In today’s financial landscape, balancing the aspiration of funding a college education with other significant life goals can seem daunting. However, with strategic planning and informed decision-making, it is entirely possible to save for college without compromising on other important objectives, such as retirement savings, buying a home, or traveling the world. This guide will walk you through practical steps and innovative strategies to harmonize your financial priorities, ensuring that you can confidently support educational pursuits while maintaining a well-rounded financial plan. Whether you’re a parent planning for your child’s future or an individual aiming to further your own education, this article will equip you with the tools to navigate the complexities of saving for college without sacrificing your broader life ambitions.

Create a Realistic Budget to Balance College Savings and Daily Expenses

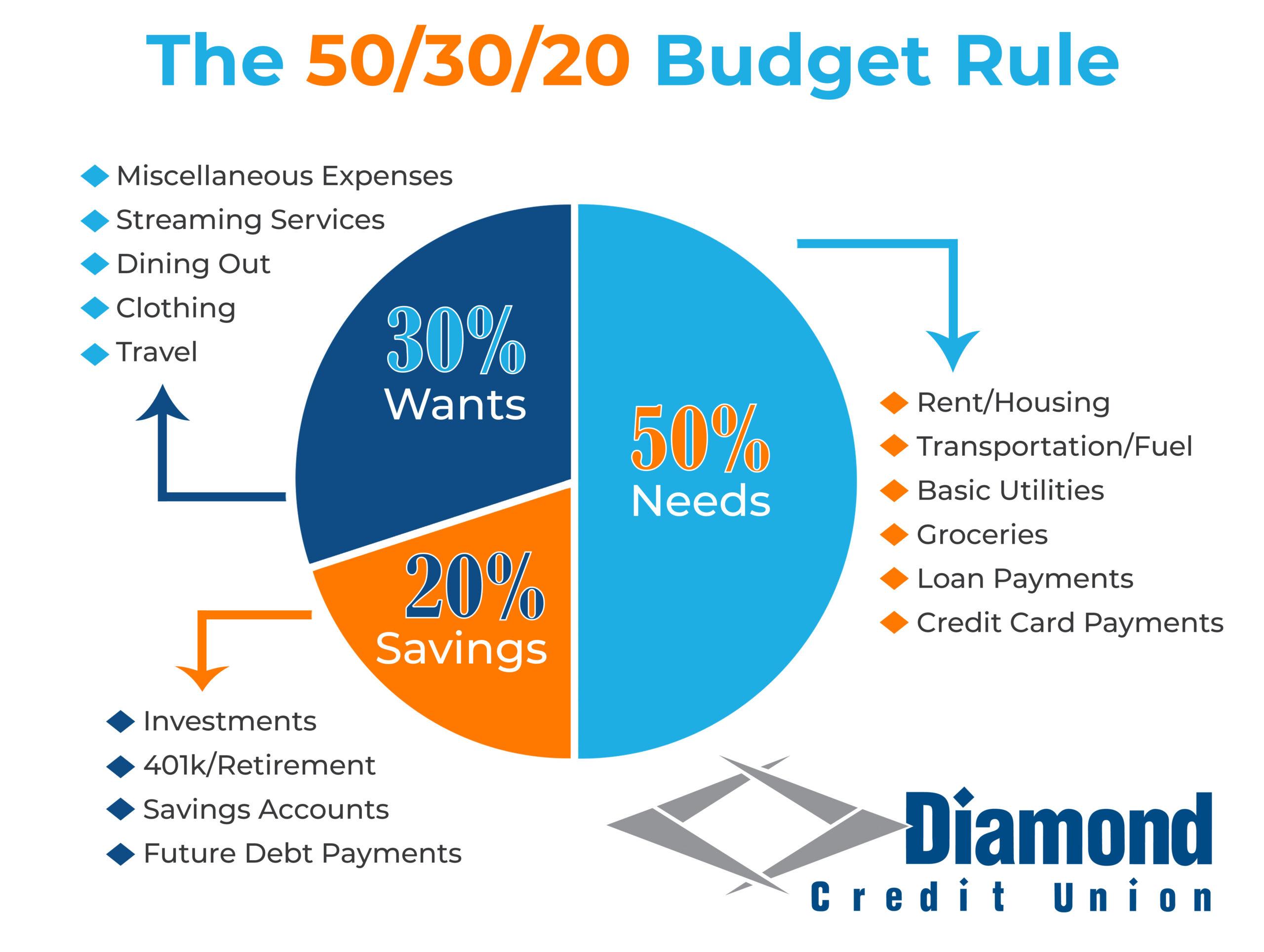

Crafting a budget that accommodates both college savings and daily expenses is an essential strategy for achieving financial balance. Start by analyzing your monthly income and expenditures to understand where your money is currently going. Identify areas where you can cut back, such as dining out or subscription services, and redirect those funds towards your college savings. It’s important to set realistic goals; consider allocating a fixed percentage of your income to your savings, ensuring it doesn’t compromise your daily necessities.

- Track Your Spending: Use apps or spreadsheets to monitor your expenses, helping you identify unnecessary costs.

- Prioritize Needs Over Wants: Focus on essential expenses and find cost-effective alternatives for non-essential items.

- Set Specific Savings Goals: Determine how much you need for college and break it down into monthly savings targets.

- Review and Adjust: Regularly review your budget to make necessary adjustments as your financial situation evolves.

By employing these strategies, you can create a budget that supports your educational aspirations while maintaining a healthy financial lifestyle. Remember, the key is consistency and the willingness to adapt as needed.

Maximize Savings with Tax-Advantaged Accounts and Scholarships

Investing in your child’s future doesn’t mean you have to compromise on your current financial goals. By strategically utilizing tax-advantaged accounts and scholarships, you can effectively save for college while maintaining a balanced financial plan. 529 Plans are a popular choice, offering tax-free growth and withdrawals when used for qualified education expenses. These plans also provide flexibility, allowing you to change beneficiaries or use the funds for various educational needs.

