Navigating the financial landscape of higher education can be a daunting task for families planning for the future. With the cost of college tuition continually on the rise, it’s essential to explore options that can help ease this financial burden. One such option is prepaid college tuition plans, a strategic approach to securing a child’s educational future at today’s rates. This article aims to provide you with a comprehensive understanding of prepaid college tuition plans, explaining how they work, their benefits, and potential drawbacks. By the end, you’ll be equipped with the knowledge to decide if this path aligns with your financial goals and educational aspirations. Let’s delve into the details and discover how you can take control of your family’s educational investment with confidence.

Understanding How Prepaid College Tuition Plans Work

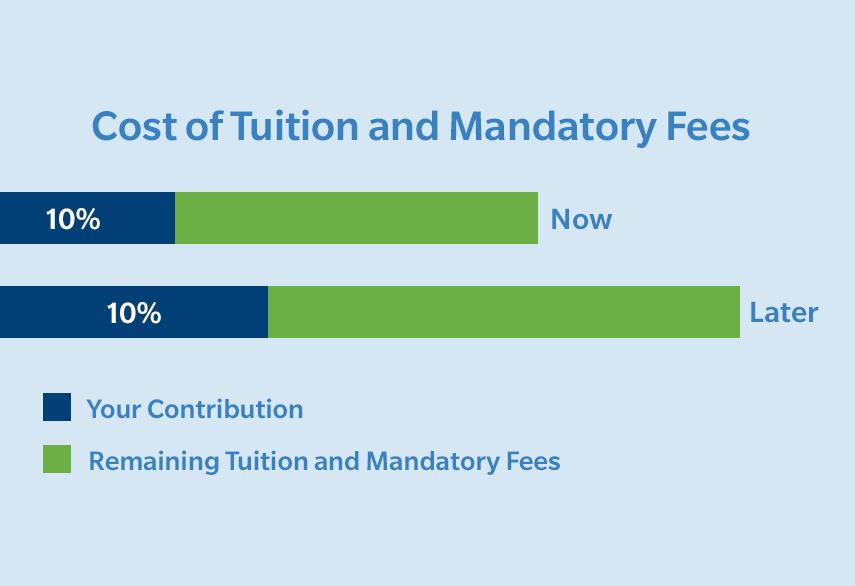

Prepaid college tuition plans are a unique financial tool that allow families to pay for future college tuition at current rates. These plans offer the benefit of locking in tuition costs, which can be a significant advantage given the rising cost of higher education. Typically, they are sponsored by state governments and are often guaranteed by the state, providing a layer of security for investors.

When considering a prepaid tuition plan, it’s important to understand the key features:

- State Residency Requirements: Most plans require either the purchaser or the beneficiary to be a resident of the state offering the plan.

- Eligible Institutions: Plans usually cover tuition at public colleges and universities within the state, but some may allow funds to be used at private or out-of-state institutions, often with limitations.

- Transferability: Many plans offer the flexibility to transfer the benefits to other family members if the original beneficiary decides not to attend college.

By understanding these components, families can make informed decisions about whether a prepaid college tuition plan aligns with their educational and financial goals.

Evaluating the Pros and Cons of Prepaid Tuition Options

When considering prepaid college tuition plans, it’s essential to weigh both the advantages and potential drawbacks. Advantages include the ability to lock in current tuition rates, providing a hedge against the unpredictable rise in educational costs. This can significantly ease the financial planning burden for families, ensuring that future tuition is covered regardless of inflation. Moreover, these plans often come with tax benefits, such as growth that is free from federal income tax, enhancing their appeal as a smart financial strategy.

However, there are potential drawbacks to consider. These plans are typically state-specific, which might limit your child’s educational options to in-state institutions. If your child decides to attend a private or out-of-state college, the plan might not cover the full tuition, resulting in unexpected expenses. Additionally, prepaid plans can be less flexible compared to other savings options, as they are often non-refundable or come with penalties for cancellation. Before committing, it’s crucial to thoroughly understand the terms and conditions, ensuring the plan aligns with your long-term educational goals.

Choosing the Right Prepaid Plan for Your Familys Needs

When considering prepaid college tuition plans, it’s essential to match the plan’s offerings with your family’s specific educational goals and financial situation. Here are some key factors to keep in mind:

- Plan Coverage: Determine whether the plan covers tuition and fees only or includes room and board. Some plans might also offer options for out-of-state or private institutions, which could be crucial if your family values flexibility in college choice.

- Payment Flexibility: Review the payment options available. Many plans offer lump-sum payments or installment plans, allowing you to choose what aligns best with your family’s cash flow.

- Transferability: If you have multiple children, consider whether the plan allows for the transfer of benefits among siblings. This can provide peace of mind if one child decides not to attend college.

- Refund Policy: Life is unpredictable, and your child’s educational path might change. Check the plan’s refund policy to ensure you understand what happens if the plan is unused or if your child receives a scholarship.

Evaluate these aspects carefully to ensure you select a prepaid plan that not only aligns with your family’s current needs but also offers flexibility for the future. A well-chosen plan can provide a significant financial advantage while securing your child’s educational journey.

Expert Tips for Maximizing Your Prepaid Tuition Investment

Unlock the full potential of your prepaid tuition plan with these strategic insights. Start by evaluating the scope of your plan. Some plans cover only tuition, while others might include fees and room and board. Understanding these nuances can help you plan your finances more effectively.

- Research Transferability: Investigate if your plan allows transferring credits to out-of-state or private institutions. This flexibility can significantly broaden your child’s educational opportunities.

- Stay Informed on Deadlines: Keep track of enrollment and payment deadlines to avoid any last-minute surprises. Missing these could lead to penalties or loss of benefits.

- Maximize State Benefits: In some regions, prepaid tuition plans offer tax advantages. Consult a financial advisor to ensure you’re making the most of these incentives.

To truly capitalize on your investment, maintain regular communication with the plan administrator. This ensures you’re updated on any changes in terms and conditions, which can directly impact your educational savings strategy.

{kind=link}