Managing debt is a challenge that many people face, yet with the right strategies and a proactive approach, it’s entirely possible to regain financial control and pave the way to a more secure future. In this article, we will guide you through practical steps to effectively manage and reduce your debt, empowering you to take charge of your financial health. By implementing these strategies, you’ll not only alleviate the stress associated with debt but also build a solid foundation for achieving your long-term financial goals. Whether you’re dealing with credit card balances, student loans, or other forms of debt, this comprehensive guide will provide you with the tools and confidence you need to transform your financial situation. Let’s embark on this journey to financial freedom together, one practical step at a time.

Understanding Your Debt Situation

To gain control over your debt, it’s essential to first grasp the full scope of your financial obligations. Start by compiling a comprehensive list of all your debts. This should include credit cards, student loans, mortgages, and any other liabilities. For each debt, note the total amount owed, interest rate, minimum monthly payment, and the due date. This step will provide a clear snapshot of where you stand and highlight the most pressing obligations.

Understanding your debt also means recognizing patterns and behaviors that may have contributed to your current situation. Consider these factors:

- Spending habits: Are there areas where you can cut back?

- Income vs. expenses: Is your income sufficient to cover all necessary expenses?

- Emergency savings: Do you have a buffer to prevent further debt accumulation?

By thoroughly assessing your debt situation, you equip yourself with the knowledge needed to make informed decisions and prioritize debt repayment strategies effectively.

