In today’s fast-paced financial landscape, high-interest debt can quickly become a formidable obstacle, threatening to derail your financial stability and peace of mind. Yet, paying off this debt does not have to mean sacrificing life’s essentials or compromising your quality of life. This guide will equip you with practical strategies and a confident mindset to tackle high-interest debt effectively. By leveraging proven techniques and making informed decisions, you can regain control of your finances, ensuring that your journey to financial freedom is both sustainable and empowering. Whether you’re dealing with credit card balances, personal loans, or other high-interest obligations, this article will illuminate a path forward, allowing you to pay down debt without sacrificing the essentials that matter most to you.

Understanding High Interest Debt and Its Impact

High interest debt, such as credit card balances or payday loans, can be a significant financial burden. The impact of these debts is multifaceted, often affecting both your financial health and emotional well-being. Interest rates can soar above 20%, making it difficult to reduce the principal balance. This type of debt can lead to a cycle where payments only cover interest, leaving the principal untouched. Understanding the implications of high interest debt is crucial for financial planning and stability.

The ramifications extend beyond just financial strain. High interest debt can negatively impact your credit score, making it challenging to secure loans or even rent a home. It can also lead to stress and anxiety, affecting your overall quality of life. Here are a few key effects of high interest debt:

- Increased financial stress and pressure.

- Limited ability to save for future goals.

- Potential damage to creditworthiness.

Addressing these issues with a strategic plan is essential for regaining control over your financial future.

Crafting a Realistic Budget to Prioritize Essentials

Establishing a realistic budget is crucial when tackling high-interest debt, ensuring you don’t compromise on life’s essentials. Start by distinguishing between needs and wants. Focus on fundamental expenses such as housing, utilities, groceries, and healthcare. These are non-negotiables that keep your household running smoothly.

- Housing: Evaluate your current living situation. Could refinancing or downsizing be viable options to reduce monthly costs?

- Utilities: Analyze past bills to identify usage patterns and potential savings. Implement energy-saving measures to lower costs.

- Groceries: Plan meals ahead, buy in bulk, and opt for generic brands to keep this expense in check.

- Healthcare: Ensure you’re getting the best value from your health insurance and take advantage of preventive care options.

Once these essentials are secured, allocate a portion of your income towards debt repayment. This strategic allocation not only prioritizes your well-being but also accelerates your journey to financial freedom.

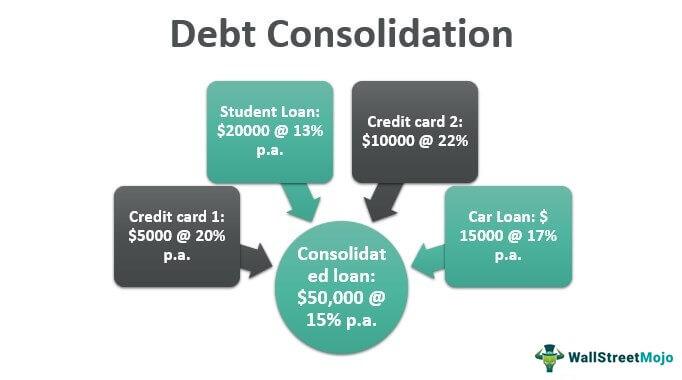

Exploring Debt Consolidation and Refinancing Options

When managing high-interest debt, it’s crucial to explore strategies that allow you to maintain your lifestyle essentials. Debt consolidation and refinancing are two viable options that can significantly ease your financial burden. By consolidating your debts, you combine multiple high-interest obligations into a single, lower-interest loan. This not only simplifies your payments but often reduces the total interest paid over time. Refinancing, on the other hand, involves negotiating a new loan to replace an existing one, potentially with more favorable terms such as a lower interest rate or extended payment period.

Before diving into these options, consider the following steps:

- Evaluate Your Debt: List all your debts, interest rates, and monthly payments to understand your current financial situation.

- Research Lenders: Look for reputable lenders who offer competitive rates for consolidation or refinancing.

- Calculate Savings: Use online calculators to estimate potential savings from lower interest rates and extended terms.

- Check Your Credit Score: A higher credit score can qualify you for better rates, so it might be worth improving it before applying.

- Read the Fine Print: Ensure you understand any fees, penalties, or changes in terms before committing to a new financial agreement.

By carefully considering these options and taking strategic steps, you can reduce your debt burden without sacrificing the essentials of daily life.

Implementing Effective Strategies for Steady Debt Reduction

One of the most critical steps in reducing high-interest debt is creating a tailored repayment plan that suits your financial situation. Begin by listing all your debts, focusing on those with the highest interest rates first. This approach, often referred to as the “avalanche method,” ensures that you minimize the amount of interest paid over time. Set clear, achievable goals and track your progress regularly to stay motivated.

While paying down debt, it’s crucial not to overlook your essential needs. Prioritize your spending by distinguishing between wants and necessities. Consider these strategies to maintain balance:

- Establish a realistic budget that allocates funds to both debt repayment and essential expenses.

- Automate savings for emergencies to avoid falling back into debt when unexpected costs arise.

- Negotiate better rates with creditors where possible, potentially lowering your monthly payments.

By adopting these strategies, you can effectively manage your debt without sacrificing your essential needs, paving the way for a more secure financial future.

{kind=link}