Debt can feel like a daunting mountain to climb, but with the right strategy, you can transform it into a manageable journey towards financial freedom. Welcome to your comprehensive guide on creating a debt repayment plan that truly works. Whether you’re juggling student loans, credit card balances, or personal loans, this article will equip you with practical steps and effective techniques to regain control over your finances. With confidence and determination, you’ll learn how to prioritize debts, set achievable goals, and implement a plan that aligns with your lifestyle. Let’s embark on this empowering path together, turning your debt repayment dreams into a tangible reality.

Assess Your Financial Situation and Set Clear Goals

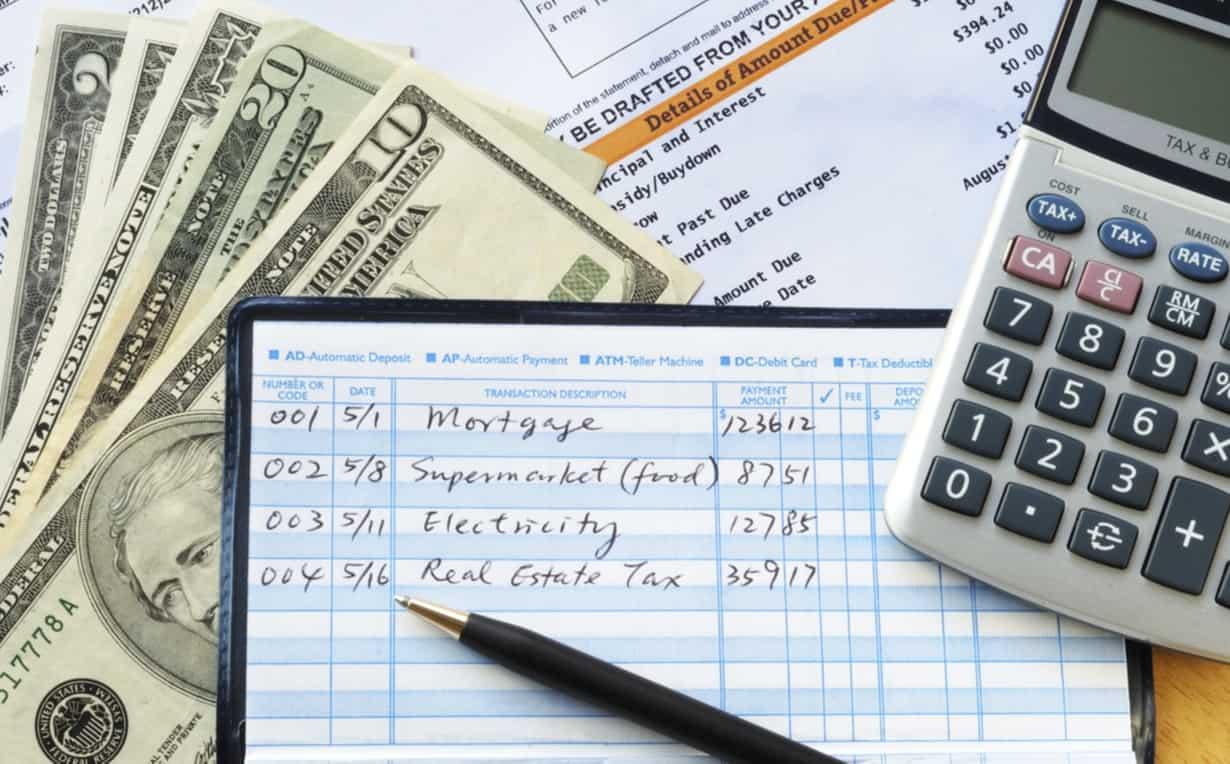

Before embarking on a debt repayment journey, it’s crucial to gain a comprehensive understanding of your current financial landscape. Begin by compiling a detailed list of all your debts, including the amount owed, interest rates, and minimum monthly payments. This inventory will provide a clear picture of where you stand and help you identify which debts are the most urgent to address. Next, take stock of your monthly income and expenses to determine how much you can realistically allocate towards debt repayment each month. This step is vital for setting achievable goals and avoiding overcommitting yourself financially.

Once you have a firm grasp of your financial situation, it’s time to set clear, actionable goals. Consider the following:

- Prioritize High-Interest Debt: Focus on paying off debts with the highest interest rates first to reduce the total amount of interest paid over time.

- Establish a Debt-Free Timeline: Decide on a target date for becoming debt-free and break it down into smaller milestones to track your progress.

- Create a Buffer: Set aside a small emergency fund to prevent unexpected expenses from derailing your repayment plan.

By aligning your repayment strategy with your financial reality and setting specific objectives, you lay the groundwork for a successful debt elimination journey.

Choose the Right Debt Repayment Strategy for You

Finding the most effective way to tackle your debt can be a game-changer in your financial journey. To start, consider your personal financial situation, the types of debt you hold, and your overall financial goals. Here are a few strategies to evaluate:

- Debt Snowball Method: Focus on paying off your smallest debts first, gaining momentum as you eliminate each one. This method can be highly motivating as you quickly see progress.

- Debt Avalanche Method: Prioritize paying off debts with the highest interest rates first. This approach minimizes the total interest paid over time, saving you money in the long run.

- Debt Consolidation: Combine multiple debts into a single loan with a lower interest rate. This simplifies payments and can reduce overall interest costs.

- Debt Management Plan: Work with a credit counseling agency to negotiate lower interest rates and create a manageable payment plan.

Each method has its benefits, so choose the one that aligns best with your financial circumstances and personality. Remember, consistency and commitment are key to any successful debt repayment strategy.

Create a Realistic Budget to Support Your Plan

Crafting a budget that aligns with your debt repayment plan is crucial to ensuring success. Begin by assessing your income and expenses to get a clear picture of your financial situation. Identify all sources of income, including salary, side gigs, or any other streams, and list them down. Next, categorize your expenses into essentials like rent, utilities, groceries, and non-essentials such as dining out or subscriptions. This will help you pinpoint areas where you can cut back to allocate more funds towards debt repayment.

Consider the following strategies to streamline your budget:

- Set realistic goals: Determine a fixed amount you can comfortably allocate to debt repayment each month without straining your finances.

- Automate payments: Set up automatic transfers to ensure timely payments, reducing the risk of late fees and improving your credit score.

- Track spending: Use budgeting apps or spreadsheets to monitor your expenses and adjust as necessary to stay on track.

- Emergency fund: Maintain a small fund for unexpected expenses to avoid derailing your repayment plan.

By adopting these measures, you create a financial environment conducive to tackling debt efficiently, ensuring that your repayment plan is not only feasible but sustainable over the long term.

Stay Committed and Monitor Your Progress Regularly

Consistency is the backbone of any successful debt repayment strategy. To ensure you’re on the right path, it’s crucial to keep a close eye on your progress. Regularly assess your financial situation to identify any deviations from your plan and make necessary adjustments. Use tools like budgeting apps or spreadsheets to track payments and expenses. This will not only provide a clear picture of your progress but also highlight areas where you can improve.

- Set regular check-ins: Schedule monthly reviews to evaluate your financial standing. These check-ins will help you stay motivated and focused on your goals.

- Celebrate small victories: Every milestone, no matter how small, deserves recognition. Rewarding yourself can boost morale and encourage you to keep pushing forward.

- Adjust as needed: Life is unpredictable. If unexpected expenses arise, be prepared to tweak your plan without losing sight of your ultimate goal.

By maintaining a diligent approach and adapting when necessary, you’ll find that your commitment transforms your debt repayment plan into a powerful tool for financial freedom.

{kind=link}