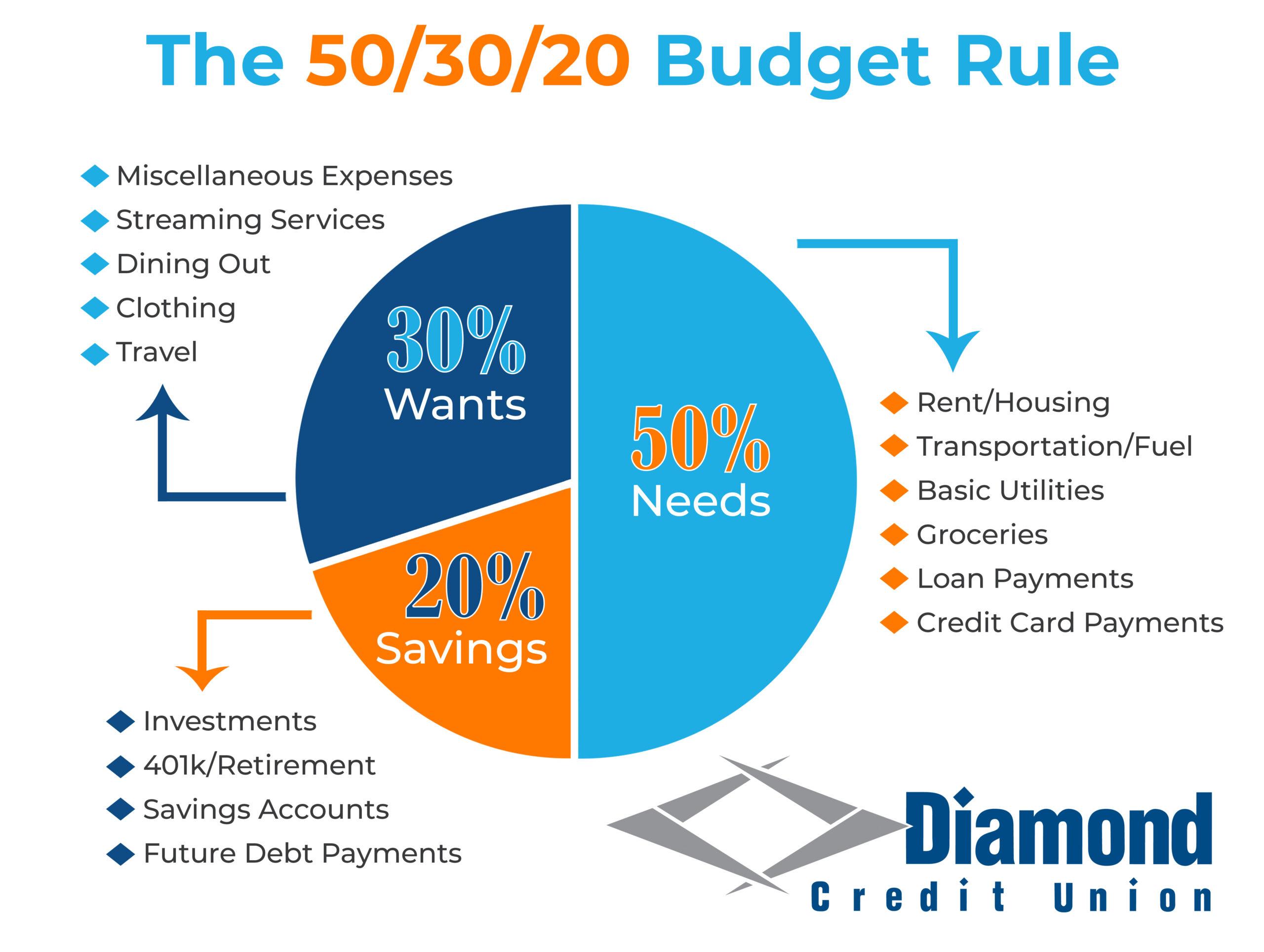

Crafting a Realistic Budget Plan

Creating a budget plan that accurately reflects your financial reality is crucial for managing debt effectively. Start by listing all your income sources and monthly expenses. Be thorough and include every possible cost, from fixed expenses like rent or mortgage payments to variable costs such as groceries and entertainment. It’s essential to have a clear picture of where your money is going. Once you have your list, categorize these expenses into essential and non-essential. This will help you identify areas where you can cut back.

- Track Spending: Use apps or spreadsheets to monitor your daily expenses. This will help you stay on top of your spending habits and adjust your budget as needed.

- Set Realistic Goals: Establish achievable financial goals, such as reducing dining out by 20% or saving an extra $100 each month.

- Allocate Funds for Debt Repayment: Designate a specific portion of your budget towards paying off debt. Prioritize high-interest debts to minimize future financial burdens.

By implementing these strategies, you’ll gain better control over your finances, paving the way to a debt-free future. Remember, a budget is not a one-time setup but a dynamic tool that requires regular review and adjustment to stay aligned with your financial goals.

Prioritizing and Consolidating Your Debts

When faced with multiple debts, it’s crucial to determine which ones need immediate attention. Begin by listing all your debts, including the outstanding balance, interest rates, and monthly payments. This will provide a clear picture of your financial obligations and help you identify which debts are costing you the most. High-interest debts, such as credit card balances, should be prioritized, as they accrue more interest over time, potentially increasing your financial burden.

Once priorities are set, consider consolidating your debts. Debt consolidation involves merging multiple debts into a single loan with a lower interest rate. This can simplify your repayment process and reduce the amount you pay each month. Benefits of consolidation include:

- Lower interest rates

- Simplified payments

- Potential improvement in credit score

Ensure you choose a consolidation option that suits your financial situation, whether it’s a personal loan, balance transfer, or a debt management plan. By prioritizing and consolidating, you can regain control over your finances and work towards a debt-free future.

Exploring Professional Financial Advice

When tackling debt, leveraging the expertise of a financial advisor can be a game-changer. These professionals offer a wealth of knowledge and tailored strategies to help you regain financial stability. Here’s how a financial advisor can assist you:

- Comprehensive Debt Analysis: They start by reviewing your current debt situation, including interest rates, terms, and monthly obligations, providing a clear picture of where you stand.

- Personalized Repayment Plans: Advisors craft customized repayment strategies that align with your financial goals, often negotiating with creditors for better terms or lower interest rates.

- Budget Creation and Management: They assist in developing a realistic budget that prioritizes debt repayment while maintaining your essential living expenses.

- Education and Support: Beyond immediate solutions, advisors educate you on financial management, ensuring you have the tools and knowledge to stay debt-free in the future.

Choosing to work with a financial advisor is a proactive step towards mastering your debt. With their guidance, you’ll gain not only a plan but also the confidence to execute it effectively.

{kind=link}