Creating a family savings plan for major life events is a crucial step toward securing your family’s financial future and ensuring that you’re prepared for the inevitable milestones that life brings. Whether you’re planning for a child’s education, a dream wedding, or a comfortable retirement, having a structured savings plan can provide peace of mind and financial stability. In this guide, we will walk you through the essential steps to develop an effective savings strategy tailored to your family’s unique needs and goals. With confidence and clarity, we’ll explore practical tips, expert advice, and proven techniques to help you navigate the complexities of financial planning. By the end of this article, you’ll be equipped with the knowledge and tools necessary to create a robust savings plan that can adapt to life’s changes and help your family thrive.

Identifying Key Life Events and Setting Savings Goals

Understanding the pivotal moments in life that require financial preparation is essential for crafting a robust family savings plan. These key events can range from the joyous arrival of a new child to the bittersweet transition into retirement. By identifying these milestones early, you can tailor your savings strategy to meet the demands of each life stage with confidence.

To effectively plan, consider the following major life events that often require substantial financial outlay:

- Education: Whether it’s saving for your child’s college tuition or furthering your own education, setting aside funds for academic pursuits can alleviate future stress.

- Homeownership: From the down payment to ongoing maintenance, owning a home is a significant financial commitment.

- Retirement: Ensuring a comfortable retirement requires early and consistent savings.

- Healthcare: Unexpected medical expenses can arise at any time, making an emergency fund a critical component of your savings plan.

- Travel and Leisure: Creating memories through travel or pursuing hobbies can enrich life, but requires financial foresight.

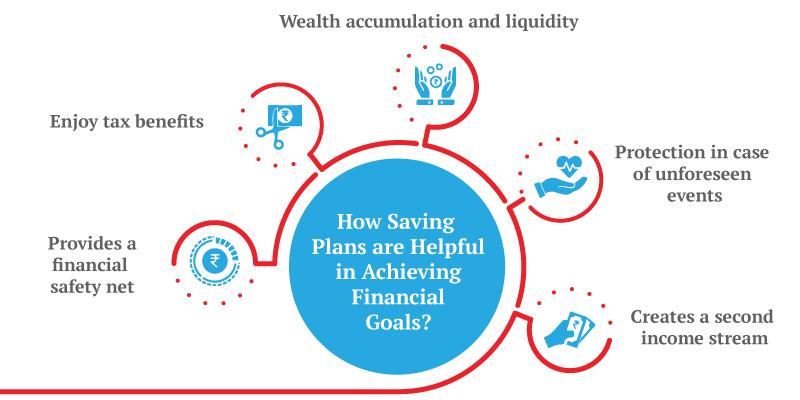

By setting clear, achievable savings goals for these events, you can ensure that your family is prepared for whatever the future holds. Use a mix of savings accounts, investment strategies, and insurance products to build a comprehensive plan that aligns with your family’s unique needs and aspirations.

Building a Realistic Budget to Support Your Savings Plan

Crafting a budget that aligns with your savings goals requires a strategic approach to ensure financial stability and success. Begin by evaluating your household’s monthly income and expenses to gain a clear picture of your financial standing. List all your fixed expenses such as mortgage or rent, utilities, insurance, and any other mandatory monthly payments. Next, identify your variable expenses like groceries, entertainment, and dining out. By categorizing these, you can easily spot areas where you can cut back.

Once you’ve outlined your expenses, establish a realistic budget that accommodates your savings plan. Consider the following steps to optimize your budget:

- Prioritize your savings by setting aside a fixed amount from your income as soon as you receive it. Treat this like a non-negotiable bill.

- Adjust discretionary spending to free up more funds for savings. This could mean dining out less frequently or finding more affordable entertainment options.

- Review and adjust your budget regularly to ensure it remains aligned with your financial goals and any changes in your circumstances.

With a disciplined approach and regular reviews, your budget will not only support your current lifestyle but also bolster your family’s savings plan for future milestones.

Choosing the Right Savings Accounts and Investment Options

When embarking on a journey to create a family savings plan for major life events, selecting the appropriate savings accounts and investment options is crucial. Start by evaluating your family’s financial goals and timelines. Consider high-yield savings accounts for short-term needs, offering a balance of accessibility and higher interest rates compared to traditional savings accounts. These accounts can serve as a secure repository for emergency funds or near-future expenses, such as a family vacation or home renovation.

For long-term aspirations, explore diverse investment avenues. Mutual funds and index funds are excellent choices for those seeking to diversify with minimal effort, while stocks may appeal to those comfortable with market fluctuations. Additionally, consider bonds for a more stable, albeit lower, return. Here are a few strategies to guide your decisions:

- Assess Risk Tolerance: Understand your comfort level with potential losses to tailor investments that align with your family’s risk appetite.

- Time Horizon: Choose options that match your investment duration, ensuring liquidity aligns with anticipated financial needs.

- Tax Implications: Consider tax-advantaged accounts, such as IRAs or 529 plans, for retirement savings or education expenses, respectively.

By strategically aligning your savings and investment choices with your family’s unique goals and timelines, you can build a robust financial foundation for life’s major milestones.

Monitoring Progress and Adjusting Your Plan for Success

To ensure your family savings plan remains effective and aligned with your goals, it’s crucial to regularly monitor progress and make necessary adjustments. Start by setting a schedule for reviewing your savings plan, such as monthly or quarterly. During these reviews, assess the following:

- Budget Alignment: Check if your spending and saving habits are in line with your initial budget. Identify any areas where you might be overspending and brainstorm ways to cut back.

- Goal Progress: Evaluate how close you are to reaching your savings goals for each major life event. If you find yourself falling short, consider revising your saving strategies or setting more achievable targets.

- Unexpected Changes: Life is full of surprises, both good and bad. Be prepared to adapt your plan in response to changes such as job transitions, family expansions, or unforeseen expenses.

By keeping a close eye on these aspects, you’ll be able to adjust your plan proactively, ensuring that your family’s financial future remains secure and on track for success.

{kind=link}