In today’s ever-evolving financial landscape, securing a robust education for future generations is a paramount concern for many families. As tuition costs continue to rise, finding effective strategies to save for education expenses becomes increasingly critical. One of the most powerful tools at your disposal is the education investment account, designed not only to support academic aspirations but also to offer significant tax advantages. In this article, we will delve into the best tax benefits associated with these accounts, equipping you with the knowledge to make informed decisions that maximize your savings and minimize your tax burden. Whether you’re a parent, grandparent, or guardian, understanding these tax advantages will empower you to strategically invest in education, ensuring that your loved ones have access to the opportunities they deserve.

Understanding Tax-Free Growth Opportunities in Education Savings

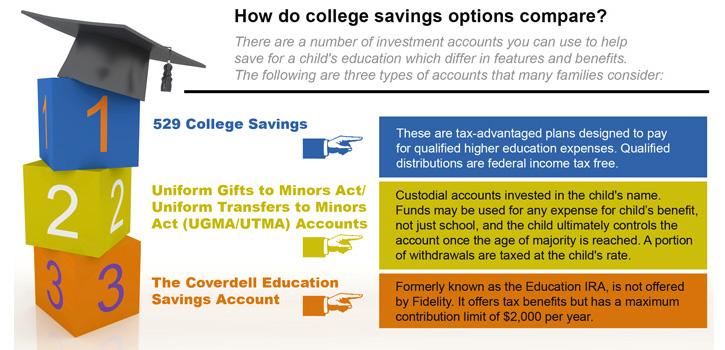

Exploring education savings accounts reveals a spectrum of tax-free growth opportunities that can significantly enhance your investment returns. 529 Plans are among the most popular options, offering tax-deferred growth and tax-free withdrawals for qualified educational expenses. This means the earnings in your account grow without the burden of annual taxes, maximizing the potential for compound growth. Coverdell Education Savings Accounts (ESAs) also provide a similar advantage, allowing tax-free growth and withdrawals for qualified education expenses, with the added flexibility of covering K-12 costs.

- Roth IRA for Education: While traditionally a retirement account, Roth IRAs can be tapped for education expenses. Contributions can be withdrawn tax-free, and earnings are penalty-free if used for qualified education costs.

- Uniform Gifts to Minors Act (UGMA) and Uniform Transfers to Minors Act (UTMA) Accounts: These accounts allow investment income to be taxed at the child’s lower rate, providing potential tax savings, though they lack the tax-free growth of 529 Plans and ESAs.

By strategically utilizing these accounts, you can optimize your savings and minimize tax liabilities, ultimately making education more affordable and accessible.

Maximizing Your Contributions for Optimal Tax Benefits

To make the most of your education investment accounts, it’s crucial to strategically plan your contributions. By understanding the nuances of these accounts, you can unlock significant tax advantages. Consider the following approaches:

- Maximize Annual Contributions: Ensure you are contributing the maximum allowable amount each year. This not only enhances your investment’s growth potential but also maximizes the tax-deferred benefits.

- Utilize Catch-Up Contributions: If you’re over 50, take advantage of catch-up contributions to further increase your investment. This can significantly boost your savings while providing additional tax benefits.

- Plan Withdrawals Strategically: Timing is everything. Withdraw funds in a way that minimizes tax implications, especially when paying for qualified educational expenses.

By implementing these strategies, you not only ensure the growth of your education fund but also optimize the tax advantages available, ultimately paving the way for a more financially secure future.

Leveraging Tax Credits and Deductions for Education Investments

When it comes to maximizing the benefits of education investment accounts, understanding the nuances of tax credits and deductions is crucial. These financial incentives can significantly enhance the value of your investments by reducing your taxable income and offering savings that can be redirected towards educational expenses. Education Savings Accounts (ESAs) and 529 Plans are two popular vehicles that offer compelling tax advantages:

- Coverdell Education Savings Accounts (ESAs): Contributions to ESAs are not tax-deductible, but the earnings grow tax-free. Withdrawals are also tax-free, provided they are used for qualified education expenses, which can include elementary and secondary education.

- 529 Plans: While contributions are made with after-tax dollars, the earnings grow tax-free. Qualified withdrawals are also tax-free, and many states offer tax deductions or credits for contributions to these plans.

In addition to these accounts, be sure to explore American Opportunity Credit and Lifetime Learning Credit, both of which can provide substantial tax relief depending on your eligibility. By strategically leveraging these tax benefits, you can effectively manage the costs associated with education and make the most of your investment.

Choosing the Right Education Investment Account for Your Financial Goals

When aiming to align your financial objectives with an education investment account, it’s crucial to understand the unique tax advantages each option offers. 529 Plans are a popular choice due to their tax-free growth and withdrawals when funds are used for qualified education expenses. Furthermore, many states provide tax deductions or credits for contributions, making it a compelling option for those looking to maximize tax efficiency.

Another noteworthy option is the Coverdell Education Savings Account (ESA). While contributions are not tax-deductible, they grow tax-free, and withdrawals for qualified expenses are also tax-free. This account allows for a broader range of educational expenses, including K-12 costs. Key benefits include:

- Investment Flexibility: Greater control over how funds are invested compared to 529 Plans.

- Broader Expense Coverage: Use for tuition, books, and even technological needs.

Choosing the right account involves weighing these tax benefits against your long-term educational savings strategy, ensuring alignment with your specific financial goals.

{kind=link}