Tackling credit card debt can often feel like an uphill battle, but with the right strategies in place, financial freedom is within reach. In today’s fast-paced world, managing debt is not just about making minimum payments; it’s about employing effective techniques that lead to long-term success. Whether you’re dealing with a mountain of debt or just looking to streamline your financial health, this article will guide you through the most effective strategies for paying off credit card debt. With confidence and clarity, we will explore actionable steps that can transform your financial situation, empowering you to take control and pave the way to a debt-free future. Let’s dive into the methods that will not only alleviate your financial burdens but also build a solid foundation for your financial well-being.

Understanding Your Debt Situation

Before diving into repayment strategies, it’s crucial to have a clear picture of where you stand financially. Start by compiling a list of all your credit card debts, including the balance, interest rate, and minimum payment for each. This list will serve as your roadmap, guiding your journey towards financial freedom. Understanding your current debt situation is the foundation for creating an effective plan. It enables you to prioritize which debts to tackle first and recognize any patterns in your spending habits that may need adjusting.

- Review Your Statements: Go through recent credit card statements to identify any unnecessary expenses that can be reduced or eliminated.

- Calculate Your Debt-to-Income Ratio: Divide your total monthly debt payments by your gross monthly income. A lower ratio indicates a healthier financial situation.

- Check Your Credit Report: Ensure there are no errors or fraudulent activities affecting your credit score, as this can impact your ability to negotiate better terms.

By systematically evaluating these aspects, you gain valuable insights into your financial health, empowering you to make informed decisions. Remember, clarity is the first step towards control.

Crafting a Personalized Repayment Plan

When it comes to conquering credit card debt, customization is key. A one-size-fits-all approach may not work for everyone, so it’s crucial to tailor your repayment plan to fit your unique financial situation. Start by assessing your debts: make a list of all your credit cards, noting the balance, interest rate, and minimum payment for each. This will help you prioritize which debts to tackle first. Consider the following strategies:

- Debt Avalanche: Focus on paying off the card with the highest interest rate first while making minimum payments on others. This can save you money on interest over time.

- Debt Snowball: Pay off the smallest debt first to gain momentum and a psychological boost, then move to the next smallest debt.

- Hybrid Approach: Combine elements of both the avalanche and snowball methods to suit your needs, such as starting with the smallest high-interest debt.

Ensure your plan is flexible enough to accommodate unexpected expenses or changes in income. Regularly reviewing your progress can keep you motivated and on track. Remember, the goal is to find a strategy that not only aligns with your financial objectives but also fits seamlessly into your lifestyle.

