Purchasing a home is one of life’s most significant milestones, offering a sense of stability and personal achievement. However, along with the excitement of homeownership comes the responsibility of managing new financial obligations. Navigating the world of mortgages, property taxes, and maintenance costs can be daunting, especially when balancing existing debts. Fear not—taking control of your financial future is entirely within your grasp. In this guide, we will explore the best strategies to manage debt effectively after buying a home, empowering you to maintain financial health and enjoy the comforts of your new abode with confidence and peace of mind.

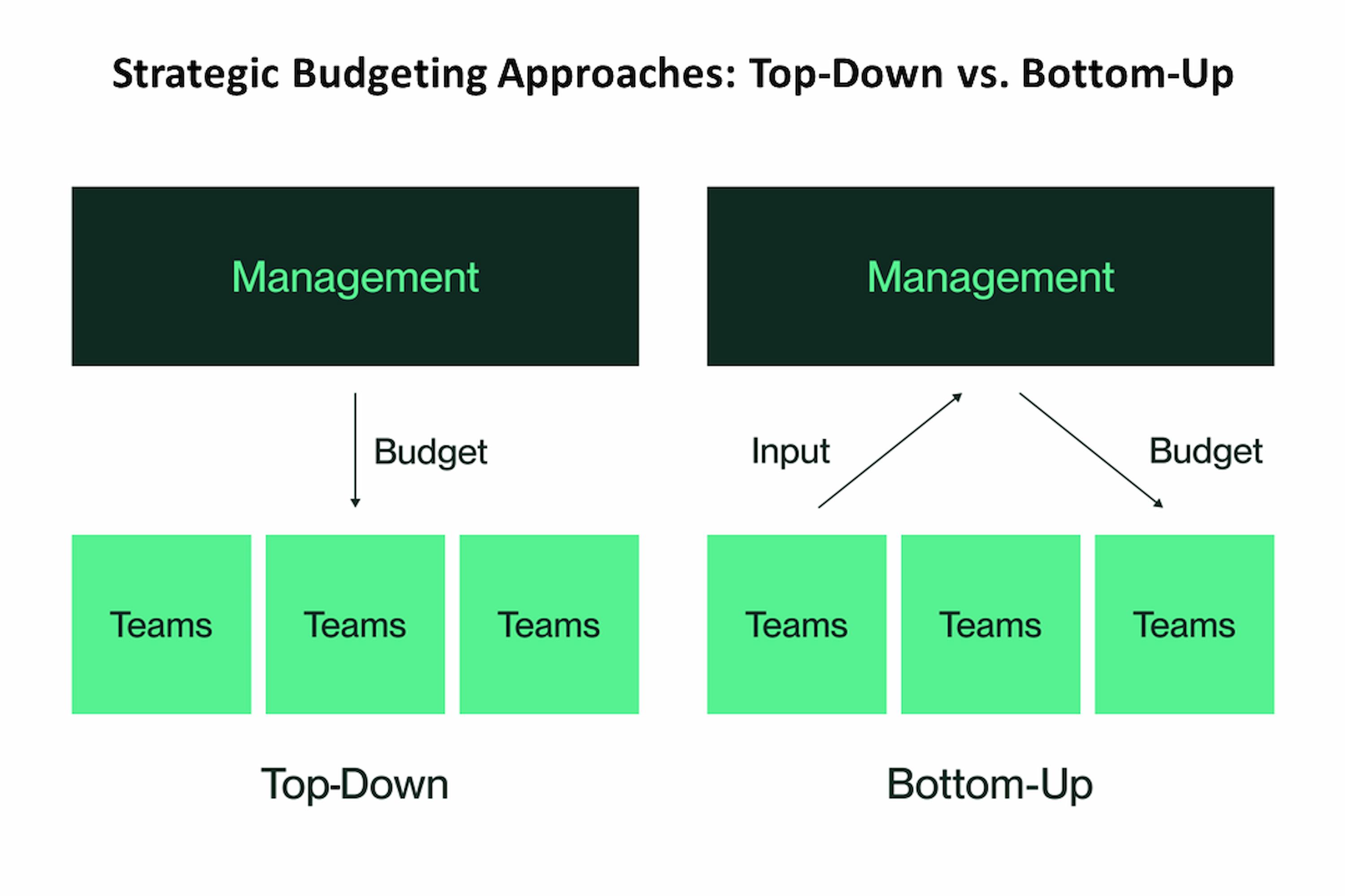

Craft a Strategic Budget to Align with Your New Financial Reality

Transforming your financial strategy post-home purchase involves a meticulous approach to budgeting that ensures your expenses and income are in sync with your new obligations. Start by analyzing your current financial landscape and identifying areas where adjustments are necessary. Consider the following strategic steps to maintain financial stability:

