Rebuilding financial stability after repaying debt is a journey that demands strategic planning, disciplined execution, and a positive mindset. While the relief of overcoming debt is significant, the path to long-term financial security requires a thoughtful approach to managing and growing your newfound financial freedom. This guide is designed to equip you with the essential steps and insights to not only stabilize your finances but to thrive in a debt-free future. By focusing on budgeting, saving, and investing wisely, you can transform your financial landscape and secure a prosperous tomorrow. With confidence and clarity, let’s embark on the path to rebuilding your financial foundation.

Assessing Your Financial Landscape for a Fresh Start

Taking stock of your current financial situation is a crucial first step towards rebuilding stability. Begin by creating a comprehensive list of all your assets and liabilities. This includes not only your savings and investments but also any remaining debts, such as credit card balances or student loans. Identify areas of potential growth—like unused skills or hobbies that could generate extra income—and pinpoint any lingering financial obligations that need attention.

- Calculate your net worth to get a clear picture of where you stand.

- Review your credit report for any discrepancies that could affect your financial plans.

- Analyze your spending habits to identify unnecessary expenses that can be trimmed.

With a detailed understanding of your financial landscape, you can make informed decisions about your future. Consider consulting with a financial advisor to help you interpret this data and develop a personalized strategy. Remember, a well-mapped financial plan is your roadmap to a secure future.

Crafting a Sustainable Budget to Prevent Future Debt

Embarking on a journey towards financial stability begins with the development of a sustainable budget. This blueprint for your financial future not only helps manage your expenses but also acts as a safeguard against potential debt pitfalls. Start by assessing your income and essential expenses, such as housing, utilities, and groceries. It’s crucial to differentiate between needs and wants to allocate funds wisely. Prioritize savings by setting aside a percentage of your income each month, even if it’s a modest amount. This habit will gradually build a financial cushion for unforeseen circumstances.

- Track your spending habits: Utilize budgeting apps or spreadsheets to monitor your daily expenses. This will help identify areas where you can cut back.

- Establish a realistic savings goal: Whether it’s an emergency fund or a retirement account, having a clear target keeps you motivated.

- Review and adjust your budget regularly: Life changes, and so should your budget. Regular reviews ensure it remains aligned with your financial goals.

- Limit credit card usage: Aim to use cash or debit for daily purchases to avoid accumulating new debt.

By adopting these practices, you can effectively manage your finances and create a robust framework that prevents future debt, ensuring long-term financial health.

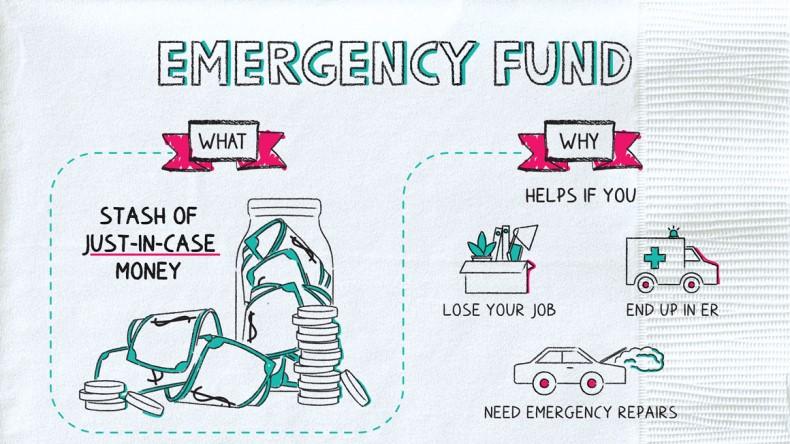

Building an Emergency Fund to Safeguard Against Uncertainty

Establishing a financial cushion is crucial once you’ve successfully paid off your debts. This buffer acts as a safety net, providing peace of mind during unforeseen circumstances. To get started, aim to save at least three to six months’ worth of living expenses. This may seem daunting at first, but breaking it down into manageable steps can make the process less overwhelming.

- Automate Savings: Set up automatic transfers from your checking account to a dedicated savings account. This ensures consistency and removes the temptation to spend.

- Prioritize Emergency Fund Contributions: Treat your emergency fund like a recurring bill. Allocate a specific amount each month, even if it means making small lifestyle adjustments.

- Cut Unnecessary Expenses: Review your monthly budget and identify areas where you can cut back. Redirect these savings to your emergency fund.

- Seek Additional Income: Consider taking on a side hustle or freelance work to boost your savings rate.

By implementing these strategies, you’ll not only build a robust emergency fund but also cultivate a disciplined approach to managing your finances, ensuring stability and security for the future.

Investing in Financial Education for Long-Term Success

Investing in your financial education is a strategic move that can significantly bolster your long-term success, especially after the challenges of debt repayment. Understanding personal finance principles is not just a skill but a necessity in today’s complex economic landscape. By equipping yourself with financial knowledge, you can make informed decisions, avoid common pitfalls, and build a robust financial foundation. Consider these key areas to focus on:

- Budgeting and Saving: Mastering the art of budgeting can help you allocate resources effectively and prioritize savings. Learn to track expenses, identify unnecessary spending, and set realistic saving goals.

- Investment Basics: Understanding the basics of investing can open doors to passive income and wealth growth. Start with the principles of stocks, bonds, and mutual funds to make informed choices.

- Credit Management: After clearing debt, it’s crucial to manage credit wisely. Learn about credit scores, responsible borrowing, and how to maintain a healthy credit history.

Online courses, workshops, and financial literacy books are excellent resources to deepen your understanding. Engage with content from reputable financial experts and platforms to stay updated on the latest trends and strategies. Remember, the more you know, the better equipped you are to steer your financial journey toward success. Empower yourself with knowledge and watch as financial stability becomes not just a goal, but a reality.

{kind=link}