Setting achievable financial goals for your family is a fundamental step toward ensuring long-term stability and prosperity. Whether you’re aiming to save for your child’s education, plan a dream vacation, or build a comfortable retirement fund, the key lies in establishing clear, realistic objectives. This guide will empower you with practical strategies to align your family’s financial aspirations with actionable plans. By breaking down the process into manageable steps, you can transform your financial dreams into attainable realities, fostering a sense of security and confidence for your family’s future. Let’s embark on this journey together, as we explore the essential elements of effective financial goal-setting tailored to your family’s unique needs and aspirations.

Identifying Your Familys Financial Priorities

Understanding what truly matters to your family financially is the cornerstone of setting achievable goals. Begin by having an open discussion with all family members involved in financial decisions. This ensures everyone’s needs and aspirations are heard and considered. List the top priorities and differentiate between what is essential and what can be considered a long-term goal. Here are some points to consider:

- Basic Needs: Housing, food, and healthcare should be at the forefront of your priorities.

- Emergency Fund: Building a safety net for unforeseen circumstances is crucial.

- Education: Allocate funds for children’s education or personal skill development.

- Debt Repayment: Prioritize paying off high-interest debts to improve financial health.

- Retirement Planning: Ensure a portion of your income is directed towards retirement savings.

Once these priorities are clear, align them with your family’s values and lifestyle. This alignment not only fosters harmony but also makes financial discipline a shared family goal. Remember, flexibility is key; as your family’s circumstances change, so too might your financial priorities.

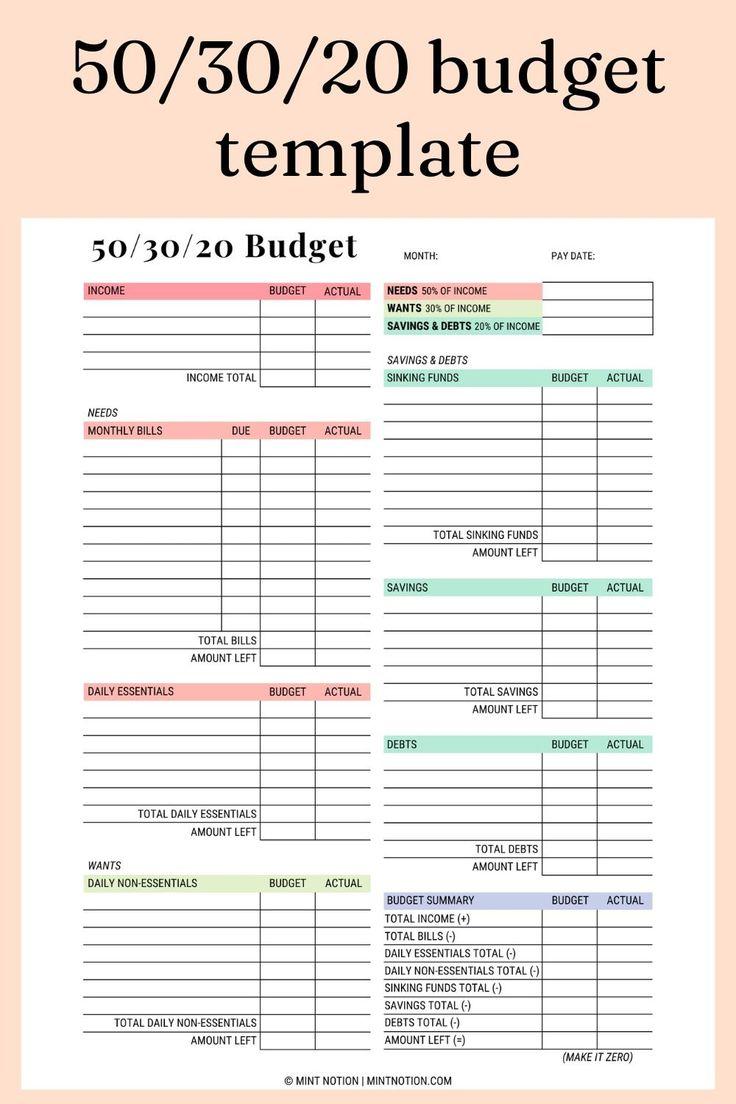

Creating a Realistic Budget to Support Your Goals

Crafting a budget that aligns with your family’s financial goals is essential for turning aspirations into reality. To start, identify your family’s short-term and long-term objectives, such as saving for a vacation, buying a home, or building an emergency fund. Once these goals are clear, categorize your expenses into fixed and variable costs. Fixed costs might include rent or mortgage payments, utilities, and insurance, while variable expenses could cover groceries, entertainment, and dining out. By understanding where your money goes, you can prioritize spending and cut unnecessary costs.

- Track Your Spending: Use budgeting apps or spreadsheets to monitor your daily expenditures and identify areas for improvement.

- Set Realistic Limits: Assign a specific amount to each category and stick to it, adjusting as necessary based on actual spending patterns.

- Review and Adjust: Regularly review your budget to ensure it still supports your goals, making adjustments for life changes like a new job or a growing family.