- Evaluate Your Expenses: Categorize and scrutinize your monthly expenses. This will help identify discretionary spending that can be reduced or eliminated to free up funds for debt repayment.

- Prioritize Debt Payments: Focus on high-interest debts first, such as credit cards, to minimize interest payments. You might consider the debt avalanche or debt snowball method, depending on what motivates you more effectively.

- Automate Savings and Payments: Set up automatic transfers to savings accounts and automate debt payments to ensure consistency and avoid missed payments, which can lead to additional fees.

- Review and Adjust Regularly: Revisit your budget monthly to ensure it aligns with any changes in income or expenses. Adjustments may be necessary as your financial situation evolves.

By proactively managing your budget with these strategies, you can effectively navigate your new financial reality and work towards a more secure and debt-free future.

Prioritize High-Interest Debt to Minimize Long-Term Costs

When managing your financial obligations after purchasing a home, it’s crucial to focus on debts with the highest interest rates first. These debts, often including credit cards and certain personal loans, can quickly accumulate and overshadow your financial progress if not addressed promptly. By prioritizing these, you can significantly reduce the total interest paid over time and free up more of your income for other essential expenses or savings.

- Identify High-Interest Debts: List all your debts, highlighting those with the highest interest rates. Credit card balances often fall into this category, along with some personal loans.

- Develop a Payment Strategy: Consider the avalanche method, which involves paying the minimum on all debts while allocating extra funds towards the highest interest debt. This method can save you more money over time compared to other strategies.

- Consolidate Wisely: If feasible, explore consolidation options to combine multiple high-interest debts into a single, lower-interest payment. This can streamline your payments and potentially reduce your interest costs.

By tackling high-interest debts head-on, you not only alleviate immediate financial pressure but also position yourself for a more secure and prosperous financial future.

Utilize Refinancing Opportunities to Optimize Mortgage Terms

Once you’ve settled into your new home, it’s crucial to regularly evaluate your mortgage terms and explore refinancing opportunities to enhance your financial stability. Refinancing can help lower your interest rate, reduce your monthly payments, or even shorten the loan term. By doing so, you can potentially save thousands over the life of the loan. Here are some strategic steps to consider:

- Monitor Interest Rates: Keep an eye on market trends. If rates drop significantly below your current rate, it might be a good time to refinance.

- Improve Your Credit Score: A higher credit score can qualify you for better refinancing terms. Pay down existing debts and make timely payments to boost your score.

- Evaluate Loan Terms: Consider switching from a variable to a fixed-rate mortgage for more predictable payments, or vice versa, depending on your financial goals.

- Consult a Financial Advisor: Professional advice can help you understand the potential savings and costs involved in refinancing.

By proactively managing your mortgage through refinancing, you can optimize your debt management strategy and potentially unlock additional financial opportunities.

Leverage Financial Tools and Resources for Effective Debt Management

In the journey to manage your debt effectively after purchasing a home, it’s crucial to make the most of the financial tools and resources at your disposal. Budgeting apps and expense tracking software can help you gain a clear view of your financial health, allowing you to allocate funds efficiently and avoid overspending. Consider utilizing online debt calculators to understand your repayment timelines and the impact of additional payments.

Engage with credit counseling services to receive professional advice tailored to your financial situation. Many of these services offer workshops and webinars that can enhance your understanding of debt management strategies. Additionally, take advantage of automated payment systems to ensure timely payments, reducing the risk of late fees and interest charges. By leveraging these resources, you can stay on top of your financial obligations and work towards a debt-free future.

{kind=link}