As you approach retirement, ensuring a stable and reliable income stream becomes paramount to maintaining your desired lifestyle. Annuities, often overlooked in financial planning, can serve as a powerful tool to guarantee a steady income during your golden years. In this guide, we will demystify the world of annuities, breaking down their complexities into actionable insights. With our step-by-step approach, you’ll learn how to harness the potential of annuities to create a secure financial foundation for your retirement. Whether you’re new to the concept or seeking to optimize your existing retirement strategy, this article will equip you with the knowledge and confidence to make informed decisions about your financial future.

Understanding the Basics of Annuities for Retirement Income

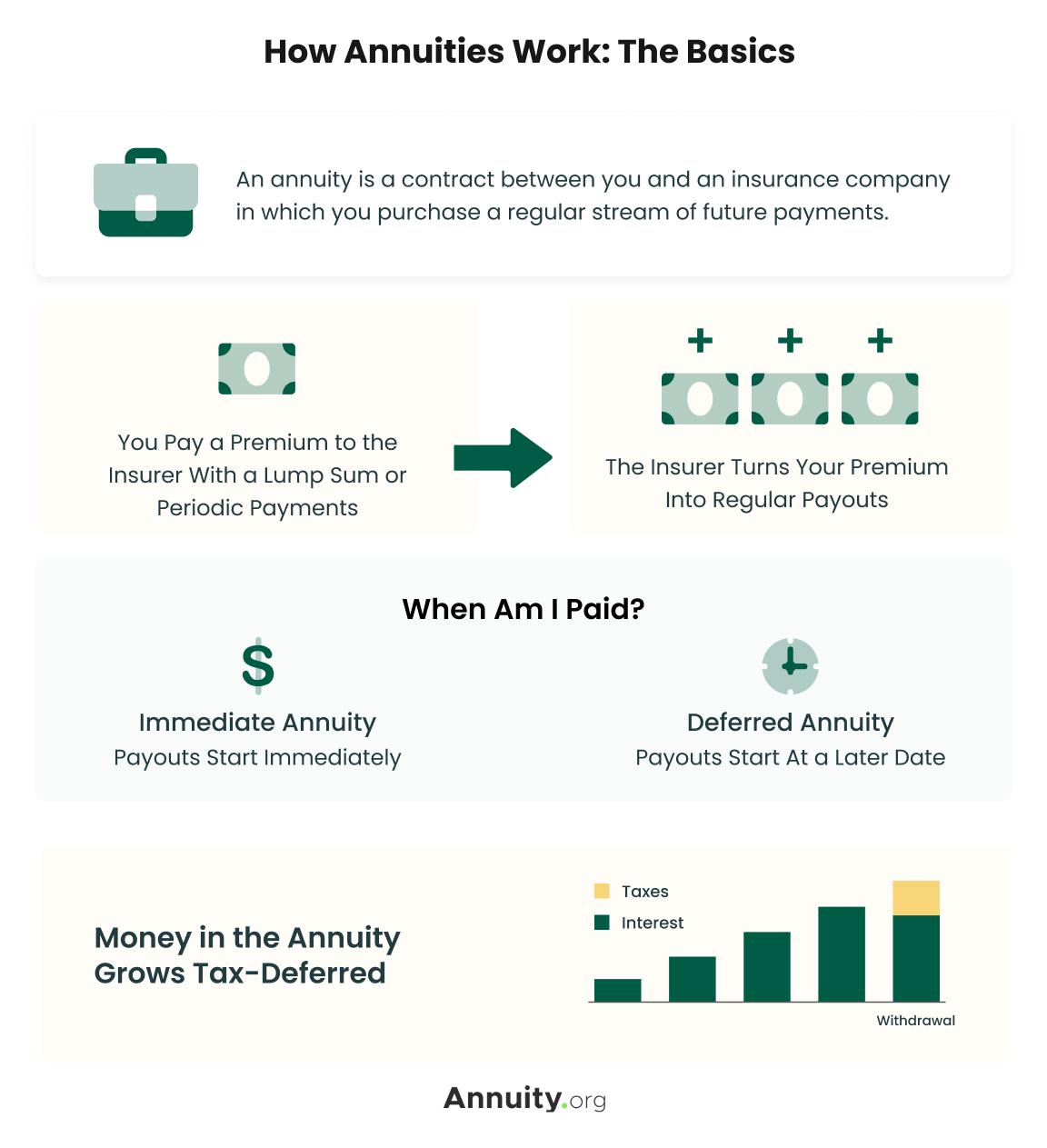

Annuities can be a powerful tool in securing a reliable income stream during retirement. At their core, annuities are contracts with an insurance company that promise a series of payments in exchange for an initial investment. There are several types of annuities to consider, each with unique features and benefits:

- Fixed Annuities: Offer a guaranteed payout at a fixed interest rate, providing predictability and stability.

