In an era marked by economic uncertainty and rapidly evolving financial landscapes, families are increasingly prioritizing long-term growth strategies to secure their financial future. The quest for robust investment plans is not just about accumulating wealth; it’s about building a legacy, ensuring financial security, and providing for future generations. This analytical exploration delves into the best investment strategies tailored for families, focusing on sustainable growth over the long haul. By examining a variety of asset classes, risk management techniques, and market trends, we aim to equip families with the knowledge and tools necessary to navigate the complexities of the investment world confidently. Whether you’re a seasoned investor or new to the realm of finance, understanding these strategies is crucial for making informed decisions that align with your family’s goals and values. Join us as we dissect the intricacies of long-term investment planning, providing insights that can help transform financial aspirations into tangible realities.

Identifying Growth-Oriented Investment Vehicles for Family Portfolios

When seeking growth-oriented investment vehicles for family portfolios, it’s essential to focus on options that balance potential returns with risk management. Equities are often at the forefront, offering robust long-term growth opportunities. Consider diversifying across sectors like technology, healthcare, and renewable energy, which are poised for substantial growth. Exchange-Traded Funds (ETFs) can also be a strategic choice, providing exposure to a broad range of stocks while mitigating individual stock risks.

Real estate investment trusts (REITs) are another compelling option, offering a combination of growth and income. They provide exposure to the real estate market without the need to manage physical properties, often resulting in consistent dividends. Additionally, Index Funds can serve as a cornerstone of a family’s investment strategy, delivering market-average returns with lower fees and less volatility. Consider these options to ensure a diversified, growth-focused family portfolio:

