Getting a late start on saving for college can feel daunting, but rest assured, it’s never too late to take control of your financial future. Whether your child is in high school or you’re considering going back to school yourself, effective strategies can help you make the most of the time and resources you have. This guide will walk you through practical steps to build a robust college savings plan, even if you’re starting later than anticipated. From exploring financial aid options to maximizing your current savings, we’ll equip you with the knowledge and tools needed to make informed decisions, ensuring that higher education remains within reach. Let’s dive into how you can confidently navigate the path to funding a college education, no matter your starting point.

Maximize Savings with Accelerated Contribution Strategies

Accelerating your contributions is a powerful tactic to bridge the gap when starting late on saving for college. By leveraging certain strategies, you can boost your savings significantly in a shorter time frame. Here’s how:

- Utilize Catch-Up Contributions: If you’re over 50, many retirement accounts allow for higher contribution limits. While these are designed for retirement, freeing up other funds for college savings can be an effective workaround.

- Leverage Tax Refunds and Bonuses: Consider allocating any tax refunds or work bonuses directly into your college savings fund. This one-time boost can make a substantial difference over time.

- Automate Savings: Set up automatic transfers from your checking account to your college savings account. This ensures consistent contributions and helps you avoid the temptation to spend the money elsewhere.

By implementing these accelerated contribution strategies, you can maximize your savings potential and make up for lost time. Focus on consistency and creativity in your saving approach, and you’ll be well on your way to achieving your college funding goals.

Leverage Financial Aid and Scholarship Opportunities

One of the most effective strategies for saving on college costs is to explore the myriad of financial aid and scholarship opportunities available. Scholarships are not just for valedictorians or star athletes; they come in all shapes and sizes, catering to a diverse range of talents, backgrounds, and interests. Begin by researching local community organizations, businesses, and foundations that may offer scholarships to students in your area. Additionally, don’t overlook national databases and platforms dedicated to connecting students with scholarships, such as Fastweb and Scholarships.com. The key is to cast a wide net and apply to as many relevant opportunities as possible.

Financial aid is another crucial component of reducing college expenses. Start by filling out the Free Application for Federal Student Aid (FAFSA) to determine your eligibility for federal grants, work-study programs, and loans. Remember, many schools also use the FAFSA to award their own institutional aid, so completing it is a vital step. Furthermore, some states offer their own financial aid programs, which can significantly alleviate the financial burden of college. Be proactive and reach out to the financial aid offices of the colleges you’re interested in; they can provide guidance on additional opportunities and deadlines specific to their institution. By actively seeking out and leveraging these resources, you can substantially reduce your out-of-pocket costs for college.

Explore Flexible College Funding Options

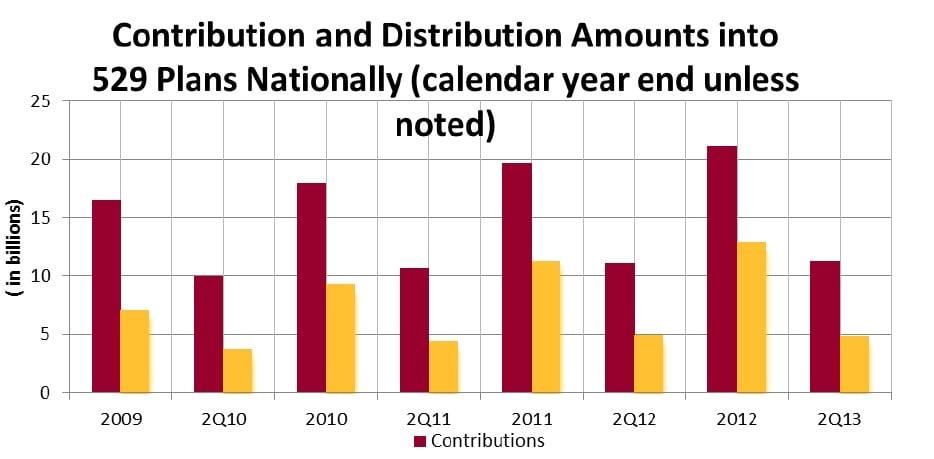

When it comes to funding college, embracing flexibility can be your greatest asset. Consider starting with 529 Plans, which offer tax advantages and can be set up quickly, allowing you to contribute at your own pace. If you’re worried about investment options, many plans offer a range of choices, from age-based portfolios to more conservative options. Also, explore the possibility of Coverdell Education Savings Accounts (ESAs), which provide more control over your investments, though with a lower contribution limit.

Don’t overlook the benefits of employer-sponsored tuition assistance programs. Many companies offer these as part of their benefits package, providing a direct path to fund your education while gaining valuable work experience. Additionally, consider community college credits as a cost-effective strategy. By completing your general education requirements at a lower cost, you can save significantly on tuition fees. scholarships and grants are invaluable resources that shouldn’t be ignored; dedicate time each month to search and apply for these opportunities.

Utilize Tax-Advantaged Accounts for Late Starters

For those who find themselves starting late in the college savings game, tax-advantaged accounts can be a powerful ally. These accounts not only offer the potential for growth but also provide significant tax benefits that can help accelerate your savings. Consider the following options:

- 529 Plans: These state-sponsored savings plans allow your investments to grow tax-free, and withdrawals for qualified education expenses are also tax-free. Many states offer tax deductions or credits for contributions, making them an attractive choice for late starters.

- Coverdell Education Savings Accounts (ESAs): While they have lower contribution limits compared to 529 Plans, ESAs offer more flexibility in investment choices. The earnings grow tax-free, and you can use the funds for both college and K-12 education expenses.

- Roth IRAs: While primarily a retirement savings tool, Roth IRAs can be tapped into for educational expenses without penalty. Contributions can be withdrawn tax-free at any time, offering a dual-purpose savings strategy.

By leveraging these accounts, you can maximize your contributions and potentially reduce your tax burden, providing a more robust financial footing as you catch up on your college savings goals.

{kind=link}