In an era marked by economic volatility and rapid market shifts, crafting a robust investment plan tailored to your family’s future is not just prudent—it’s essential. Navigating the complexities of financial planning can be daunting, yet with a strategic approach, it becomes a powerful tool for securing long-term prosperity. This article delves into the critical components of developing a personalized investment plan, emphasizing the importance of setting clear objectives, assessing risk tolerance, and diversifying assets. By adopting an analytical mindset and leveraging proven financial principles, you can confidently steer your family’s financial journey toward a stable and promising future.

Assessing Financial Goals and Risk Tolerance

Understanding your family’s financial aspirations and risk tolerance is crucial when crafting an investment strategy. Start by clearly defining what your financial goals are. Are you saving for your children’s education, a comfortable retirement, or perhaps a dream vacation home? Establishing specific, measurable objectives will help guide your investment decisions. Once your goals are outlined, assess your family’s risk tolerance by considering factors such as age, income stability, and investment experience. Risk tolerance varies from one family to another, and it’s essential to find a balance between potential returns and the level of risk you’re comfortable taking on.

- Short-term goals: These might include saving for a family vacation or a new car. Generally, lower-risk investments are preferred for these objectives.

- Medium-term goals: Examples include saving for a down payment on a house or your children’s college tuition. A mix of low to moderate-risk investments may be suitable.

- Long-term goals: These could involve planning for retirement or building generational wealth. Consider higher-risk investments that offer greater potential returns over time.

By systematically evaluating your financial targets and risk appetite, you create a robust foundation for your investment plan, ensuring it aligns with your family’s aspirations and financial comfort level.

Diversifying Your Investment Portfolio

One of the key principles in creating a robust investment plan for your family’s future is the diversification of your investment portfolio. By spreading your investments across a range of asset classes, you can mitigate risks and enhance potential returns. This approach ensures that the poor performance of one asset doesn’t drastically affect the overall health of your portfolio. Consider incorporating a mix of the following asset types:

- Stocks: Offer the potential for high returns but come with higher volatility. A well-researched selection of stocks can provide significant growth over the long term.

- Bonds: Typically less volatile than stocks, bonds can offer stable income and act as a buffer during market downturns.

- Real Estate: Provides tangible assets and potential rental income, along with the opportunity for appreciation.

- Mutual Funds and ETFs: Offer a way to invest in a diversified portfolio of stocks or bonds, managed by professionals.

- Alternative Investments: Consider assets like commodities, hedge funds, or even cryptocurrencies to further diversify and capitalize on niche markets.

By maintaining a balanced and varied investment strategy, you can better position your family to achieve financial stability and growth, regardless of market fluctuations. Regularly review and adjust your portfolio to align with your financial goals and risk tolerance.

