In today’s fast-paced world, achieving financial stability and success is more crucial than ever. Whether you’re aiming to pay off debt, save for a dream vacation, or build a robust retirement fund, setting clear financial goals is the cornerstone of a secure financial future. Yet, the path to financial success can often feel overwhelming, with countless options and potential pitfalls along the way. This article is your guide to demystifying the process, offering you a confident approach to setting financial goals that not only align with your aspirations but also keep you firmly on track. By implementing strategic steps and maintaining a focused mindset, you can transform your financial dreams into achievable realities, paving the way for a prosperous future.

Identifying Your Financial Priorities for Success

To navigate the complex landscape of personal finance, it’s crucial to first pinpoint what truly matters to you. Begin by reflecting on your values and envisioning your ideal life. Are you aiming for a debt-free existence, planning for a comfortable retirement, or saving for your children’s education? Once your core values are clear, prioritize them. This will guide your financial decisions and ensure that your money is being directed towards what you truly value.

- Short-term needs: These include building an emergency fund or paying off high-interest debt.

- Medium-term goals: Such as saving for a down payment on a house or planning a dream vacation.

- Long-term aspirations: These might involve investing for retirement or starting your own business.

Aligning your spending with your priorities ensures that every dollar spent is a step towards achieving your personal vision of success. By categorizing and focusing on what matters most, you create a clear roadmap that not only keeps you on track but also empowers you to make informed financial choices.

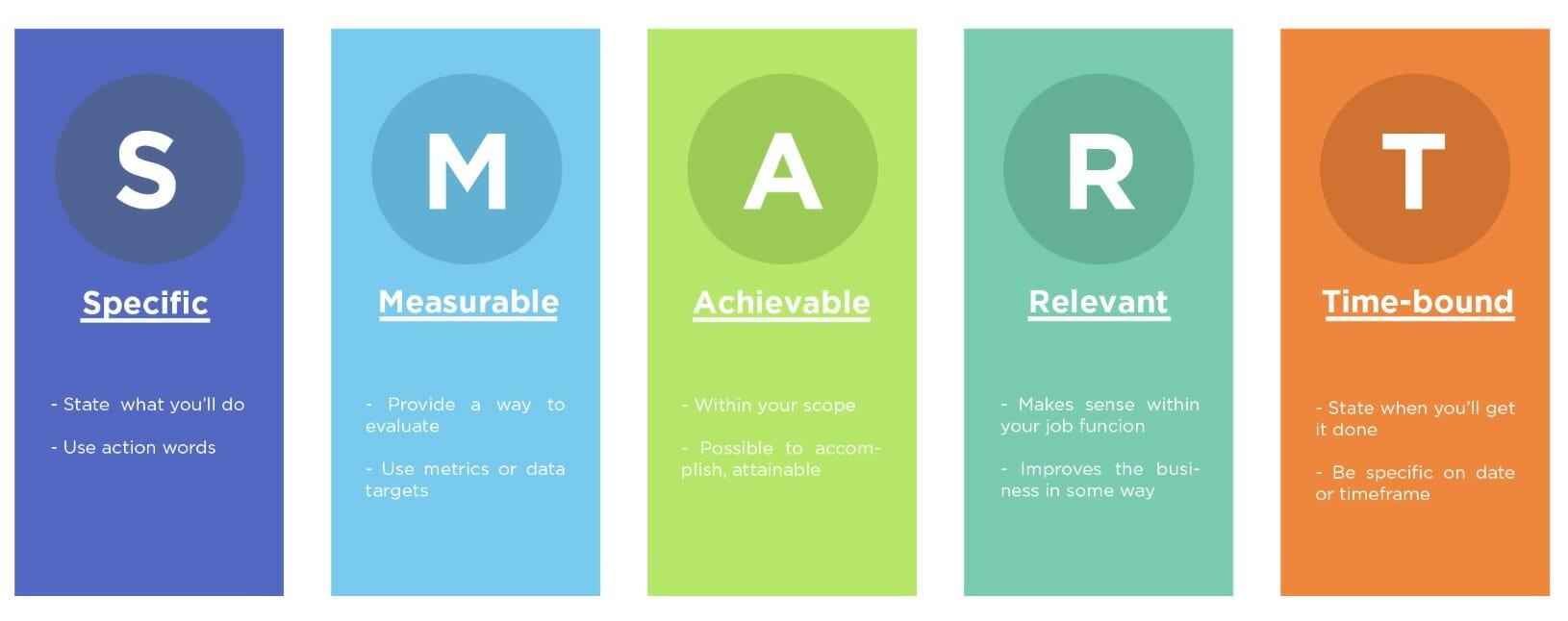

Crafting SMART Financial Goals for Achievable Milestones

When it comes to setting financial goals, applying the SMART criteria—Specific, Measurable, Achievable, Relevant, and Time-bound—is crucial for success. First, make your goals specific by defining exactly what you want to achieve. For example, instead of saying “save money,” opt for “save $5,000 for a vacation.” This clarity gives your goal a tangible target.

Next, ensure your goals are measurable. This means tracking your progress with milestones, such as saving $1,000 every three months. Your goal should also be achievable, challenging yet within reach based on your current financial situation. Align your goals with your life priorities to ensure they are relevant. Lastly, make them time-bound by setting a clear deadline, which creates a sense of urgency and helps maintain focus.

- Specific: Define clear and detailed objectives.

- Measurable: Use metrics to track progress.

- Achievable: Set realistic yet challenging targets.

- Relevant: Align with personal values and priorities.

- Time-bound: Establish deadlines to foster accountability.

Developing a Realistic Budget to Support Your Objectives

Crafting a realistic budget is a pivotal step in aligning your financial landscape with your personal goals. To begin, you should first evaluate your current financial situation, including income, expenses, and any outstanding debts. This assessment will lay the groundwork for a more structured financial plan. Consider the following strategies to create a budget that supports your ambitions:

- Identify Non-Negotiable Expenses: Start by listing essential costs such as rent, utilities, groceries, and transportation. Understanding these fixed expenses will help you determine how much discretionary income you have available.

- Allocate Funds to Savings and Investments: Prioritize setting aside a portion of your income towards savings or investments. This could be for an emergency fund, retirement, or other long-term goals. Consistent contributions, no matter how small, can significantly impact your financial stability over time.

- Track and Adjust: Regularly monitor your spending to ensure you remain within your budget. Use tools like budgeting apps or spreadsheets to track your expenses. If you find you’re overspending in certain areas, adjust your budget accordingly to stay on track.

By following these guidelines, you’ll create a budget that not only supports your immediate needs but also propels you towards your financial objectives with confidence and clarity.

Utilizing Tools and Strategies to Monitor Your Progress

Tracking your financial progress is crucial to ensuring you stay aligned with your goals. Begin by employing financial tracking apps that offer real-time insights into your spending and saving habits. These tools often provide customizable alerts and reports, helping you quickly identify areas where you might be overspending or under-saving.

Additionally, consider maintaining a personal finance journal. This method allows for a more reflective approach, enabling you to jot down not just numbers, but also thoughts and feelings about your financial journey. Some effective strategies include:

- Setting up monthly reviews to assess your progress against your financial goals.

- Using visual aids like graphs and charts to see trends over time.

- Incorporating automated savings plans to ensure consistent contributions toward your objectives.

By combining these tools and strategies, you create a robust framework that not only monitors your financial journey but also empowers you to make informed decisions moving forward.

{kind=link}