In the ever-fluctuating world of financial markets, safeguarding your retirement savings against unexpected downturns is not just a prudent strategy—it’s an essential component of a secure financial future. While market volatility can pose significant risks, it also presents opportunities for those equipped with the right knowledge and tools. This article delves into the best practices for protecting your nest egg from the inevitable ebbs and flows of the market. From diversifying your investment portfolio to considering alternative assets, we’ll guide you through proven strategies that can help mitigate risk and ensure your retirement savings remain resilient. With a confident approach and a well-informed plan, you can navigate market uncertainties and keep your retirement goals on track.

Diversify Your Investment Portfolio for Maximum Stability

To shield your retirement savings from the inevitable ebbs and flows of the market, it’s crucial to adopt a strategic approach that involves spreading your investments across a variety of asset classes. This strategy, known as diversification, helps minimize risk and stabilize your portfolio over time. Consider these key elements:

- Stocks and Bonds: Balance is essential. While stocks offer growth potential, bonds provide stability and regular income. The right mix depends on your risk tolerance and retirement timeline.

- Real Estate: Investing in property or REITs can offer a steady income stream and hedge against inflation, adding a tangible asset to your portfolio.

- Commodities: Including assets like gold or oil can act as a safeguard against market volatility and currency fluctuations.

- International Exposure: Don’t limit your investments to one geographical area. Global diversification can reduce risk and tap into emerging markets with growth potential.

By thoughtfully allocating your investments across these diverse asset classes, you can build a robust portfolio designed to weather economic storms, ensuring your retirement savings remain secure and grow over time.

Embrace Safe Haven Assets to Mitigate Risks

In the quest to safeguard your retirement savings, allocating a portion of your portfolio to safe haven assets can be a prudent strategy. These assets are typically less volatile and can provide a buffer against market fluctuations. Here are some key options to consider:

- Gold: Often referred to as a “crisis commodity,” gold has historically maintained its value during economic downturns. Its intrinsic value and global demand make it a reliable choice for diversifying your portfolio.

- Government Bonds: U.S. Treasury bonds and other government securities are considered low-risk investments, offering stability and predictable returns. They are backed by the full faith and credit of the issuing government, making them a cornerstone of any risk-averse strategy.

- Cash Equivalents: Instruments such as money market funds or short-term certificates of deposit (CDs) provide liquidity and safety. These assets allow you to quickly reallocate funds without the fear of significant loss.

By incorporating these assets, you can create a balanced approach that not only preserves your capital but also positions you to take advantage of future market opportunities. Remember, the goal is not to eliminate risk entirely but to manage it effectively.

