In the ever-evolving landscape of financial markets, managing retirement accounts through periods of volatility can be a daunting yet essential task for securing your financial future. Market fluctuations, while inevitable, do not have to derail your long-term goals if approached with strategic foresight and disciplined practices. This article delves into the best practices for navigating these turbulent times, empowering you with the knowledge and confidence to make informed decisions. Whether you’re a seasoned investor or just beginning to build your retirement nest egg, these strategies will equip you with the tools necessary to weather market storms, preserve your assets, and optimize growth potential. By adopting a proactive and resilient approach, you can transform market volatility from a source of anxiety into an opportunity for growth and stability.

Assessing Risk Tolerance to Safeguard Your Retirement Portfolio

Understanding your personal risk tolerance is crucial when navigating the unpredictable waters of market volatility, especially in the context of retirement planning. This assessment involves evaluating your financial goals, investment horizon, and emotional capacity to handle market fluctuations. Begin by asking yourself how much risk you are comfortable taking and how it aligns with your retirement objectives. Consider factors like your age, income stability, and any potential financial obligations. By aligning your risk tolerance with your investment strategy, you can create a more resilient portfolio that can withstand the ups and downs of the market.

- Identify Your Risk Capacity: Assess your financial situation, including your current assets and liabilities, to understand how much risk you can realistically take on.

- Evaluate Emotional Tolerance: Reflect on past experiences with market volatility and how you reacted to them. This insight will help gauge your comfort level with potential losses.

- Set Clear Objectives: Define specific, measurable goals for your retirement portfolio, ensuring they are in line with your risk profile.

- Diversify Investments: Spread your investments across various asset classes to mitigate risks and reduce the impact of market swings.

- Regularly Reassess: Periodically review and adjust your portfolio to reflect changes in your financial situation or market conditions.

By thoroughly assessing and understanding your risk tolerance, you can develop a strategic approach to safeguarding your retirement portfolio, ensuring it remains robust against market volatility.

Diversifying Investments for Long-Term Stability

To achieve long-term stability in retirement accounts, it’s crucial to embrace a diversified investment strategy. This approach minimizes risk by spreading investments across various asset classes, which can include:

- Stocks: Offering potential for high returns, stocks should be balanced between domestic and international options to mitigate geographic risks.

- Bonds: These provide a more stable, predictable income stream, counteracting the volatility of the stock market.

- Real Estate: Investing in property can offer both income through rentals and capital appreciation.

- Commodities: Gold, silver, and other commodities can serve as a hedge against inflation and currency fluctuations.

- Mutual Funds and ETFs: These are excellent for gaining exposure to a wide range of assets without needing to select individual investments.