In addition to tax-advantaged accounts, scholarships can significantly reduce the financial burden of college. Encourage your child to actively seek scholarships by exploring options through school counselors, online databases, and community organizations. Here are a few tips to enhance their scholarship search:

- Start early to increase the number of opportunities available.

- Tailor applications to highlight unique strengths and achievements.

- Apply to a mix of local, regional, and national scholarships for broader coverage.

By taking advantage of these resources, you can save for college without derailing other financial aspirations.

Implement Smart Investment Strategies for Long-Term Growth

Embracing a diversified approach to investing can be a game-changer for securing funds for college without compromising your other financial aspirations. Begin by assessing your risk tolerance and investment horizon. Consider a blend of investments that include stocks, bonds, and mutual funds to balance potential risks and rewards. The power of compound interest over time can significantly amplify your savings, so start early and contribute regularly to harness this advantage.

- Explore tax-advantaged accounts such as 529 plans, which offer tax-free growth and withdrawals for qualified education expenses.

- Utilize automation to maintain consistent contributions to your investment accounts, ensuring that your savings strategy remains on track.

- Rebalance your portfolio periodically to adjust to market changes and align with your evolving financial goals.

By implementing these smart investment strategies, you can efficiently save for college while continuing to pursue other life goals with confidence.

Prioritize Financial Goals and Monitor Progress Regularly

Embarking on the journey to save for college while juggling other financial aspirations requires strategic prioritization and consistent monitoring. Begin by clearly defining your short-term and long-term financial objectives. Categorize your goals into essentials, like emergency funds and retirement savings, and aspirational targets, such as college funds and vacations. This clarity will help you allocate resources effectively, ensuring that urgent needs are met without sidelining future plans.

- Assess your current financial standing: Regularly review your income, expenses, and savings to understand your financial health.

- Set realistic timelines: Assign achievable deadlines to each goal, considering your financial capacity and any potential changes in income.

- Utilize budgeting tools: Leverage apps or spreadsheets to track progress, making it easier to adjust strategies as needed.

- Schedule regular check-ins: Monthly or quarterly reviews can help you stay on track and make necessary adjustments.

By keeping a close eye on your financial progress, you can confidently navigate the complexities of saving for college while ensuring that other significant milestones are not compromised.

{kind=link}