- Variable Annuities: Allow you to invest in a selection of funds, with payments varying based on the performance of these investments.

- Indexed Annuities: Combine features of both fixed and variable annuities, linking returns to a specific market index while offering a minimum guaranteed payout.

Choosing the right annuity involves understanding your risk tolerance and income needs. Fixed annuities might be ideal for those seeking security and a steady income, while variable annuities could appeal to those willing to take on more risk for potentially higher returns. Indexed annuities offer a balanced approach, suitable for those looking for moderate growth with some security. Consulting with a financial advisor can help tailor an annuity strategy that aligns with your retirement goals.

Choosing the Right Type of Annuity to Meet Your Retirement Goals

When exploring annuities as a solution for guaranteed retirement income, it’s essential to understand the diverse options available and how they align with your financial goals. Fixed annuities provide a stable and predictable income stream, making them ideal for retirees seeking security against market fluctuations. They offer a fixed interest rate over a specified period, ensuring consistent payments. On the other hand, variable annuities allow you to invest in a range of sub-accounts, similar to mutual funds, which can potentially yield higher returns. However, they come with greater risk and require careful management.

For those who prefer a balance between security and growth, indexed annuities might be a suitable choice. These annuities link returns to a stock market index, offering the potential for higher earnings while safeguarding against significant losses with a minimum guaranteed return. Consider these factors when selecting an annuity:

- Risk Tolerance: Determine your comfort level with market volatility.

- Income Needs: Assess your required income to maintain your lifestyle.

- Inflation Protection: Ensure the annuity can adjust for inflation to preserve purchasing power.

- Liquidity: Evaluate the flexibility for accessing funds if needed.

By aligning your annuity choice with your retirement objectives, you can create a robust strategy that provides peace of mind and financial stability.

Maximizing Income with Strategic Annuity Investments

Strategic annuity investments can be a powerful tool for those looking to ensure a steady stream of income during retirement. By selecting the right type of annuity, retirees can enjoy the benefits of guaranteed income while minimizing risks associated with market volatility. Here are some key strategies to consider:

- Deferred Annuities: Allow your investment to grow tax-deferred until you start withdrawing. This can lead to a larger payout during retirement.

- Immediate Annuities: Convert a lump sum into an immediate income stream, perfect for those who are nearing or have just entered retirement.

- Variable Annuities: Provide potential for growth by linking payouts to the performance of an investment portfolio, offering higher income possibilities.

- Fixed Annuities: Ensure a predictable and steady income, unaffected by market changes, making it ideal for risk-averse investors.

By incorporating these strategies, retirees can effectively manage their income sources, ensuring they have a reliable financial foundation throughout their retirement years. Always consider consulting with a financial advisor to tailor annuity choices to your specific needs and goals.

Avoiding Common Pitfalls in Annuity Planning for a Secure Retirement

When integrating annuities into your retirement plan, it’s crucial to navigate some common pitfalls to ensure a smooth path to financial security. One of the most frequent mistakes is not fully understanding the different types of annuities available. Immediate annuities, deferred annuities, and variable annuities each come with their own set of benefits and risks. Failing to align your choice with your financial goals and risk tolerance can lead to unwanted surprises. For instance, opting for a variable annuity without considering market volatility might jeopardize your income stream. Take the time to educate yourself on these options or consult with a financial advisor who can guide you in making an informed decision.

Another common misstep is overlooking the impact of fees and charges, which can significantly erode your returns over time. Be vigilant about understanding the fee structure associated with your annuity. Common charges include:

- Surrender charges – fees for early withdrawal.

- Administrative fees – regular charges for managing the annuity.

- Mortality and expense risk charges – costs associated with the insurance component.

Ensure that you have a clear picture of these expenses and how they might affect your overall retirement income. By being proactive and thorough in your annuity planning, you can sidestep these pitfalls and secure a more reliable financial future.

{kind=link}