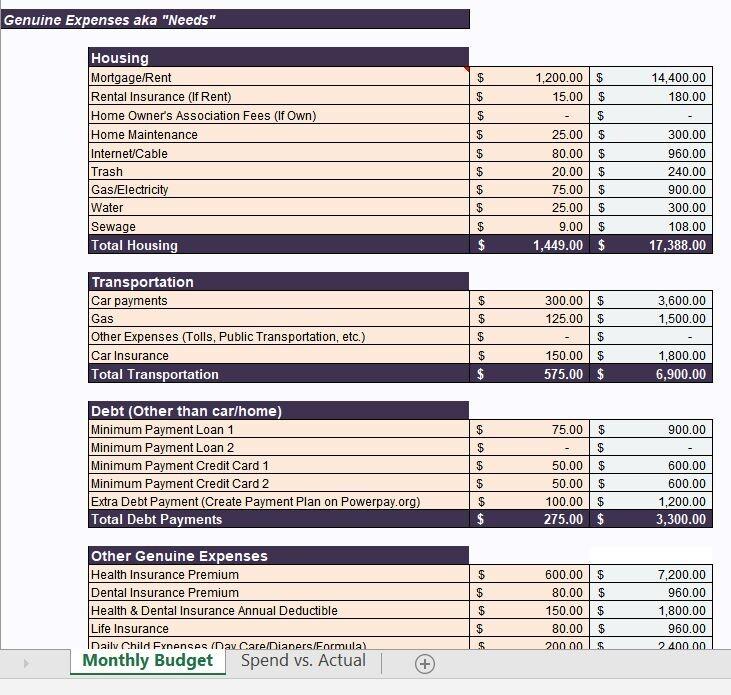

Crafting a Realistic Monthly Budget That Accommodates Both Partners

Creating a financial plan that respects both partners’ needs and aspirations is crucial for newlywed families. Begin by having an open dialogue about each partner’s financial situation, goals, and spending habits. This transparency is the cornerstone of a successful budget. Utilize a shared spreadsheet or budgeting app to track income and expenses, ensuring both partners have access and input. Remember, this is not just about numbers; it’s about aligning your financial future together.

To accommodate both partners effectively, consider these strategies:

- Set common financial goals: Discuss and agree on short-term and long-term objectives, such as saving for a home or a vacation.

- Allocate personal spending money: Ensure each partner has a discretionary amount to spend as they wish, which can help prevent feelings of restriction.

- Divide responsibilities: Assign tasks like bill payments and expense tracking to ensure equal participation in managing finances.

- Regularly review the budget: Schedule monthly budget meetings to discuss progress, adjust allocations, and address any financial concerns.

By embracing these practices, newlywed couples can craft a budget that not only supports their financial well-being but also strengthens their partnership.

Effective Strategies for Managing and Reducing Shared Expenses

Managing shared expenses can be a breeze with the right approach. Start by creating a joint budget that outlines all the monthly expenditures. Use tools like Google Sheets or budgeting apps to keep everything organized and accessible to both partners. It’s crucial to have regular financial meetings to review expenses, adjust budgets, and ensure you’re on track with your financial goals. Make sure to establish clear communication channels to discuss any changes or unexpected costs.

- Set clear financial goals: Decide together on short-term and long-term goals, such as saving for a vacation or buying a house.

- Allocate funds for individual spending: Ensure both partners have a personal allowance for individual needs, reducing potential conflicts.

- Use a joint bank account for shared expenses: This simplifies tracking and accountability for bills, groceries, and other shared costs.

- Regularly review and adjust: Life changes, and so should your budget. Be flexible and open to revising your strategies as needed.

Implementing these strategies not only helps in effectively managing shared expenses but also strengthens the financial partnership between newlyweds, paving the way for a harmonious and financially sound future together.

Building an Emergency Fund to Safeguard Your Familys Financial Stability

One of the most crucial steps in ensuring financial security for your family is to establish an emergency fund. This fund acts as a financial buffer against unexpected expenses, such as medical emergencies, car repairs, or sudden job loss. Begin by setting a realistic goal for your emergency fund, typically three to six months’ worth of living expenses. This might seem daunting, but with strategic planning, it’s achievable.

- Automate Savings: Set up automatic transfers from your checking account to your savings account each month. This way, saving becomes a consistent habit.

- Cut Unnecessary Expenses: Analyze your spending habits and identify areas where you can cut back, such as dining out or subscription services.

- Increase Income: Consider side gigs or freelance work to boost your savings rate without affecting your current budget.

- Use Windfalls Wisely: Allocate bonuses, tax refunds, or any unexpected cash influx directly into your emergency fund.

By integrating these practices into your financial routine, you not only build a safety net but also cultivate a disciplined approach to money management. This foresight and preparedness can offer peace of mind and stability in times of uncertainty.

{kind=link}