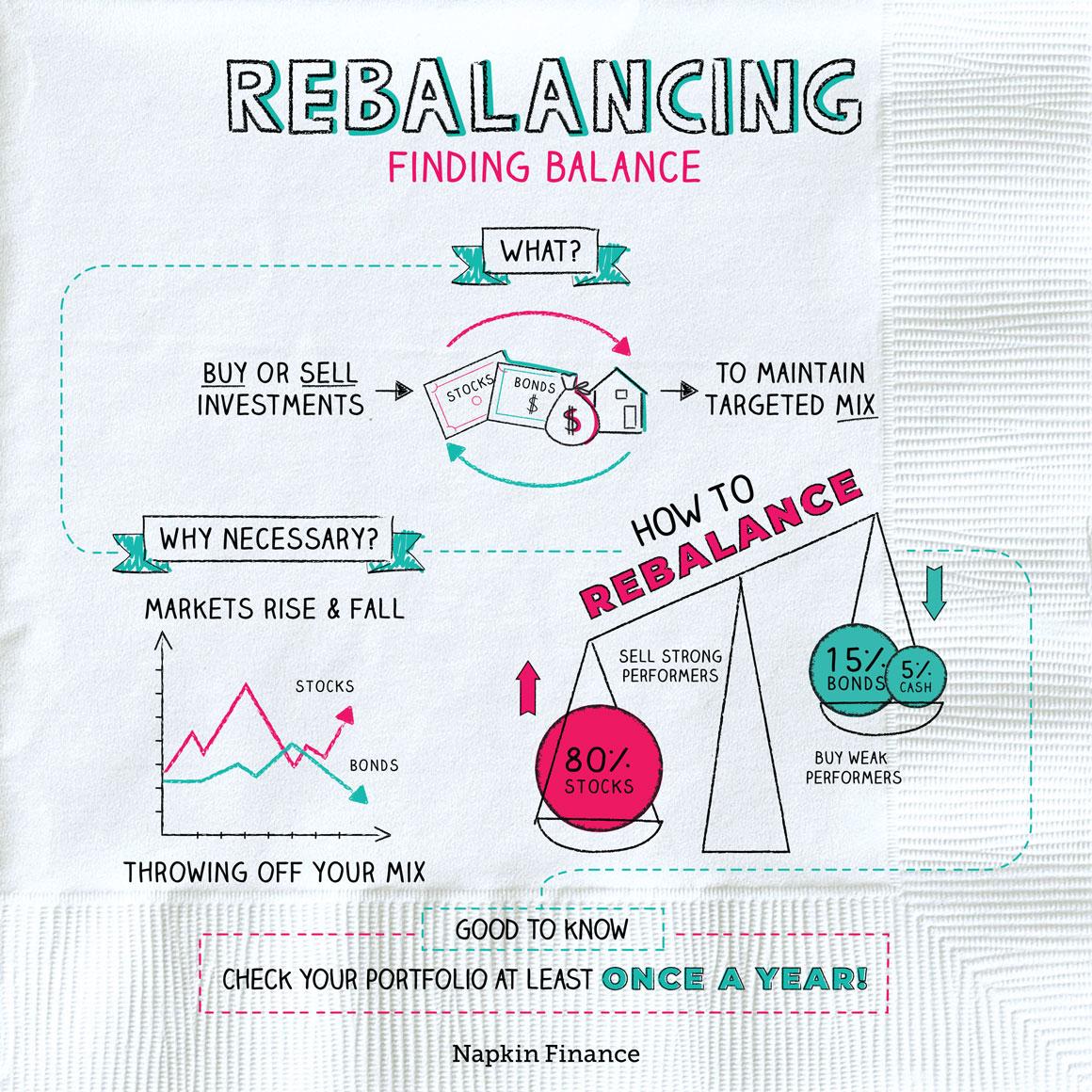

Regularly rebalancing your portfolio ensures that your investments remain aligned with your risk tolerance and financial goals. In times of market volatility, this disciplined approach allows you to capitalize on lower asset prices and maintain a strategic asset allocation. Keep a vigilant eye on market trends and economic indicators, adjusting your strategy as necessary to safeguard your retirement savings.

Timing Market Moves with Strategic Rebalancing

In the face of market turbulence, the art of strategic rebalancing becomes essential for maintaining the integrity of your retirement accounts. Strategic rebalancing involves adjusting your investment portfolio to realign with your long-term goals, ensuring that your asset allocation remains consistent with your risk tolerance. This proactive approach can help mitigate losses and capitalize on market opportunities. Consider the following best practices:

- Set a rebalancing schedule: Regularly review your portfolio, whether quarterly or annually, to adjust for market fluctuations.

- Establish target allocations: Clearly define your asset mix targets to guide your rebalancing decisions.

- Use a threshold-based approach: Rebalance only when your asset allocations deviate significantly from your targets, avoiding unnecessary transactions.

- Consider tax implications: Be mindful of the tax consequences when selling assets in taxable accounts, and utilize tax-advantaged accounts for rebalancing when possible.

By adhering to these strategies, you can navigate market volatility with confidence, ensuring that your retirement funds remain robust and aligned with your financial objectives.

Utilizing Professional Guidance to Navigate Economic Uncertainty

In times of economic turbulence, leveraging the expertise of financial advisors can be a strategic move to safeguard your retirement accounts. These professionals offer invaluable insights, helping you make informed decisions that align with your long-term goals. Here are some best practices to consider:

- Regular Portfolio Reviews: Ensure your investments remain aligned with your risk tolerance and retirement timeline by scheduling regular check-ins with your advisor.

- Diversification: A well-diversified portfolio can help mitigate risks. Your advisor can guide you in spreading investments across various asset classes.

- Stay Informed: Keep abreast of market trends and economic indicators with the help of your advisor’s expert analysis.

- Rebalancing: During volatile times, rebalancing your portfolio can help maintain your desired asset allocation, and your advisor can assist in executing this efficiently.

By working closely with a professional, you can navigate market fluctuations with confidence, ensuring your retirement strategy remains robust and resilient. Trust in their expertise to help you make the most of your retirement savings, even amidst economic uncertainty.

Contributions")

{kind=link}