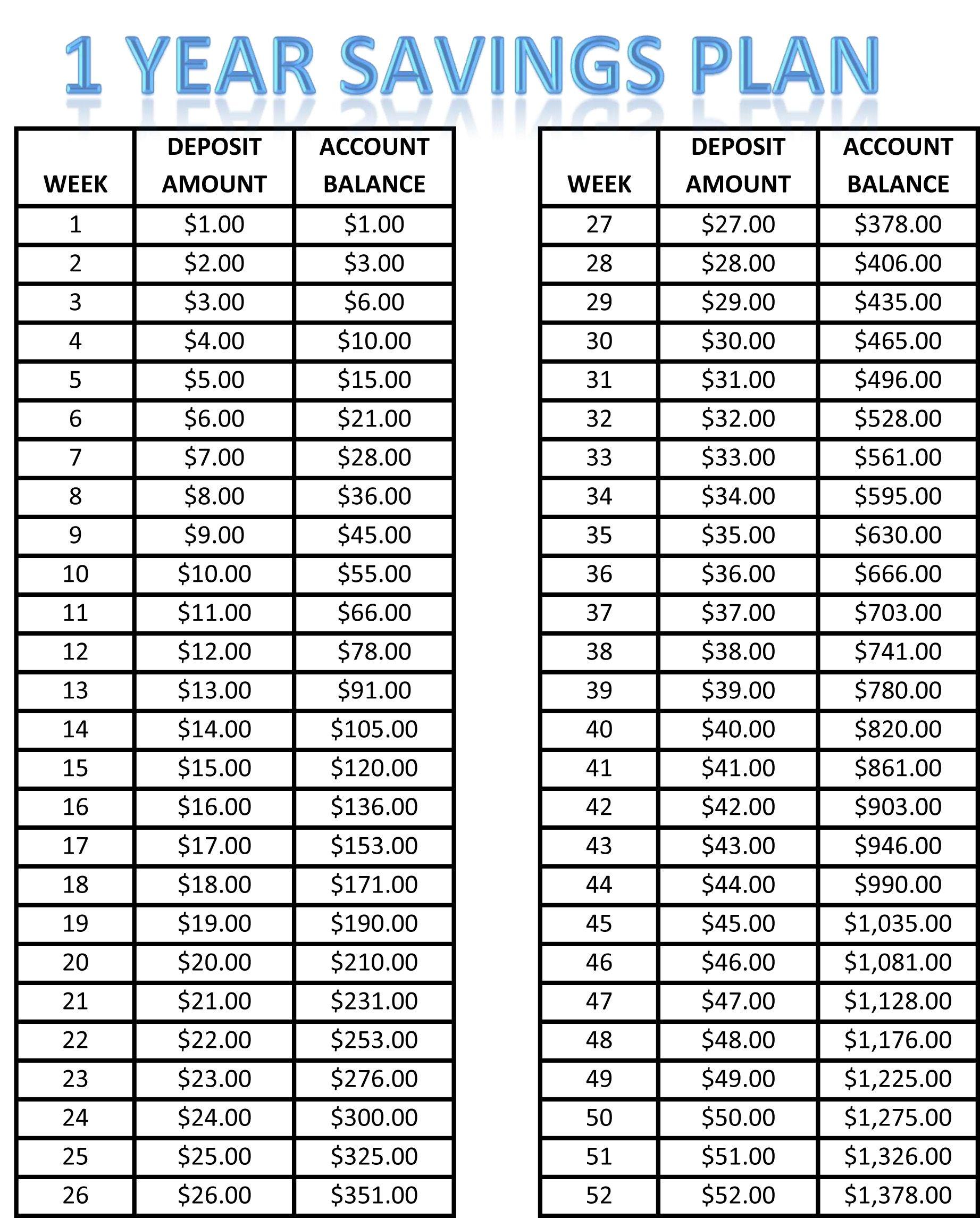

Establishing a Savings Plan for Long-Term Success

Crafting a robust savings strategy is essential for ensuring your family’s financial well-being. Start by identifying your long-term goals and breaking them down into manageable steps. Consider the following key elements to effectively design your plan:

- Determine Your Savings Goals: Clearly define what you’re saving for, whether it’s a comfortable retirement, your children’s education, or a dream vacation. Specific goals provide direction and motivation.

- Set Realistic Timelines: Establish achievable time frames for each goal. A realistic timeline helps prevent frustration and keeps your plan on track.

- Create a Budget: Analyze your current financial situation and allocate a portion of your income towards savings. Prioritize savings in your budget as a non-negotiable expense.

- Automate Your Savings: Use automatic transfers to ensure consistent contributions. This “set it and forget it” approach makes it easier to accumulate wealth over time.

- Monitor and Adjust: Regularly review your savings progress and adjust as needed. Life changes and unexpected expenses may require modifications to your plan.

By incorporating these elements into your financial strategy, you establish a solid foundation for achieving long-term success. Remember, the key is consistency and adaptability as you navigate your family’s financial journey.

Tracking Progress and Adjusting Your Financial Strategy

Once you have set your financial goals, it’s crucial to monitor your progress regularly to ensure you’re on the right path. This involves evaluating your financial strategy and making necessary adjustments. Start by establishing a consistent schedule to review your goals, whether it’s monthly or quarterly. Use this time to analyze your income, expenses, and savings to identify areas that need improvement. Keep a detailed record of your financial activities to easily spot trends or unexpected changes that might impact your goals.

- Assess your budget: Revisit your budget periodically and adjust it to accommodate any changes in your family’s needs or financial situation.

- Review your investments: Check if your investments are performing as expected and consider reallocating assets if necessary.

- Evaluate your debt management plan: Ensure that you are on track to pay off debts as planned, and adjust your repayment strategy if required.

- Update your goals: As life changes, so might your financial priorities. Be open to revising your goals to reflect new aspirations or circumstances.

By actively tracking your progress and being willing to adapt your financial strategy, you increase the likelihood of achieving your family’s financial aspirations. Remember, flexibility and responsiveness are key components of a successful financial journey.

{kind=link}