In today’s rapidly evolving financial landscape, securing a robust educational future for your children requires more than just setting aside money. With the rising costs of tuition and associated educational expenses, selecting the right savings account is crucial for maximizing your investment and ensuring your child’s academic success. This article confidently guides you through the intricacies of the top five education savings accounts available today, providing a comprehensive comparison to help you make an informed decision. Whether you’re a new parent planning for the long term or a guardian seeking the most efficient way to grow your savings, this guide is designed to equip you with the knowledge you need to confidently navigate the world of education savings.

Understanding the Basics of Education Savings Accounts

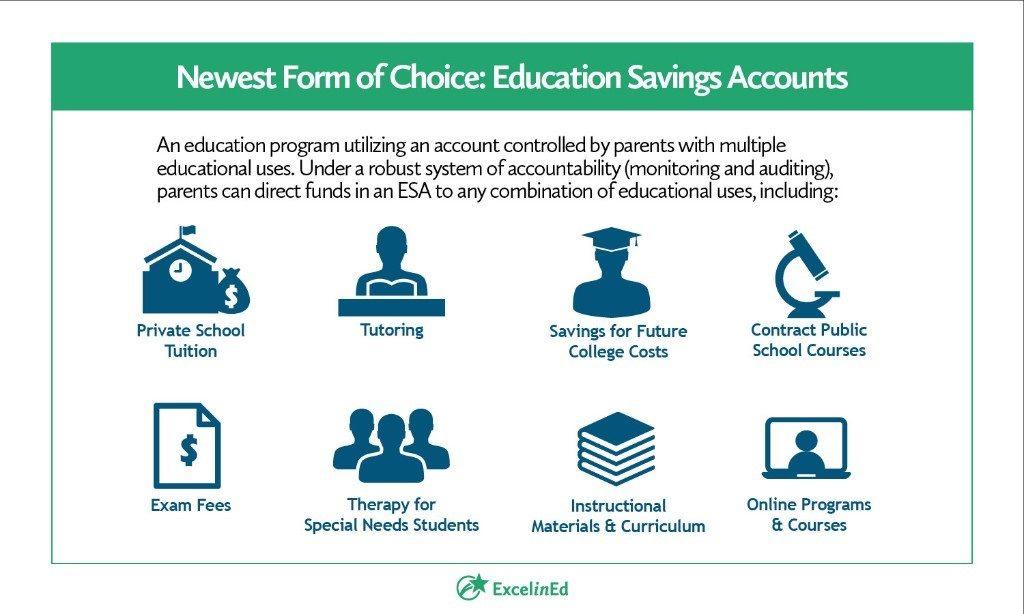

Education Savings Accounts (ESAs) are specialized savings tools designed to help families plan and save for educational expenses. These accounts offer tax advantages, allowing your investments to grow tax-free when used for qualified educational costs. Understanding the key features of different ESAs can empower you to make informed decisions about your educational financial planning.

- Tax Benefits: Most ESAs offer tax-free growth on your savings, which can significantly increase your investment over time. Withdrawals for qualified educational expenses are also tax-free.

- Contribution Limits: Each type of ESA has its own contribution limits. It’s essential to know these limits to maximize your savings potential while adhering to IRS regulations.

- Eligible Expenses: Be aware of what expenses are considered “qualified.” While some accounts cover only tuition, others may include books, supplies, and even room and board.

- Age Restrictions: Certain accounts impose age limits on when contributions can be made or when funds must be used, so understanding these restrictions can help you plan accordingly.

- Investment Options: Different ESAs offer varied investment choices. Some may allow you to choose from a range of mutual funds, while others might be more restrictive. Understanding these options can help you tailor your savings strategy to your risk tolerance and investment goals.

Comparative Analysis of Features and Benefits

When it comes to choosing the right education savings account, understanding the features and benefits of each option is crucial for making an informed decision. Here’s a breakdown of the top five education savings accounts to help you navigate your choices:

- 529 Plans: These plans are popular due to their tax advantages. Contributions grow tax-free, and withdrawals are tax-free when used for qualified education expenses. Many states also offer tax deductions or credits for contributions.

- Coverdell Education Savings Accounts (ESAs): Although contributions are limited to $2,000 per beneficiary per year, Coverdell ESAs offer greater investment flexibility compared to 529 plans. They can be used for K-12 expenses, in addition to higher education costs.

- UGMA/UTMA Accounts: While not exclusively for education, these custodial accounts allow assets to be used for any purpose that benefits the child. They offer flexibility but come with fewer tax advantages than 529 plans or Coverdell ESAs.

- Roth IRAs: Typically used for retirement, Roth IRAs can also be tapped for education expenses. Contributions can be withdrawn tax-free at any time, and earnings can be withdrawn tax-free and penalty-free for qualified education expenses after a five-year holding period.

- Traditional Savings Accounts: These accounts offer simplicity and liquidity, though they lack the tax advantages of other options. Interest earned is taxable, making them less appealing for long-term education savings.

By comparing these accounts, you can weigh the tax benefits, contribution limits, and flexibility each offers to determine which aligns best with your educational savings goals.

Expert Recommendations for Maximizing Your Savings

When it comes to selecting the right education savings account, tapping into expert insights can make all the difference in your financial planning. Financial advisors often suggest considering factors like contribution limits, tax benefits, and account flexibility. Here are some key recommendations to help you navigate your choices:

- Evaluate Tax Advantages: Look for accounts that offer tax-deferred growth or tax-free withdrawals for educational expenses. This can significantly enhance your savings over time.

- Assess Flexibility: Choose an account that allows for a wide range of educational expenses, not just tuition. Consider plans that cover books, supplies, and even room and board.

- Consider Contribution Limits: Be aware of annual contribution limits and ensure they align with your savings goals. Some accounts may offer higher limits, providing more room for growth.

- Review Investment Options: A diverse portfolio can be crucial. Look for accounts that offer a variety of investment options, from stocks to bonds, to suit your risk tolerance.

- Understand Penalties and Fees: Be mindful of potential penalties for non-educational withdrawals and any maintenance fees that could eat into your savings.

By focusing on these elements, you can make informed decisions that align with your financial goals and provide a solid foundation for educational funding.

Strategic Tips for Choosing the Right Account

When it comes to selecting an education savings account, strategic thinking is crucial to maximizing your investment and securing your child’s future. Start by evaluating your financial goals and timeline. Are you saving for college in the next few years, or do you have a longer horizon? Consider the following strategic tips to help you make an informed decision:

- Understand Tax Implications: Different accounts come with varied tax benefits. Some offer tax-free growth, while others allow tax-deductible contributions. Research these nuances to determine which option aligns best with your financial strategy.

- Assess Contribution Limits: Be aware of how much you can contribute annually to each type of account. Higher limits can provide more room for growth, but also ensure you’re comfortable meeting these thresholds.

- Evaluate Investment Options: Some accounts offer a wide range of investment choices, while others may be more limited. Select an account that offers the investment flexibility you need to achieve your savings objectives.

- Review Withdrawal Rules: Understand the conditions under which you can withdraw funds. Some accounts penalize non-qualified withdrawals, which could impact your savings if plans change.

By carefully considering these factors, you can strategically choose an education savings account that aligns with your financial goals and sets your child on the path to success.

{kind=link}