In today’s fast-paced world, managing finances can be a daunting task, particularly for growing families striving to balance daily expenses with long-term goals. As your family expands, so do the financial responsibilities, making it essential to adopt effective budgeting strategies that ensure stability and security. This article delves into simple yet powerful budgeting techniques designed specifically for families experiencing growth. By implementing these strategies, you can gain control over your finances, reduce stress, and create a solid foundation for your family’s future. Whether you’re navigating the costs of childcare, education, or simply trying to save for a rainy day, these expert tips will guide you towards financial peace of mind, empowering you to make informed decisions and foster a thriving household.

Establishing a Family Financial Framework for Long-Term Stability

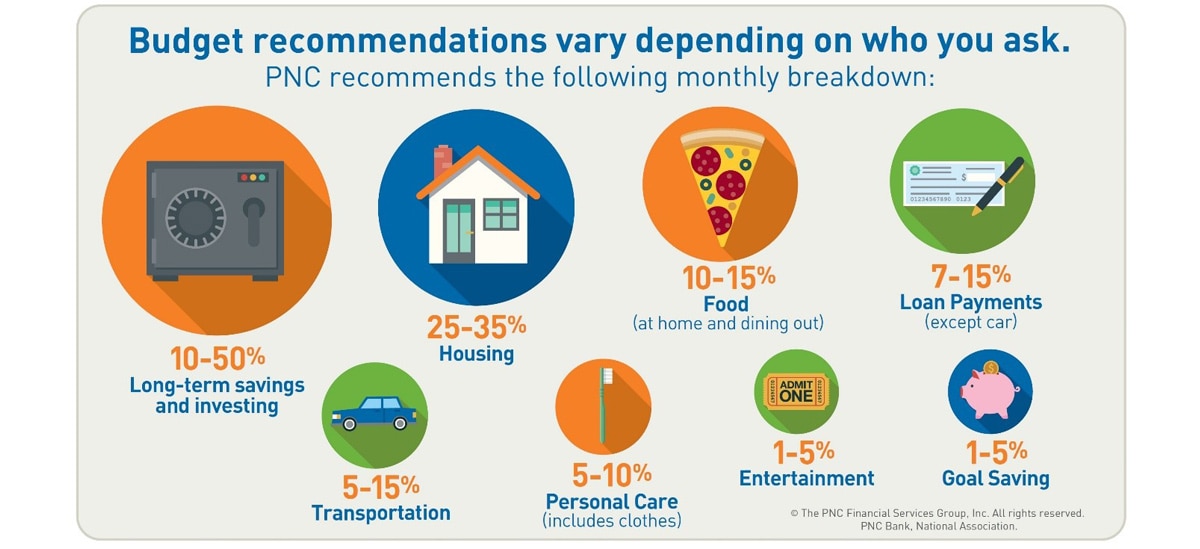

Building a solid financial foundation for your family starts with setting clear, realistic goals and crafting a budget that caters to both current needs and future aspirations. Begin by evaluating your monthly income and categorizing expenses into essential and discretionary items. Essential expenses include housing, utilities, groceries, and transportation, while discretionary items encompass dining out, entertainment, and hobbies. Tracking your spending habits through apps or spreadsheets can illuminate areas for potential savings, allowing you to allocate funds more efficiently.

Once you’ve identified where your money goes, it’s time to implement a 50/30/20 budgeting rule: allocate 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment. This simple yet effective strategy ensures that you’re living within your means while steadily working towards financial security. Consider establishing an emergency fund as a safety net for unexpected expenses, and regularly review your budget to adapt to changing family dynamics, such as the birth of a child or a job change. Remember, consistency and communication with your partner or family members are key to maintaining a healthy financial framework.

Prioritizing Essential Expenses While Accommodating Growth

In the midst of expanding family needs, it’s crucial to differentiate between essential expenses and those that can be adjusted or deferred. Essential expenses are the non-negotiables, the financial obligations that must be met to maintain the family’s well-being. These typically include:

- Housing Costs: Mortgage or rent payments, property taxes, and home insurance.

- Utilities: Electricity, water, gas, and necessary communication services.

- Groceries: Basic food supplies and household necessities.

- Healthcare: Health insurance premiums, medications, and routine medical check-ups.

- Transportation: Car payments, fuel, and maintenance for essential travel.

While these expenses form the foundation of your budget, accommodating growth requires strategic planning. Consider reallocating funds from discretionary spending to areas that support family expansion, such as education or home improvements. Implementing flexible budgeting techniques like setting aside a contingency fund can provide a cushion for unexpected costs associated with growth, ensuring that the family’s core needs remain secure.

Implementing Savings Strategies to Secure Your Family’s Future

Building a robust financial future for your family starts with mastering the art of budgeting. Embrace the envelope method to allocate cash for different spending categories. This traditional approach helps in curbing overspending and encourages discipline. Additionally, consider setting up automatic transfers to a dedicated savings account every month. This “pay yourself first” strategy ensures that saving becomes a priority rather than an afterthought.

- Meal Planning: Reduces food waste and saves money by sticking to a list.

- Utility Monitoring: Keep track of energy consumption to lower monthly bills.

- Subscription Audit: Regularly review and cancel unused services.

- Emergency Fund: Aim for 3-6 months of living expenses to cover unforeseen events.

Leveraging Budgeting Tools for Effective Financial Management

In today’s fast-paced world, keeping track of your family’s finances can be challenging, but modern budgeting tools can make this task significantly more manageable. Digital budgeting applications offer a comprehensive view of your income and expenses, helping you identify areas where you can cut costs and save more effectively. These tools often provide features such as automatic transaction tracking, customizable spending categories, and even alerts for upcoming bills, ensuring you never miss a due date. Embracing these technologies can transform your financial management approach from reactive to proactive, allowing you to make informed decisions that align with your family’s financial goals.

To maximize the benefits of these tools, consider implementing the following strategies:

- Set Clear Financial Goals: Define what you want to achieve financially, whether it’s saving for a family vacation, college fund, or emergency savings.

- Create a Realistic Budget: Use your budgeting tool to establish a monthly budget that reflects your actual income and expenses, adjusting as necessary to accommodate changes in your family’s needs.

- Monitor Spending Regularly: Check your budgeting app frequently to ensure you’re staying on track, and make adjustments as needed to avoid overspending.

- Involve the Entire Family: Encourage family members to participate in financial discussions and understand the budget, fostering a team effort in achieving financial stability.

{kind=link}