As the cost of higher education continues to rise, the prospect of attending college without accumulating debt can seem daunting. Yet, with strategic planning and informed decision-making, it is entirely possible to achieve this goal. This article aims to equip you with practical tips and effective strategies for saving for college without the burden of loans. By taking proactive steps and making smart financial choices, you can pave the way for a debt-free college experience. Whether you are a student planning your future, or a parent preparing for your child’s education, these insights will guide you towards financial independence and educational success. Let’s embark on this journey together, transforming the dream of a debt-free degree into a tangible reality.

Start Early and Leverage Compound Interest

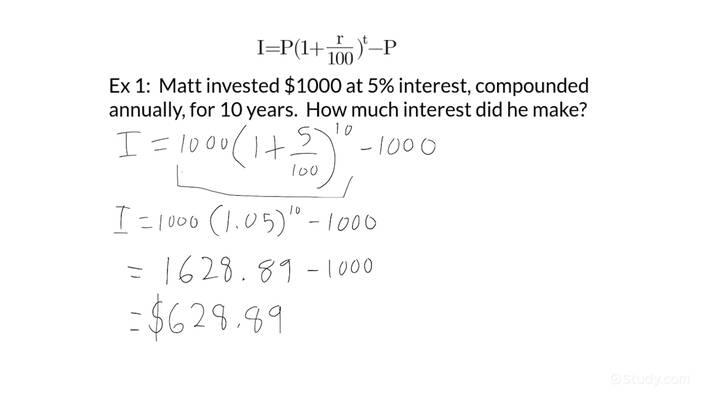

Starting your college savings journey early is one of the most effective strategies to ensure a debt-free education. By taking advantage of the power of compound interest, even modest initial investments can grow significantly over time. Imagine your savings as a snowball rolling down a hill, gathering more snow and momentum as it goes. Compound interest works similarly by earning interest not only on your initial deposit but also on the interest that accumulates over time.

- Begin with small, regular contributions: Even a few dollars a week can add up over the years.

- Automate your savings: Set up automatic transfers to your college fund to make saving a seamless part of your financial routine.

- Explore different savings accounts: Consider options like a 529 plan or a high-yield savings account, which offer potential tax advantages and higher interest rates.

By making the most of compound interest, you empower your savings to work harder for you, reducing the financial burden of college tuition in the future. The earlier you start, the more time your money has to grow, paving the way for a financially secure education journey.

Maximize Scholarships and Grants Opportunities

Securing scholarships and grants can significantly reduce the financial burden of college. Start by researching opportunities early; many organizations offer awards to high school juniors or even younger students. Use dedicated scholarship search engines and check with local community organizations, businesses, and educational institutions for available funds. Focus on those scholarships that align with your strengths, whether they are academic, athletic, or based on unique personal experiences. Remember, smaller scholarships can add up quickly, so apply for as many as possible.

- Tailor Your Applications: Customize each application to match the scholarship’s specific criteria and values. This shows genuine interest and increases your chances of success.

- Leverage Your Network: Reach out to teachers, mentors, and family members who might know about opportunities or be willing to provide recommendations.

- Stay Organized: Keep track of deadlines and required materials. A missed deadline can mean a missed opportunity.

- Follow Up: After submitting applications, consider sending a thank-you note to express appreciation and keep your name memorable to the selection committee.

Utilize Community Resources and Support Networks

Exploring and engaging with local community resources can be a game-changer in your quest to save for college without accumulating debt. Many communities offer scholarships, grants, and financial aid workshops that can provide valuable information and assistance. Local libraries, for instance, often host free seminars on financial literacy and college planning. Check with your high school guidance counselor or local community center for information on upcoming events or resources available in your area.

Support networks can also play a crucial role in your financial journey. Join online forums or local groups focused on college savings strategies. These networks can offer practical advice, share experiences, and even alert you to scholarship opportunities you might not find elsewhere. Additionally, consider reaching out to alumni networks from prospective colleges, as they may offer mentorship and financial guidance. By leveraging these community resources and support networks, you can access a wealth of knowledge and support that can help you achieve your college savings goals.

Implement Smart Budgeting and Spending Strategies

To effectively manage your finances while saving for college, consider implementing smart budgeting and spending strategies. Start by evaluating your current expenses and identifying areas where you can cut costs. This might include reducing dining out, cancelling unused subscriptions, or finding cheaper alternatives for entertainment. Allocate these savings directly into a college fund to maximize their impact.

- Set clear goals: Determine how much you need to save and establish a timeline to reach your target. Break this down into monthly savings goals to make the process more manageable.

- Use budgeting tools: Leverage apps and software to track your spending and savings. These tools can provide insights into your spending habits and help you stay on track.

- Prioritize high-impact savings: Focus on strategies that offer significant savings potential, such as refinancing loans or consolidating debt to reduce interest payments.

{kind=link}