In today’s complex financial landscape, managing debt across multiple creditors can feel like navigating a maze without a map. Yet, with the right strategies and a disciplined approach, it is entirely possible to take control of your financial obligations and steer your way toward a debt-free future. This article delves into the best practices for effectively managing debt across various creditors, offering a clear and confident guide to help you streamline your payments, reduce financial stress, and ultimately achieve financial stability. Whether you’re juggling credit card balances, personal loans, or other forms of debt, these expert-recommended strategies will empower you to organize your financial commitments, prioritize payments, and make informed decisions that align with your long-term financial goals. Join us as we explore actionable steps to regain control over your finances and transform your debt management journey into a pathway of empowerment and success.

Assess Your Financial Situation with Precision

In navigating the complexities of managing debt across multiple creditors, it’s crucial to have a clear and precise understanding of your financial landscape. Begin by creating a detailed list of all your outstanding debts. Include the following information for each creditor:

- Outstanding balance

- Interest rate

- Minimum monthly payment

- Due date

Once you have this information at your fingertips, prioritize your debts. Focus on high-interest debts first, as they cost you more over time. Consider strategies such as the avalanche method, which targets high-interest debts, or the snowball method, which focuses on smaller debts to build momentum. Regularly update your list to reflect any changes in your financial situation, ensuring you stay on track and maintain control over your debt management strategy.

Strategize an Effective Debt Repayment Plan

Creating a robust plan to tackle debt from multiple sources requires a structured approach that focuses on prioritization and consistency. Start by listing all your debts, including details like the total amount owed, interest rates, and minimum monthly payments. This will provide a clear overview of your financial obligations. Once you have a comprehensive list, consider adopting either the debt snowball or debt avalanche method. The snowball method involves paying off the smallest debts first to gain momentum, while the avalanche method focuses on eliminating high-interest debts to save money in the long run. Choose the strategy that aligns best with your financial goals and psychological comfort.

Consistency is key to successful debt repayment. Establish a realistic budget that accommodates your debt payments while covering essential expenses. Utilize digital tools or apps to track your progress and set up automated payments to avoid missing due dates. Furthermore, if possible, allocate any extra income or windfalls directly toward your debts. Effective communication with creditors can also provide relief; negotiate for lower interest rates or explore consolidation options if necessary. By adhering to these practices, you’ll not only manage your debt more effectively but also cultivate healthier financial habits for the future.

Communicate Proactively with Creditors

Effective communication is key when juggling debts across various creditors. Reach out early to inform them of your situation. Proactive engagement can lead to more flexible repayment options and demonstrate your commitment to settling your debts responsibly. Start by creating a list of all your creditors, noting down their contact information, the amount owed, and the due dates. This will help you stay organized and prepared for any discussions.

- Be transparent about your financial situation. Honesty fosters trust and can lead to more favorable terms.

- Negotiate for lower interest rates or revised payment plans. Creditors are often willing to adjust terms to ensure they receive payments.

- Document all communications for future reference. This can be crucial if any disputes arise.

- Schedule regular check-ins to keep creditors updated on your progress and to renegotiate terms if necessary.

By maintaining open lines of communication, you can reduce stress and potentially avoid penalties, creating a more manageable debt repayment journey.

Utilize Financial Tools to Stay on Track

Staying organized while managing debt across multiple creditors can feel overwhelming, but financial tools can make this process more manageable. Consider using budgeting apps or software that allow you to track all your accounts in one place. These tools often provide features such as automatic expense categorization, payment reminders, and debt payoff calculators. By having a clear overview of your financial situation, you can prioritize debts effectively and ensure timely payments, ultimately helping to improve your credit score.

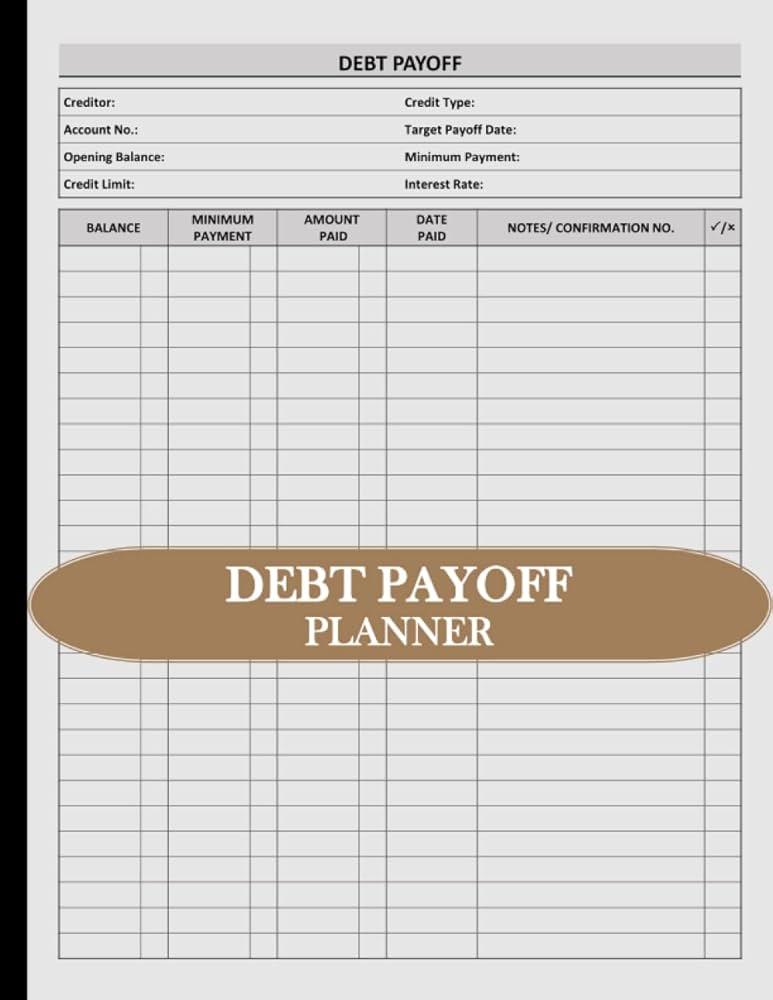

Another invaluable resource is a debt management planner, which can be a digital tool or a physical notebook. Such planners help you outline all outstanding debts, including interest rates and minimum payments. Utilizing these tools can lead to better financial decision-making and a more strategic approach to paying down debt. Here’s how they can help you stay on track:

- Consolidation Insights: Some apps provide insights into whether debt consolidation could benefit your situation.

- Customized Alerts: Set alerts for upcoming due dates to avoid late fees.

- Progress Tracking: Visualize your debt reduction journey to stay motivated.

{kind=link}