In an era where financial security often feels elusive, building wealth for your family without succumbing to high-risk ventures is not only a prudent strategy but a necessary one. As economic landscapes fluctuate and market volatility becomes a constant companion, many families are seeking pathways to financial prosperity that prioritize stability and long-term growth over quick, high-stakes gains. This article delves into the analytical frameworks and strategic approaches that can guide families in accumulating wealth responsibly. By exploring diversified investment portfolios, sustainable savings plans, and prudent financial management techniques, we aim to equip you with the tools necessary to secure your family’s financial future confidently and intelligently. Whether you are just beginning your wealth-building journey or looking to refine your existing strategies, this guide offers insights grounded in sound financial principles and a deep understanding of market dynamics. Low-Risk Investment Vehicles for Family Wealth”>

Low-Risk Investment Vehicles for Family Wealth”>

Understanding Low-Risk Investment Vehicles for Family Wealth

For families looking to secure their financial future without the volatility of high-risk ventures, low-risk investment vehicles offer a reliable path. These options are designed to provide steady growth and protect your principal investment. Bonds, particularly government and high-grade corporate bonds, are a popular choice, as they provide fixed interest returns over a specified period. Certificates of Deposit (CDs) also offer a low-risk alternative, where your money is locked in for a set term with guaranteed interest earnings.

Another approach is to consider mutual funds that focus on conservative assets like dividend-paying stocks and money market funds. These funds are managed by professionals and diversify your investments to minimize risk. Additionally, index funds that track the performance of major market indices offer diversification and lower fees. Investing in real estate investment trusts (REITs) can also provide a stable income stream with less volatility than direct real estate investments. By choosing a mix of these low-risk vehicles, families can build a robust portfolio that emphasizes safety while still achieving growth.

Strategic Savings Plans to Secure Your Familys Financial Future

Building wealth for your family while minimizing risk is a careful balancing act, but with strategic savings plans, you can ensure financial stability without unnecessary exposure. One effective approach is to diversify your savings portfolio. Consider allocating funds into a mix of low-risk investment vehicles such as government bonds, high-yield savings accounts, and Certificates of Deposit (CDs). These options provide a safety net with predictable returns and lower volatility compared to stock market investments.

- Government Bonds: These are often seen as one of the safest investment options, offering steady interest over a fixed period.

- High-Yield Savings Accounts: These accounts provide higher interest rates than traditional savings accounts, allowing your money to grow securely.

- Certificates of Deposit (CDs): Lock in your funds for a specified term with a guaranteed return, making it an excellent option for long-term savings.

Another critical component of a strategic savings plan is automated savings. Set up automatic transfers from your checking account to your savings or investment accounts. This “set it and forget it” method ensures consistent contributions to your family’s financial future without the temptation to spend the money elsewhere. By leveraging these strategies, you can build a robust financial foundation that supports your family’s needs and ambitions without the stress of high-risk ventures.

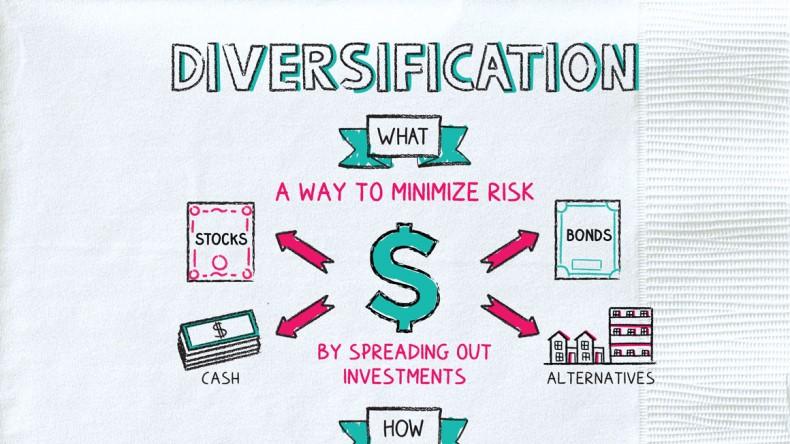

The Role of Diversification in Minimizing Financial Risks

In the quest to build family wealth with minimal risk, one of the most effective strategies is spreading investments across a variety of asset classes. Diversification acts as a protective shield, reducing the impact of volatility in any single investment. By allocating resources into different areas such as stocks, bonds, real estate, and perhaps even international markets, investors can mitigate potential losses. This strategy works on the principle that not all asset classes will respond to market forces in the same way at the same time.

- Stocks: Offer growth potential but come with higher volatility.

- Bonds: Generally provide stable returns and act as a buffer against stock market swings.

- Real Estate: Can offer steady income and appreciation, often moving independently of stock markets.

- International Investments: Provide exposure to global growth and can offset domestic downturns.

By incorporating a mix of these investments, families can protect their portfolios from drastic losses while still pursuing growth opportunities. It’s a strategic approach that balances risk and reward, ensuring that wealth is built steadily over time without exposing the family to unnecessary financial dangers.

Leveraging Tax-Advantaged Accounts for Long-Term Wealth Growth

When it comes to building long-term wealth, tax-advantaged accounts serve as a strategic tool that can significantly boost your family’s financial security. By utilizing these accounts, you can take advantage of tax breaks and compound interest, allowing your investments to grow more efficiently over time. Retirement accounts like 401(k)s and IRAs are popular choices, offering tax-deferred growth or tax-free withdrawals in retirement, depending on the type. For those looking to save for education expenses, a 529 plan provides tax-free growth and withdrawals when funds are used for qualified educational purposes. These options not only reduce your taxable income today but also pave the way for substantial savings in the future.

Key benefits of tax-advantaged accounts include:

- Tax Deferral: Contributions are often made pre-tax, reducing your taxable income.

- Compound Growth: Earnings on investments grow tax-free or tax-deferred, enhancing growth potential.

- Flexibility: Various accounts cater to different life goals, such as retirement, education, or healthcare.

- Employer Contributions: Many employers offer matching contributions to 401(k) plans, adding free money to your savings.

{kind=link}