Managing multiple loans can often feel like a juggling act, where each payment due date and interest rate demands your attention. However, structuring an effective debt repayment plan is not only possible but can also empower you to regain control over your financial future. In this article, we will guide you through the essential steps to organize your loans, prioritize payments, and choose strategies that align with your financial goals. Whether you’re dealing with student loans, credit card debt, or personal loans, our comprehensive approach will equip you with the tools and confidence needed to systematically reduce your debt and work towards financial freedom. Let’s embark on this journey to transform your debt repayment process into a streamlined, manageable plan.

Assess Your Financial Situation and Prioritize Loans

Understanding your current financial landscape is the cornerstone of a successful debt repayment plan. Start by gathering all your financial documents to get a comprehensive view of your financial health. This includes bank statements, pay stubs, credit card bills, and any other loan documents. By examining these, you’ll be able to calculate your total income and expenses, and determine how much you can realistically allocate towards debt repayment each month.

Once you have a clear picture of your finances, it’s crucial to prioritize your loans. Consider factors such as:

- Interest Rates: Focus on paying off high-interest loans first, as these accumulate debt faster.

- Loan Terms: Review the terms of each loan, identifying any that may have penalties for late payments or incentives for early repayment.

- Loan Amounts: Smaller loans can often be paid off quickly, freeing up funds to tackle larger debts.

By assessing your financial situation and strategically prioritizing your loans, you lay the groundwork for a more manageable and effective debt repayment strategy.

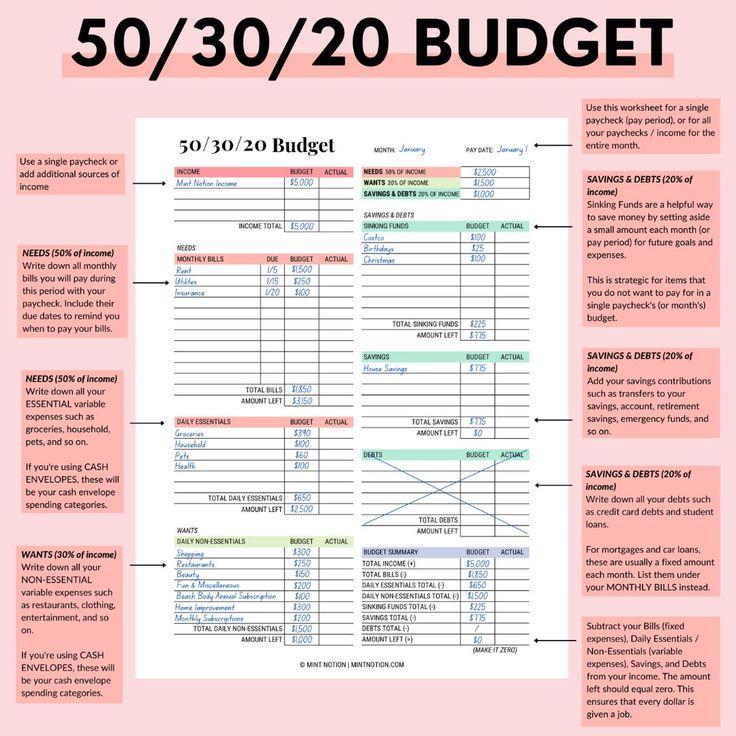

Craft a Realistic Budget to Optimize Repayment

To effectively tackle your loans, start by crafting a realistic budget that prioritizes repayment. Begin by listing all your sources of income and essential expenses. Once you’ve identified your discretionary spending, allocate a portion of this towards loan payments. This approach not only ensures that you’re living within your means but also helps in accelerating debt reduction.

- Assess Your Income: Total your monthly earnings, including salary, bonuses, and any side hustles.

- Track Your Expenses: Document every expense to see where your money goes. Differentiate between fixed and variable costs.

- Identify Cutbacks: Look for non-essential expenses that can be reduced or eliminated.

- Set Priorities: Allocate more funds to high-interest debts or those with the smallest balances to gain momentum.

By systematically organizing your finances, you’ll gain a clearer picture of your repayment capabilities. This empowers you to make informed decisions and adjustments, ensuring that your debt repayment plan is not just a financial obligation, but a manageable and strategic endeavor.

Explore Consolidation and Refinancing Options

When juggling multiple loans, finding the right strategy to streamline your payments can make all the difference. Consider consolidation as a way to merge your debts into a single loan with a potentially lower interest rate. This approach not only simplifies your financial obligations but can also reduce the overall cost of borrowing. Alternatively, refinancing allows you to replace an existing loan with a new one, ideally with better terms. Refinancing can be particularly beneficial if your credit score has improved since you initially took out your loans, potentially unlocking lower interest rates.

Here are some key points to consider when evaluating your options:

- Interest Rates: Look for options that offer a lower overall interest rate compared to your current loans.

- Loan Terms: Consider the length of the new loan term and how it aligns with your financial goals.

- Fees: Be aware of any fees associated with consolidating or refinancing, as these can impact the savings you might achieve.

- Repayment Flexibility: Ensure that the new loan terms offer flexibility in repayment, in case your financial situation changes.

By exploring these options, you can effectively manage your debt and work towards financial freedom with confidence.

Implement Effective Strategies for Consistent Progress

To ensure you are consistently making progress in your debt repayment journey, it is crucial to adopt strategies that align with your financial capabilities and goals. Begin by prioritizing your loans based on interest rates and balances. Consider the avalanche method, where you focus on repaying the loan with the highest interest rate first while making minimum payments on others. This approach minimizes the total interest paid over time. Alternatively, the snowball method—targeting the smallest debt first—can provide quick wins and boost motivation.

- Create a realistic budget: Allocate funds specifically for debt repayment, ensuring it is a non-negotiable part of your monthly expenses.

- Automate payments: Set up automatic transfers to avoid missed payments and reduce the temptation to use the funds elsewhere.

- Regularly review and adjust: Monthly reviews of your financial situation can help you adapt your strategies, ensuring they remain effective as circumstances change.

{kind=link}