In today’s rapidly evolving financial landscape, families embarking on their investment journey face a unique set of challenges and opportunities. With the complexities of global markets, economic fluctuations, and a plethora of investment vehicles to choose from, crafting a robust investment strategy is more crucial than ever. This article delves into the best investment strategies tailored specifically for families who are just starting out, providing a comprehensive analysis of the foundational principles and practical approaches that can pave the way for financial security and growth. By examining diverse investment options, assessing risk tolerance, and understanding long-term goals, we aim to equip families with the confidence and knowledge needed to make informed decisions that will secure their financial future.

Understanding Risk and Reward in Family Investments

Venturing into the world of family investments can be an exhilarating journey, but it requires a solid understanding of the delicate balance between risk and reward. Risk, in the context of investments, refers to the potential for loss or lower-than-expected returns. On the other hand, reward is the potential gain or profit from the investment. It’s crucial for families to recognize that higher potential rewards typically come with higher risks. By understanding this dynamic, families can make informed decisions that align with their financial goals and risk tolerance.

To effectively manage this balance, families should consider diversifying their investment portfolio. This means spreading investments across various asset classes, such as:

- Stocks: Generally offer higher potential returns but come with greater volatility.

- Bonds: Provide more stability and regular income, though with lower returns.

- Real Estate: Offers tangible asset value and potential for rental income.

- Mutual Funds: Allow for diversification within a single investment, managed by professionals.

Families just starting out should evaluate their risk appetite and financial objectives, ensuring their investment strategy is both realistic and adaptable to life’s changes.

Building a Diversified Portfolio for Long-term Growth

Creating a mix of investments that spans across various asset classes is crucial for families looking to secure financial stability and growth over the long term. Diversification is not just a buzzword; it’s a strategy that mitigates risk and enhances potential returns. By spreading investments across different sectors, geographies, and asset types, families can protect themselves against market volatility. Here’s how to get started:

- Stocks and Bonds: A balanced combination of equities for growth and bonds for stability can provide a solid foundation. Consider a mix of domestic and international stocks to capture global growth opportunities.

- Real Estate: Investing in real estate, whether through direct property purchases or REITs (Real Estate Investment Trusts), can offer both income and capital appreciation over time.

- Index Funds and ETFs: These are cost-effective ways to gain exposure to a wide range of markets, ensuring your portfolio isn’t overly dependent on any single investment.

- Emerging Markets: Including a portion of emerging market investments can tap into the rapid growth potential of developing economies.

By carefully selecting a variety of investment vehicles, families can build a portfolio that is resilient in the face of economic fluctuations and poised for sustained growth.

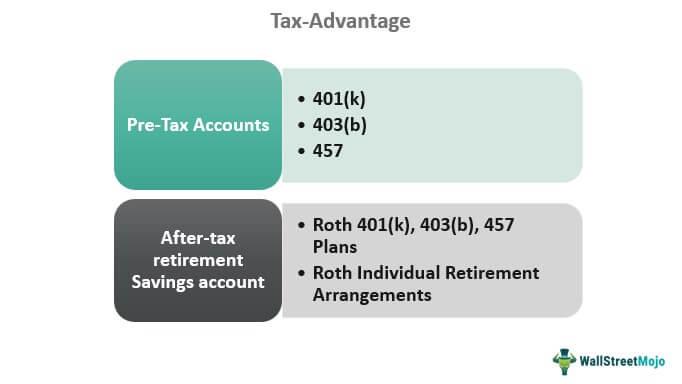

Maximizing Tax-advantaged Accounts for Future Security

For families beginning their financial journey, strategically utilizing tax-advantaged accounts can be a cornerstone of building long-term financial security. These accounts offer significant tax benefits that can maximize growth potential and minimize tax liabilities. Here are key accounts to consider:

- 401(k) Plans: Often provided by employers, these plans allow families to contribute pre-tax income, reducing taxable income and benefiting from potential employer matches.

- IRAs (Individual Retirement Accounts): Both Traditional and Roth IRAs provide unique tax advantages. Traditional IRAs offer tax-deferred growth, while Roth IRAs allow for tax-free withdrawals in retirement.

- 529 College Savings Plans: Designed for education expenses, these plans offer tax-free growth and withdrawals when funds are used for qualified education costs, making them ideal for families planning for their children’s future education.

By prioritizing these accounts, families can effectively build a robust financial foundation while leveraging tax benefits. Consistent contributions, even in small amounts, can accumulate significantly over time, providing both security and flexibility for future financial needs.

Balancing Short-term Needs with Long-term Financial Goals

When embarking on the journey of financial planning, it is crucial for families to effectively juggle immediate needs with aspirations for the future. Short-term needs, such as emergency funds and everyday expenses, often compete for attention with long-term financial goals like retirement savings and college funds. A practical approach involves creating a flexible budget that can accommodate both.

- Emergency Fund Prioritization: Allocate a portion of your monthly income to an emergency fund, ensuring your family is prepared for unexpected expenses without derailing long-term plans.

- Debt Management: Focus on reducing high-interest debt, which can free up more resources for future investments.

- Gradual Investment in Retirement Accounts: Start with small contributions to retirement accounts, such as a 401(k) or IRA, and gradually increase them as your financial situation improves.

By aligning your financial strategy with both immediate and future needs, you can ensure a balanced approach that fosters stability and growth. This method not only secures your family’s current lifestyle but also sets the stage for a prosperous future.

{kind=link}