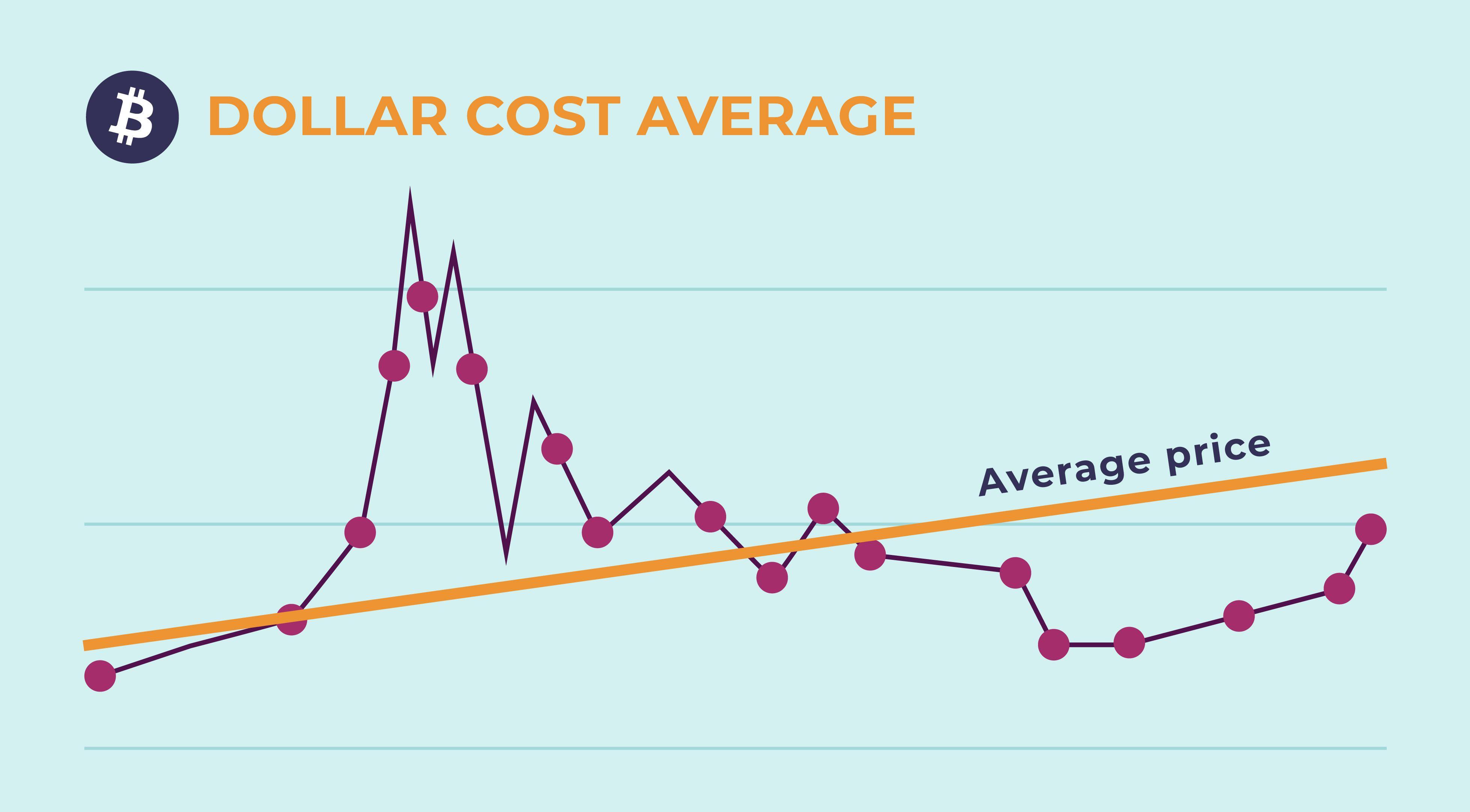

Utilize Dollar-Cost Averaging to Smooth Out Market Volatility

One proven strategy to navigate the turbulent waters of financial markets is the practice of dollar-cost averaging. By investing a fixed amount of money at regular intervals, regardless of market conditions, you effectively reduce the impact of market volatility on your portfolio. This method allows you to purchase more shares when prices are low and fewer when they are high, ultimately leading to a lower average cost per share over time. It’s a disciplined approach that removes the emotional component from investing, helping you to avoid the pitfalls of trying to time the market.

- Consistency: Establish a routine investment schedule, such as monthly or quarterly, to maintain steady contributions to your retirement savings.

- Diversification: Combine this approach with a diversified portfolio to further cushion against market fluctuations.

- Long-term Focus: Embrace a long-term perspective, understanding that short-term market dips are normal and can be opportunities rather than setbacks.

Implement Strategic Withdrawals to Preserve Long-Term Growth

In times of market volatility, maintaining a steady course can be challenging. However, implementing strategic withdrawals can be a savvy approach to safeguard your retirement savings. By carefully planning how and when to withdraw funds, you can mitigate the impact of a downturn and ensure your nest egg remains robust for the future. Here are some key strategies to consider:

- Prioritize Withdrawals from Stable Accounts: Focus on drawing from more stable, low-risk accounts during market slumps. This can help preserve the value of higher-risk investments until markets recover.

- Utilize a Cash Reserve: Having a dedicated cash reserve allows you to cover expenses without tapping into investments that might be underperforming. Aim to maintain a cash reserve that can support your living expenses for at least 1-2 years.

- Implement a Withdrawal Rate Strategy: Consider adopting a flexible withdrawal rate that adjusts with market conditions. This approach allows you to withdraw less during downturns and more when the market is strong, thereby protecting your portfolio’s longevity.

These strategies, when executed thoughtfully, not only help in navigating market fluctuations but also bolster the long-term growth of your retirement savings. By making informed decisions about withdrawals, you can maintain financial stability and peace of mind, even amidst economic uncertainty.

{kind=link}