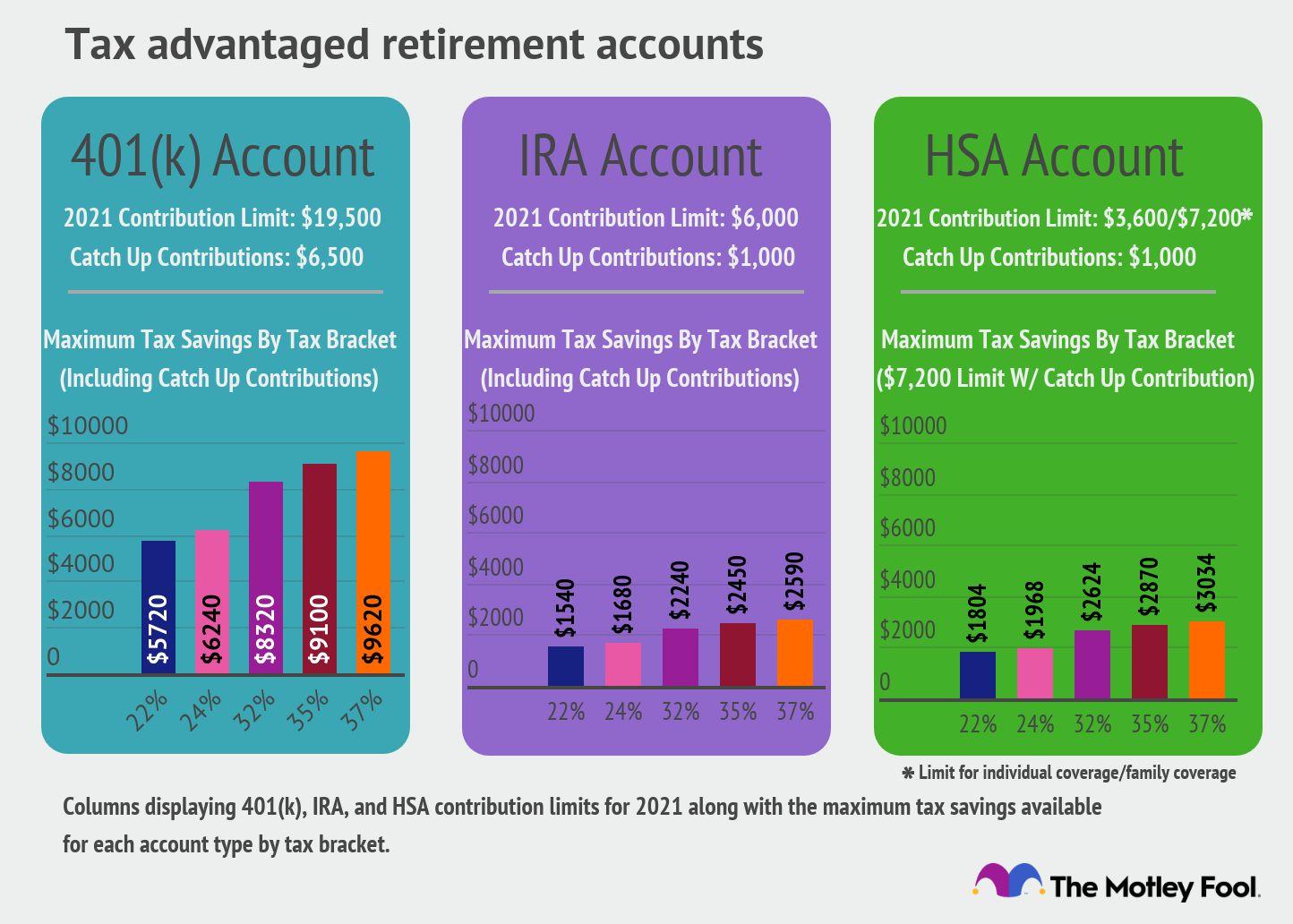

Leveraging Tax-Advantaged Accounts

Utilizing tax-advantaged accounts is a powerful strategy for enhancing your family’s financial future. These accounts, such as 401(k)s, IRAs, and 529 plans, offer unique benefits that can significantly reduce your tax burden while promoting long-term growth. By investing in these accounts, you can take advantage of tax deferral or even tax-free growth, allowing your investments to compound more effectively over time.

- 401(k) and Traditional IRA: Contributions may be tax-deductible, lowering your taxable income in the year they are made.

- Roth IRA: While contributions are made with after-tax dollars, withdrawals in retirement are tax-free, offering potential tax savings during your golden years.

- 529 Plan: Specifically designed for education savings, these accounts provide tax-free growth and withdrawals for qualified educational expenses.

By strategically allocating funds into these accounts, you not only prepare for retirement and educational expenses but also optimize your tax strategy, ensuring more of your money works for your family’s goals.

Monitoring and Adjusting Your Investment Strategy

As you embark on the journey of securing your family’s financial future, it’s crucial to regularly assess and refine your investment approach. The financial landscape is dynamic, and what works today might not be as effective tomorrow. Consistent monitoring of your investments ensures that your strategy aligns with your evolving financial goals and the changing market conditions. Consider the following steps to keep your investment plan on track:

- Set regular review intervals: Establish specific times to evaluate your portfolio, such as quarterly or bi-annually, to maintain a proactive approach.

- Assess performance against benchmarks: Compare your investment returns to relevant market indices to gauge effectiveness.

- Rebalance when necessary: Adjust the allocation of your assets to maintain the desired level of risk and return, especially after significant market shifts.

- Stay informed: Keep abreast of economic trends and policy changes that may impact your investments.

By integrating these practices into your investment routine, you can better safeguard your family’s financial future and ensure your strategy remains both relevant and robust. Adapting to changes with a calculated and informed mindset can make all the difference in achieving long-term financial success.

{kind=link}