- Equities in emerging markets for higher potential returns

- ETFs with a focus on innovative sectors

- REITs for income and growth

- Index Funds for stability and steady growth

Balancing Risk and Reward in Long-Term Family Investment Strategies

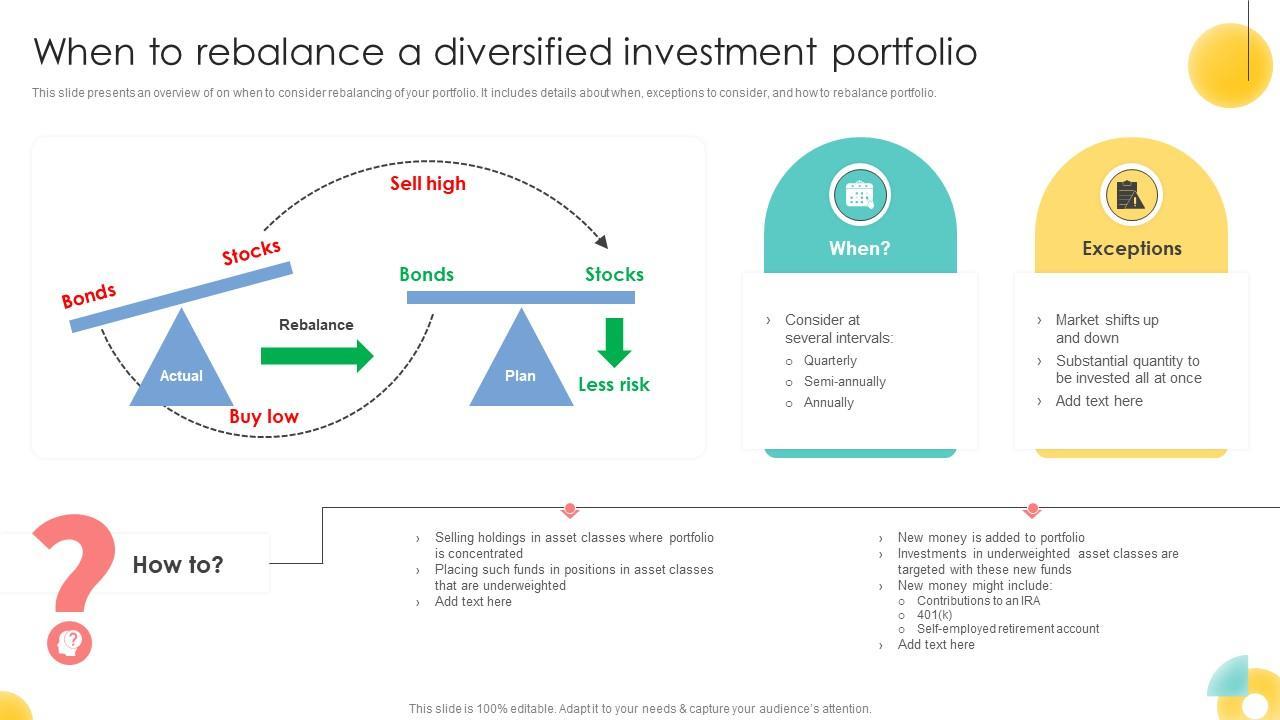

When designing investment strategies that prioritize long-term growth for families, it’s crucial to strike the right balance between risk and reward. A well-diversified portfolio can help manage volatility while still aiming for substantial growth. Here are some key considerations:

- Asset Allocation: Diversifying across asset classes such as stocks, bonds, and real estate can mitigate risks while providing opportunities for growth. Younger families might allocate more towards equities for higher growth potential, while gradually shifting to bonds as they approach their financial goals.

- Investment Horizon: Families should assess their financial goals and timelines. Long-term objectives like funding a child’s education or retirement savings allow for a higher risk tolerance, enabling investments in higher-yielding assets.

- Regular Rebalancing: Periodically reviewing and adjusting the portfolio ensures it remains aligned with the family’s risk tolerance and financial goals. This practice helps in capitalizing on market opportunities while protecting against downturns.

By carefully evaluating these factors, families can craft a robust investment strategy that aligns with their long-term aspirations, balancing the scales between potential risks and rewards with confidence.

Leveraging Tax-Advantaged Accounts for Maximum Family Wealth Growth

To secure a prosperous future for your family, it’s essential to make strategic use of tax-advantaged accounts. These accounts, such as 401(k)s, IRAs, and 529 college savings plans, offer significant benefits that can enhance your long-term wealth-building efforts. Maximize contributions to these accounts to take full advantage of tax deferrals and, in some cases, tax-free growth. With a focus on compounding returns, even modest contributions can grow substantially over time, making them a cornerstone of a robust financial plan.

Consider the following strategies to optimize your family’s financial growth:

- Utilize employer matching: If your employer offers a match on 401(k) contributions, ensure you’re contributing enough to receive the full match. This is essentially free money that can significantly boost your retirement savings.

- Diversify investments: Within your tax-advantaged accounts, maintain a diversified portfolio that aligns with your risk tolerance and investment horizon. This helps mitigate risks while capitalizing on growth opportunities.

- Prioritize Roth IRAs for young earners: Encourage younger family members to open Roth IRAs. Contributions are made with after-tax dollars, but withdrawals in retirement are tax-free, offering a valuable tax hedge.

Implementing these strategies ensures that your family’s wealth grows efficiently, leveraging the full potential of tax advantages for a secure financial future.

Crafting a Diversified Investment Plan for Multi-Generational Success

To cultivate a thriving investment strategy that serves multiple generations, it’s essential to blend diverse asset classes and financial instruments. Equities, for instance, offer the potential for high returns and should be a staple in any long-term plan. Consider allocating a portion of your portfolio to blue-chip stocks, which provide stability, and growth stocks that promise substantial appreciation. Real estate is another pillar, offering both rental income and capital growth. Incorporate REITs (Real Estate Investment Trusts) to diversify property investments without the need for direct ownership.

Beyond traditional investments, look towards alternative assets to hedge against market volatility. These might include commodities, such as gold and silver, or private equity and venture capital for those willing to take on higher risk for potentially higher returns. Bonds remain crucial for income generation and risk mitigation, with municipal bonds being particularly attractive for their tax benefits. Families can also explore international markets to tap into emerging economies, ensuring a truly global portfolio. By carefully balancing these elements, families can build a resilient investment plan that stands the test of time.

{kind=link}