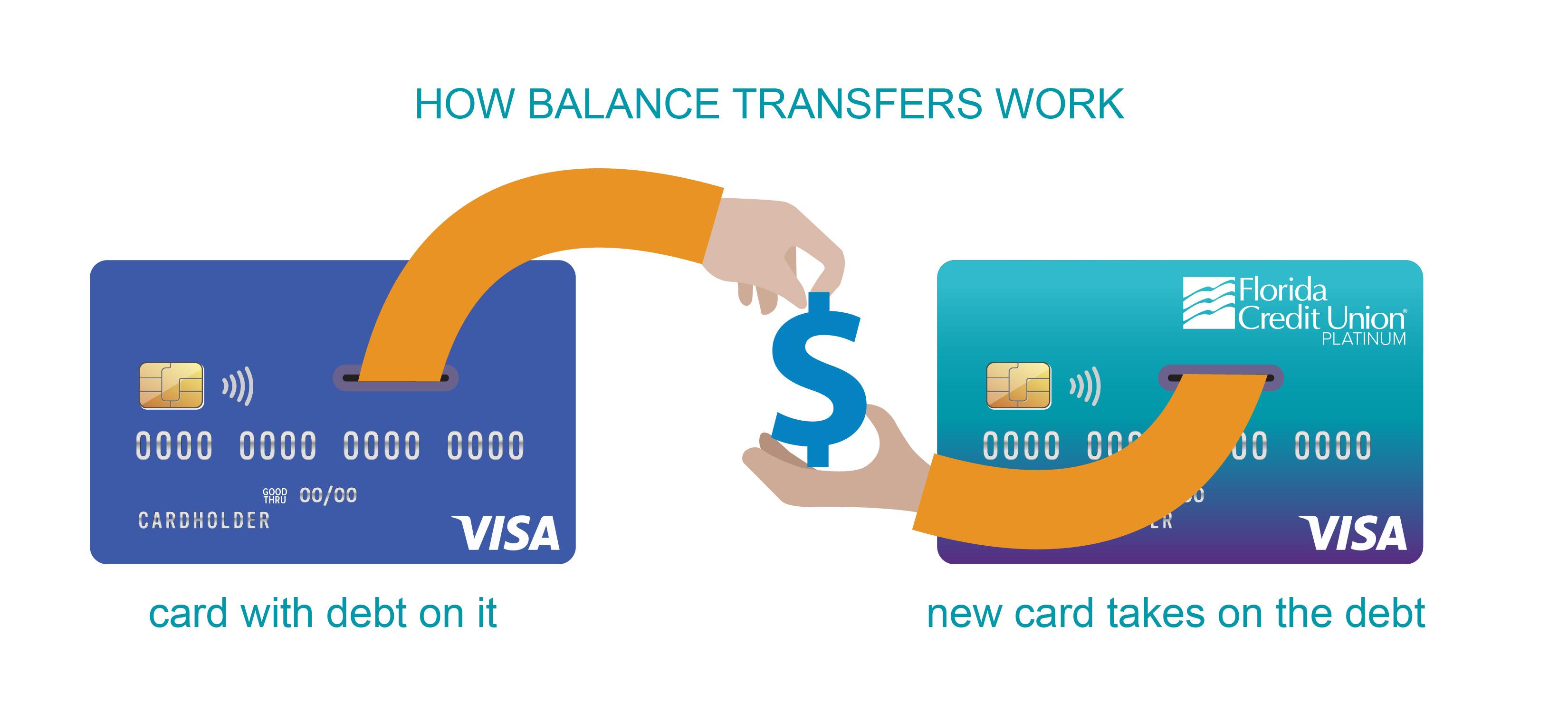

Maximizing Savings with Balance Transfers

One powerful strategy to tackle credit card debt is leveraging balance transfers. This involves transferring your existing high-interest credit card balances to a new card with a lower interest rate, often 0% for an introductory period. This approach can significantly reduce the amount you pay in interest, allowing more of your payments to chip away at the principal debt. To maximize savings, consider the following tips:

- Read the Fine Print: Ensure you understand the terms, including the duration of the introductory rate and any balance transfer fees.

- Calculate Potential Savings: Compare the fees and interest savings to determine if the transfer is beneficial.

- Pay Off Debt Within the Introductory Period: Aim to eliminate your balance before the regular interest rate kicks in.

- Avoid New Purchases: Focus on paying off the transferred balance without adding new charges to the card.

By strategically using balance transfers, you can accelerate your journey to becoming debt-free, all while keeping more money in your pocket.

Utilizing Extra Income to Accelerate Debt Reduction

When it comes to accelerating your journey towards a debt-free life, leveraging extra income can be a game-changer. Start by allocating any additional funds directly towards your highest interest debt. This strategy not only reduces the principal balance but also minimizes the amount of interest you accrue over time, helping you save money in the long run. Consider using bonuses, tax refunds, or any unexpected windfalls to make substantial payments that can significantly chip away at your debt. Remember, every little bit counts, and consistent efforts can lead to major progress.

- Freelance Work: Utilize your skills to take on freelance projects or part-time jobs. The extra earnings can make a big impact when used wisely.

- Sell Unused Items: Declutter your home and sell items you no longer need. This not only frees up space but also provides extra cash to reduce your debt.

- Side Hustles: Engage in side hustles that align with your interests. Whether it’s pet sitting, ride-sharing, or crafting, additional income streams can boost your debt repayment efforts.

By strategically directing extra income towards your credit card balances, you not only shorten the repayment timeline but also cultivate financial discipline that can be beneficial in the future. Make every dollar count and watch your debt diminish faster than you imagined.

{kind=link}